Personal Wealth Management /

China Removes The Floor on Its Bank Lending Rate

A brief note on credit dymanics in China.

The People’s Bank of China announced it will remove the floor on bank lending rates, moving Chinese rates one step closer to a market-oriented system. China has long kept a firm grip on lending and deposit interest rates in order to maintain some degree of control over the money supply and broader economy. Most recently, the lending rate was set at 0.7x the one-year benchmark lending rate—after being reduced a year ago from 0.8x and 0.9x before June 2012. This is a noteworthy indication of the government’s dedication to reforms despite the slowing economy—a positive—but its near-term financial impact is likely limited.

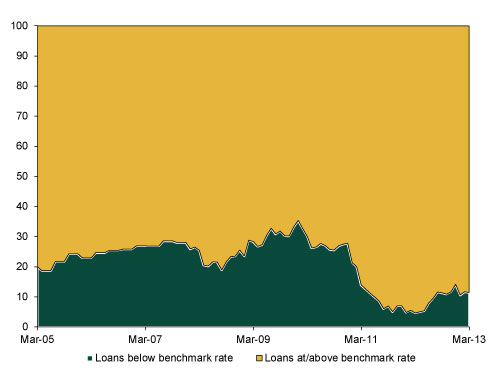

For one, the move likely won’t have an immediate impact on banks as most loans were already priced about 90% above the benchmark rate, as you can see in Exhibit 1.

Exhibit 1: Chinese Loans Below and Above Benchmark Rate

Source: People's Bank of China.

But the move is symbolically important. It’s a clear signal the new government remains committed to financial liberalization and market-oriented reform despite recent turmoil in China’s shadow banking system. Removing the lending rate floor could also allow banks to more quickly and easily adapt to market forces and changing loan demand conditions—a first step toward credit allocation based on price, not quantity.

China’s regulated interest rates limited the role of price signals in credit allocation. With deposit rates capped at artificially low levels and few options other than bank deposits, savers were essentially a captive, cheap market for banks. Meanwhile, demand for loans was more normal. In this model, banks were incentivized to maximize volume—hence the usage of loan quotas by the government to cap quantity and prevent a bubble. The government recognizes this model is increasingly inefficient, and its move to increase loan quotas and reduce reserve requirements didn’t spur as much lending as expected last year.

This is probably one reason the Chinese government condoned the country’s developing shadow banking system in the past few years. Wealth Management Plans (WMP) and other products were simply a way of getting around the deposit rate restrictions and letting some market forces bleed in. However, increased competition made banks’ deposit base more volatile, thus limiting their ability to lend for longer periods. Indeed, medium- to short-term loans as a percentage of total loans have been declining since early 2011.

Liberalizing interest rates—i.e., removing the cap on deposit rates and the floor on lending rates—would allow banks to compete more directly with the shadow banking system. Friday’s removal of the lending floor, along with tighter regulation on shadow banking, shows this is likely the direction the government is headed. However, the bigger reform would be getting rid of the ceiling on deposit rates, which would allow Chinese banks to react to market forces and stabilize their funding—putting them in better position to extend loans, reduce rates and compete with shadow banking.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today