Personal Wealth Management / Market Analysis

Checking in on Spain

With economic competitiveness improving and sovereign yields staying manageable, Spain’s decision to reject a bailout seems to be working out ok so far.

Mere months after Spanish Prime Minister Mariano Rajoy shunned bailout pressure from the likes of French President FranÇois Hollande, Spain’s doing just fine on its own. Photo: Antoine Antoniol/Getty Images.

Just last summer, it seemed not a day could pass without an EU official clamoring for Spain to request a full sovereign rescue. Spain, of course, demurred—Prime Minister Mariano Rajoy believed ongoing economic reforms and the bank rescue package he secured from the EFSF/ESM would give Spain enough breathing room to keep tapping primary markets (and we largely agreed).

Thus far, judging from Spain’s recent success at primary debt auctions, Rajoy’s decision seems to be working out ok. Though demand wobbled at times, Spain met all its 2012 funding targets and even got a head-start on 2013 in late December 2012. Yields retreated from a 7% spike in July, finishing 2012 near 5%, and year-end auctions saw increased foreign demand.

Spain has another tough fundraising burden this year, with €159.2 billion in maturing debt and total financing needs of €215 billion, but early results are promising. Last Thursday’s auction—the year’s first—exceeded targets at lower yields. Tellingly, a 13-year bond was 2.9x subscribed at 5.555%, compared to 2.1x coverage and 6.191% at the last comparable offering a year and a half ago, suggesting investors are gaining confidence in Spain’s ability to meet its long-term obligations. Tuesday’s auction of short-term debt was similarly successful, and expectations are for this Thursday’s offering of 2-, 5- and 28-year bonds to go just as well. At least for now, Spanish panic seems a thing of the past.

With 2012 financing overall successful and 2013 off to a good start, Rajoy’s passed a key test. When he took office in late December 2011, one of his biggest challenges was to earn investors’ patience as economic data deteriorated, giving him time to implement badly needed reforms—and allowing them time to work as intended. As expected, Spain’s economic performance in 2012 was dismal. Headline GDP, consumer spending and private investment fell hard, and unemployment—particularly youth unemployment—skyrocketed. But despite heightened volatility at times, investors remained willing to give Spain some breathing room.

No doubt the ECB’s actions played a role in this. The Outright Monetary Transactions program, where the ECB pledged to purchase bailed-out nations’ short-term debt on secondary markets, essentially gave investors a free put option in the event Spain needed a bailout, removing much of the near-term risk. This at least partly explains why the two-year debt sold last Thursday received strong demand despite being the first Spanish bond to carry a Collective Action Clause enabling the government to force haircuts on private-sector investors if the debt were restructured (required for eurozone debt issued from now on). The bank bailout, finalized in late 2012, also helped as it removed a key source of uncertainty—especially when the banks ended up needing less than the full €100 billion set aside. As part of the deal, financial sector restructuring also progressed. Banks no longer operate as non-profits, which gives them incentive to run more streamlined, disciplined (and ultimately successful) businesses—lowering the likelihood Spain will be on the hook for more bank losses.

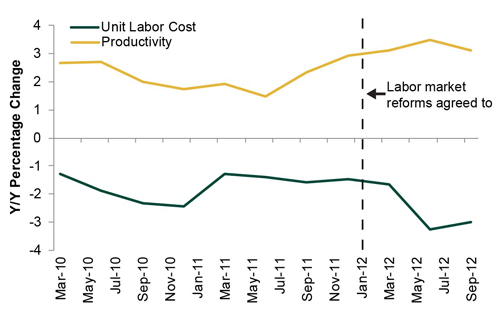

But investors also seemed to reward signs of fundamental progress. Productivity’s risen lately, helping unit labor costs to fall significantly—Spain’s getting more competitive. Notably, the margin between the two widened after Rajoy’s government, labor unions and employers reached an agreement on labor market reforms in January 2012 (Exhibit 1).

Exhibit 1: Unit Labor Costs and Productivity

Source: Bank of Spain.

In fact, according to a new IMF study, Spain’s competitiveness is now on par with France’s—and, unlike France, Spain’s moving in the right direction. This progress has helped exports continue growing apace, providing a much-needed source of economic strength.

Looking ahead, a more competitive Spain should attract ever more domestic and foreign investment, while productivity gains should help firms produce more goods for less—fuel for an economic recovery and eventual expansion. And economic growth begets higher tax revenues, which should further improve Spain’s debt sustainability over time. That’s not to say Spain’s out of the woods—the 2013 budget included nasty tax hikes, which will no doubt weigh on consumers and the private sector, and the recession’s expected to continue this year. But as long as Spain can keep demonstrating incremental progress, yields should remain manageable, buying the nation more time to continue reforming and return to growth without a full bailout.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 8 - June 122026-06-15

-

Market Analysis A Market Perspective on Iran Truce Whisperings2026-06-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today