Personal Wealth Management / Market Analysis

Clearing Up Bond Trading

How far do regulators' rule proposals go for improving transparency for bond investors?

Most bond trading is as opaque as this black case. Photo by Todd Bliman.

Here is a simple question that often doesn't have a simple answer: How much did you pay to buy that bond? This week, the Municipal Securities Rulemaking Board (MSRB) and the Financial Industry Regulatory Authority (FINRA) proposed amendments to their current rules that seek to make that answer easier to come by, clarifying transaction costs for municipal, corporate and agency debt securities. Their plan is a step in the right direction, in our view, but the proposed rules are still less clear than they could otherwise be.

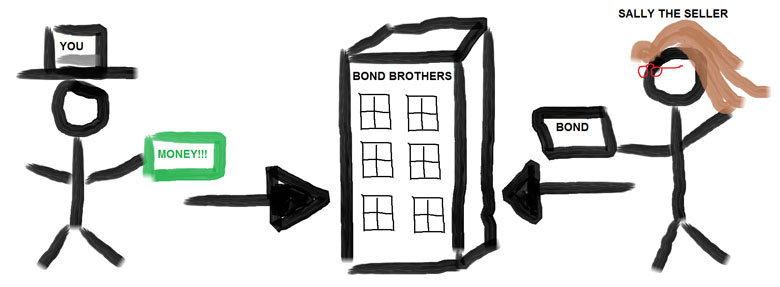

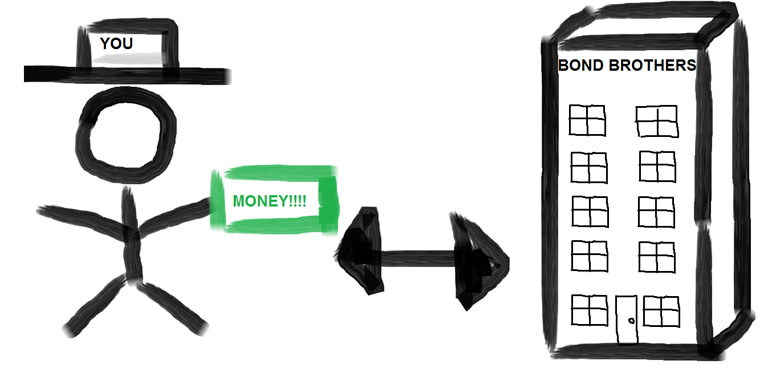

The reason it isn't always easy to know what you as a retail investor paid for a bond is due to the mechanics of bond trading. With most non-Treasury bonds, your buy order must be submitted to a brokerage firm. That firm can then act in one of two capacities. The first is agent, in which the firm takes your order and seeks out the desired bonds, helping execute the trade on your behalf. (Exhibit 1) This isn't terribly dissimilar from equity trading, in which the firm takes your order and seeks to match it with someone selling similar securities in a market or exchange. In such transactions, fees are usually disclosed plainly. However, most bond trades don't happen this way. Most are executed with the firm taking your order acting as principal, which basically means they sell you bonds from their inventory. (Exhibit 2) They typically do not charge a commission per se, so your trade confirmation doesn't show you an account of the broker fees involved.

Now, before you presume this means, "Most bond buying is free! Wheeeeee!" consider: Instead of commissions, firms acting as principal simply mark up the bond price (or down, if you're selling). They are required to report only the price you paid for the bond and some description of the security, including basic information like its yield. Heck, sometimes firms even blur the line between agency and principal, selling you bonds they are actively trading in, so their "inventory" isn't exactly bonds sitting on a dusty shelf. They may sell you bonds they just bought (plus a markup)-so-called "riskless principal" transactions. [i]

Exhibit 1: Bond Trading With Firm Acting as Agent

Source: Our imagination.

Exhibit 2: Bond Trading With Firm Acting as Principal

Source: Ibid.

Maybe this seems a little underhanded, but consider: Virtually every retailer in the world sells something they bought and marked up. But the difference, in our view, is that if you are buying a pair of jeans, you can find similar jeans from various retailers, compare, contrast and buy the cheapest (or most expensive, if you're a label lover!). It's tough to comparison shop the same or similar bonds without knowing the fee built into the bond's price. Said differently, you don't know if you are buying a bond at the bond market's equivalent of Dollar General or Hermes.

This is where regulators come in. The MSRB and FINRA now want muni, corporate and agency bond dealers[ii] to shed more light on this by publishing a reference price for each bond, allowing investors to compare. This reference price is a reflection of what price similar securities were trading at without a markup at roughly the time of the trade. This may seem to imply you could take the price you paid, subtract the reference and boom![iii] divine the markup. But a reference price is merely an estimation of the going market prices of similar securities. The dealer's actual cost could be higher or lower. Some bonds are also relatively illiquid, which makes you wonder how comparable those prices really are anyway.

And it doesn't even apply to all bond trades. Both regulatory bodies limit the requirement to "riskless principal" transactions where 100 bonds (less than $100,000 face value) or fewer are being traded. Reference prices stem only from those trades executed the same trading day. The MSRB thinks it should apply only to transactions where the dealer is on the same side of the trade as transaction in question. For example, the reference price would be disclosed if a muni dealer sells 10 bonds to one buyer for $10,000 and 10 bonds to another buyer for $10,050. FINRA thinks dealers should disclose reference prices in offsetting transactions-where the dealer is a buyer in one transaction but a seller in another.

Currently, if investors want this information, they have to scrounge it up on their own. And unfortunately, researching bond prices isn't as easy as pulling up Google Finance and typing in a ticker. They'd have to pull up regulators' databases (EMMA at the MSRB and TRACE at FINRA[iv] or ante up thousands for a professional Bloomberg terminal), and run their own numbers to determine each mark-up. By that point, prices may have changed, making all that work darn near worthless. That regulators want to make this information readily available is a plus!

Regardless, regulators' goals are two-fold: increase transparency and encourage competition. If investors have a better understanding of what they're paying, they're better able to choose who they trade through. Which are good goals! But it is worth questioning whether this is really the best, most clear, most easy-to-understand way to get there. If improving transaction cost transparency is the target, we wonder why costs aren't being disclosed a la equity market trades? After all, on a stock trade confirmation, you can see clearly what you paid. Commission. SEC fees. Other charges, if applicable. Complete transparency.

We'll always vote for more transparency than less-so this is a step in the right direction. But the move isn't as clear as it could be, so the step doesn't go quite far enough, in our view.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] To be clear, no investment is riskless. However, FINRA defines "riskless principal" as a trade in which a member who has received a customer order immediately executes an identical order in the marketplace, while stating on the role of principal, in order to fill a customer order.

[ii] The MSRB, as the name implies, regulates only muni bonds. FINRA does the other stuff.

[iii] This is not like sis-boom-bah. That is the sound made when a sheep explodes.

[iv] We know, that's a lot of acronyms.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today