Personal Wealth Management / Market Analysis

China’s Confounding Trade Data

Chinese import growth decelerated and widely missed estimates Tuesday, yet Chinese equity markets showed little negative influence.

China’s imports badly missed expectations Tuesday, rising just 11.8% y/y versus expectations of 18.0% y/y. Yet Chinese equities rallied.

Why the dichotomy? The answer may be in two parts. First, the reality may not be as bad as the headline number indicated. After all, commodity imports rose substantially by volume. Copper volumes led the way, rising to a new all-time record on the back of a whopping 48% y/y gain. Most analysts estimated the miss on import numbers was due to the faster-than-expected commodity price declines. It takes time for spot prices to filter through contracts, and it appears analysts underestimated the speed with which it occurred.

Still, both exports and import growth rates continued to decelerate, which brings us to the second—and more important—reason Chinese equities may have rallied. It’s likely inherently forward-looking equities care more about the outlook than the recent past. And China can’t afford a recession. With its authoritarian government structure, a recession breeds social instability and revolt. With no ability to vote, protests are the only way for the people to express their displeasure.

Therefore, the more its economy slows, the more stimulus China likely needs to add to maintain economic growth. This is primarily done by expanding loan growth, which is closely controlled with loan quotas. Much-higher-than-expected December loan growth and the first acceleration in loan growth rates since November 2010 seemingly further illustrate this. Additionally, since September China has cut income taxes and oil production taxes, raised power prices while limiting coal prices (incentivizing energy production), cut banks’ reserve requirements, delayed the implementation of Basel’s stricter bank regulations and approved local governments to extend the maturity of bad debt. Not bad for a few months’ work.

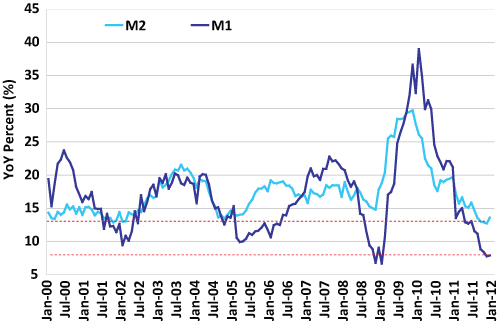

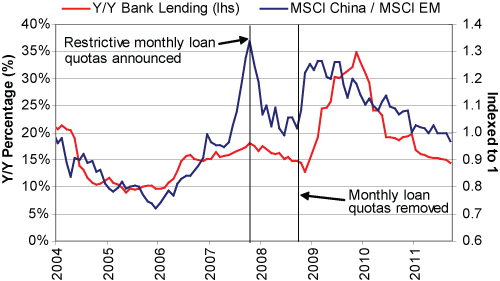

Importantly, China’s equity markets historically tend to track these domestic loan growth cycles, outperforming Emerging Markets when loan growth accelerates and underperforming when it decelerates. Therefore, with money supply growth rates appearing near a cyclical trough and most signs pointing towards a reacceleration, the outlook for Chinese equities appears bright.

Exhibit 1: China Money Supply Near Cyclical Low

Source: Thomson Reuters.

Exhibit 2: China Loan Growth Vs. Relative Performance

Source: Thomson Reuters.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today