Personal Wealth Management / Market Analysis

Chinese Checkers

Chinese GDP slowed a bit in Q1, but the economy should still do fine overall in 2013.

China’s getting less bang for its buck from urbanization and infrastructure development, but economic reforms should yield a more sustainable model over time. Photo by China Photos/Getty Images.

In most nations, 7.7% y/y GDP growth would be cheered. In China, however, it was a disappointment. After GDP grew 7.9% in Q4, most analysts were expecting Q1 to top 8%. The slower-than-expected result led many to question the durability of China’s reacceleration.

In our view, the pessimism seems unwarranted. The 7.7% growth rate may be slower, but value added is larger—if China were to grow 7.7% for full-year 2013, it would contribute more to global GDP in dollar terms than it did when it grew 7.8% 2012. Plus, the government has every incentive to keep growth elevated in 2013, the new administration’s first year in power. Historically, growth during a new administration’s first year has been above-trend as officials sought to shore up support. With inflation decelerating, officials have plenty of latitude for monetary stimulus, and policymakers have already telegraphed some loosening in Q2.

At the same time, we wouldn’t expect a gangbusters acceleration from here. The official growth target is 7.5%, and anything above likely satisfies policymakers. Officials have admitted as much, saying growth likely slows as they engineer a shift from the investment-fueled export-oriented system to domestic consumption-led growth. That was evident in Q1, when the slowdown was led by weaker-than-expected industrial production (8.9% y/y vs. 10.1% expected) and fixed asset investment (20.9% y/y vs. 21.3% expected) while retail sales met expectations at 12.6% y/y.

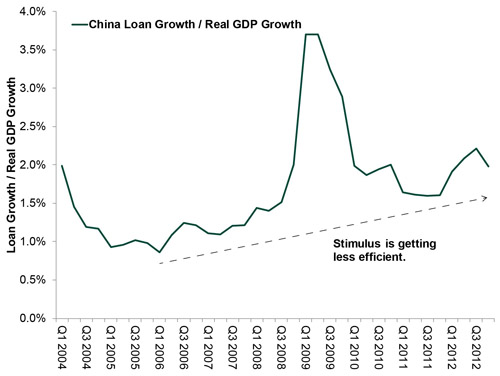

For 20 years, China’s made easy gains by essentially confiscating people’s savings at artificially low rates (via capital controls and low deposit rates at state-run banks), funneling the money into infrastructure and property development through state-run bank lending, and relying on urbanization for productivity gains. Lately, however, China hasn’t gotten as much bang for its buck. 2009’s massive stimulus program helped get GDP back on track post-2008, but it was inefficient—it took a disproportionately large amount of money to generate 1% of real GDP growth. That spike was temporary, but China’s model has grown steadily more inefficient since 2006—it takes nearly twice as much loan growth to generate equivalent GDP growth. (Exhibit 1)

Exhibit 1: Loan Growth for China to Generate 1% of Real GDP Growth

Source: Thomson Reuters, as of 03/05/2013.

This inefficiency frustrated officials last year, when looser loan quotas didn’t boost growth as quickly as they anticipated. Almost all of the money went to state-run firms (SOE), which weren’t doing well—SOE profits fell -11.8% and -16.1% in Q1 and Q2 2012, respectively, and finished the year up only 2.7%. Investment in them was woefully inefficient. China’s small and medium businesses (SME) tend to be more profitable, but SMEs couldn’t get funding unless they were willing to pay credit card-like rates to loan sharks. So officials did the smart thing and deregulated corporate financing markets. They expanded corporate bond issuance, raised caps on foreign investments in corporate debt and allowed simple derivatives trades to entice investors, believing large firms would gravitate to corporate debt markets, freeing up bank capital for private SMEs. They also expanded off-balance sheet lending, peer-to-peer lending and other forms of shadow financing to further broaden SMEs’ access to capital. The measures seem to have worked. Total Social Financing rose nicely, and China’s SME development index rose in Q4 2012 for the first time in eight quarters and accelerated in Q1.

So officials seem to realize their best shot at boosting growth over time is economic liberalization. Which means Q1’s slower growth rate could very well be a catalyst for further reforms. The new administration has already proposed wide-ranging changes, including reforming the migrant registration system (to boost urbanization), modernizing farmland lease rules and liberalizing interest rates. They’ve also raised foreign investment caps, expanded last year’s VAT reform nationwide and extended regional pilot programs for full financial deregulation.

Reform progress is likely a meaningful driver of Chinese stock returns moving forward, though it likely takes time for these and other pending changes to materially impact the economy. In the near term, however, the economy has plenty of fundamental support. Total Social Financing surged in Q1, which should support investment and growth. And while newly enforced real estate curbs hit housing markets in Q1, looking ahead, demand should stabilize as more first-time homebuyers enter the market, and property investment should reaccelerate. Quarterly GDP growth rates could very well continue fluctuating, but overall, China likely logs perfectly fine growth in 2013—and provides plenty of support to global GDP.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today