Personal Wealth Management / Economics

Chart Flash: US Petroleum Imports

The shale boom in action!

For the past several quarters, US import growth has been pretty lackluster. Ordinarily, this might be concerning—weak imports typically mean weak demand—but in this case, it isn’t. Falling petroleum imports are the primary driver of headline weakness—a happy byproduct of the shale boom and another tailwind for US stocks.

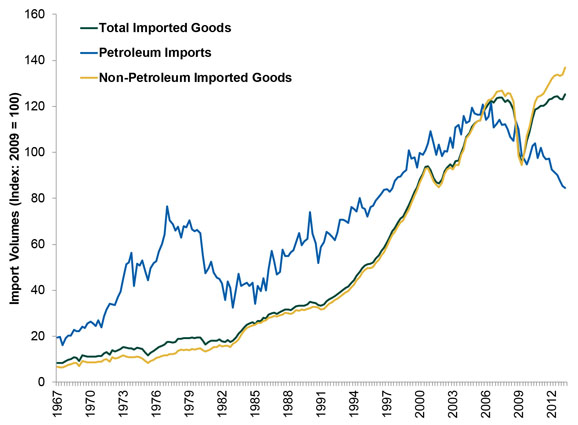

Exhibit 1 shows US import volumes (units, not dollars, in order to remove the skew of fluctuating oil prices) since 1967—total, petroleum and total ex-petroleum. Petroleum peaked in Q2 2007. Today, petroleum imports are back near 1997 levels. Yet headline imports are back at all-time highs, and non-petroleum imports are well into record territory. Demand is robust.

Demand for petroleum products is robust, too! It’s true US petroleum consumption is down from 2007’s peak, but since 2009 it has largely held steady—even as imports have continued falling. Thanks to shale, domestic production is up! In 2009, domestic oil production averaged 162.8 million barrels per month. Year to date, the monthly average is 217.4 million barrels.i

This is great for US firms—more energy produced at home means less money spent shipping it from overseas, which reduces costs. That’s one more reason US earnings are wrapping up their 14th straight quarter of growth.

Exhibit 1: US Import Volumes, Q1 1967 – Q2 2013

Source: Bureau of Economic Analysis, as of 8/29/2013.

i Source: US Energy Information Administration.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History COVID-Panic’s Lockdown-Low Anniversary2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today