Personal Wealth Management /

China Credit Crunch Redux?

Rising Chinese short-term rates have headlines warning of a credit crunch, but evidence suggests markets needn’t panic.

Chinese financial markets have been a bit stormy lately: Short-term rates are up, banks are hoarding cash, and the central bank is seemingly responding with tough love. And on cue, headlines are fretting a potential credit crunch in the world’s second-largest economy. In our view, however, these fears seem overwrought. Higher rates and cash squeezes are fairly normal near month-end in China, and while the readings are a bit more extreme this month, evidence suggests this is largely just politics and Chinese markets as usual—not a big concern for global markets.

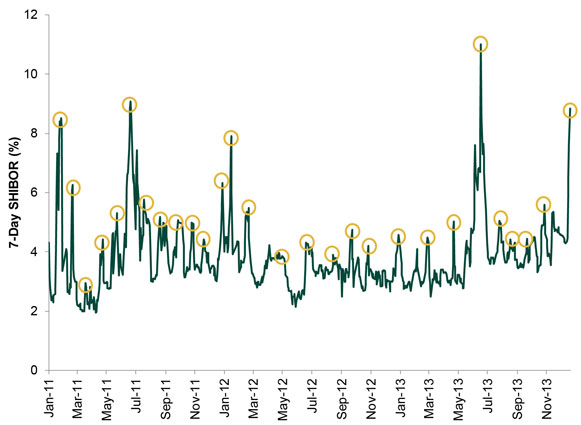

In China, banks must meet regulatory capital requirements at the end of every month, and it isn’t unusual for them to draw down buffers early then rebuild them before the audit. This scramble usually occurs in the last week or so of each month, and when demand for cash rises, so does the price. Exhibit 1 shows the 7-day Shanghai Interbank Offered Rate (SHIBOR) since 2011 began. Only three of the short-term spikes occurred before the 20th of the month—all others (circled) occurred after that. Current levels, though high, aren’t unusual—similarly high rates throughout 2011 and earlier this year didn’t wreak havoc.

Exhibit 1: 7-Day SHIBOR

Source: Shibor.org, as of 12/23/2013.

Historically, the People’s Bank of China (PBOC) has helped keep SHIBOR down by boosting liquidity amid the scramble. In June, however, officials allowed rates to spike in an apparent effort to spook banks into reducing off-balance sheet lending. These loans (aka “shadow financing”) accounted for about 30% of all new financing in the year’s first five months, which didn’t please Chinese regulators—they can’t control off-balance sheet loans as they can traditional financing, making money supply more difficult to manage. Plus, these loans typically go to regional governments, which use the cash to fund unapproved construction projects, further messing with the national government’s growth plans—and exacerbating municipal governments’ already sizeable debt load. Many of these loans are wrapped into “wealth management products” (WMP), which China’s state-run banks offer as higher-yielding alternatives to traditional deposits. About half of the nation’s WMPs mature every three months, and another 25% mature semiannually, driving up banks’ demand for cash in June and December. Withholding liquidity at these times is an easy way for the government to encourage banks to lend more judiciously.

Evidence suggests they’re doing the same today. After decelerating in September and October, off-balance sheet lending resurged in November, suggesting banks were once again defying the government’s goals. Now, with year-end capital requirements looming and most WMPs in need of refinancing, the time seems ripe for another shot across the bow. Compounding matters, the central government is tightening fiscal policy somewhat. Historically, year-end government spending has helped boost liquidity. This year, that funding source isn’t as great as in years past.

But, as in June, the PBOC seems likely to eventually ease up. Then, officials announced they’d provide liquidity to select banks who did play by the rules, and market pressures eventually eased. This time, officials have already provided the first round of those targeted liquidity injections, adding about $50 billion to the system on December 19 as SHIBOR jumped. Some suggest the continued use of opaque, nontraditional liquidity injections rather than normal open market operations suggests the PBOC won’t be accommodative enough, while others suggest rising rates mean the central bank is powerless. Yet it’s not that the central bank can’t intervene. It’s more that they don’t want to add cash to the extent many observers seem to want—it’s out of step with their longer-term aims. However, still-rising rates give them incentive to step in further as needed—a full blown credit crunch and banking panic isn’t exactly on the government’s Christmas list. The Communist Party relies on financial stability and continued growth to keep the masses more or less placated under one-party rule. Allowing a full-blown funding meltdown (ü la US financial markets post-Lehman) would be tantamount to asking for an uprising.

In short, a “bank shock,” as some describe it, seems highly unlikely. Officials have heavy incentive to keep the financial system functioning, and they have plenty of firepower. Forex reserves totaled about $3.5 trillion at last count. China also has a fairly robust history of recapitalizing the state-run banks dominating its financial network. Not that banks are starving for cash. According to the PBOC, they have about $250 billion in excess reserves on deposit with the central bank—“relatively high,” according to the bank. Analysts estimate total reserves ($3 trillion) amount to about 15% of all on- and off-balance sheet loans—levels the Basel committee would consider robust. In a true bank shock, banks wouldn’t have anywhere near that big a buffer.

Not that we expect Chinese money markets to be cheap and awash with liquidity from here. While SHIBOR eased after June ended, it remained elevated compared to the first half of the year as the PBOC remained hesitant to add broad liquidity. Judging from the latest editorials in state-sponsored media, reining in the state-run banks remains a top goal. The government is also moving toward a more market-driven banking system, which would expose banks with weaker balance sheets to risks they haven’t historically faced, keeping demand for cash high. Marry that with tightish supply, and borrowing costs seem unlikely to drop back to 2011’s average levels.

But global stocks likely don’t need easy Chinese money markets for this bull market to continue. With expectations so low, a financial system that simply keeps functioning smoothly and an economy that keeps growing at a brisk (if not double-digit) pace is likely good enough to surprise most investors to the upside.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today