Personal Wealth Management / Market Analysis

Coal’s Continued Decline Defies Political Narratives

While many see political policies as responsible for coal’s decline in America (for better or worse), reality shows this is a lot more about basic economics.

Around a decade ago, the article you are presently reading online would likely have been delivered to you via the magic of coal-fired electricity. In the intervening years, however, that has become increasingly uncommon. Coal’s share of US electricity output has fallen tremendously—a trend the COVID lockdowns have compounded. Why this decline? For years, many have chalked it up to political policy—which some see as a positive and others a negative. But as we have written for years, while politics may play a fringe role, coal’s plight has a whole lot more to do with market economics and seismic shifts in America’s energy industry. The direct investing implications of this are limited, as pure-play publicly traded coal firms are a rarity these days. But the industry’s state—and its cause—is a reminder to get beyond common narratives and assess data even-handedly.

Wednesday, the US Energy Information Administration (EIA) estimated that, based on railcar loadings, US total coal production had dropped a stunning -27% year-to-date through May 2020 versus the same period in 2019.[i] The culprit, of course, is the economic lockdowns tied to the coronavirus, which have crushed demand worldwide. EIA data show coal exports fell -29% year-over-year in 2020’s first five months, while coal-fired utility production plummeted -34%.

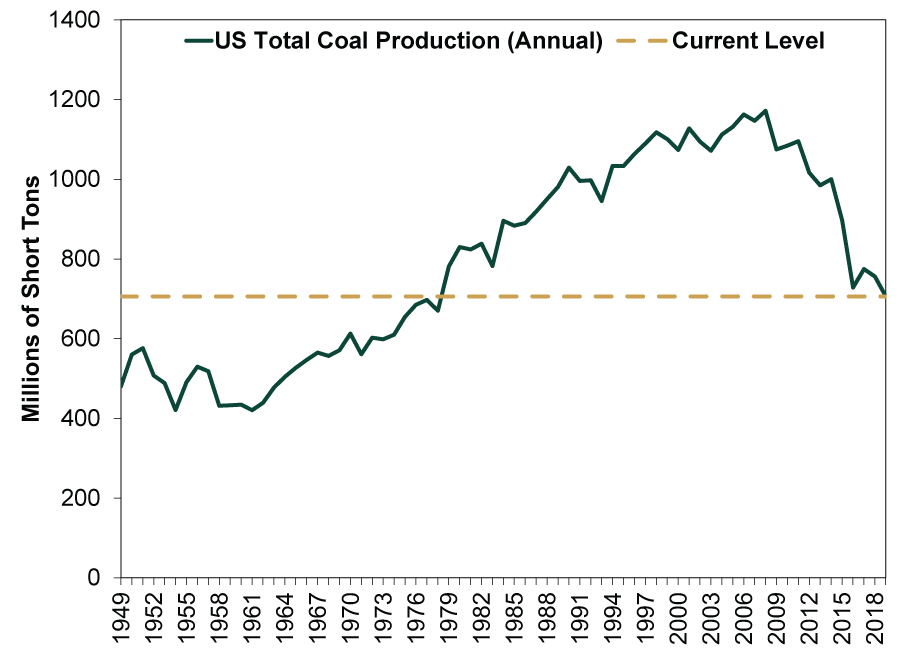

While the lockdowns almost certainly exacerbated the huge declines—which will likely reverse to some extent as reopening shows up in the data—the trend isn’t new and it isn’t coal’s friend. As Exhibit 1 shows, US coal production fell to levels unseen since 1978 last year—in the pre-coronavirus era.

Exhibit 1: US Total Coal Production

Source: Energy Information Administration, as of 7/30/2020. US total coal production, 1949 – 2019. The 2019 data are preliminary, based on tallies of weekly output.

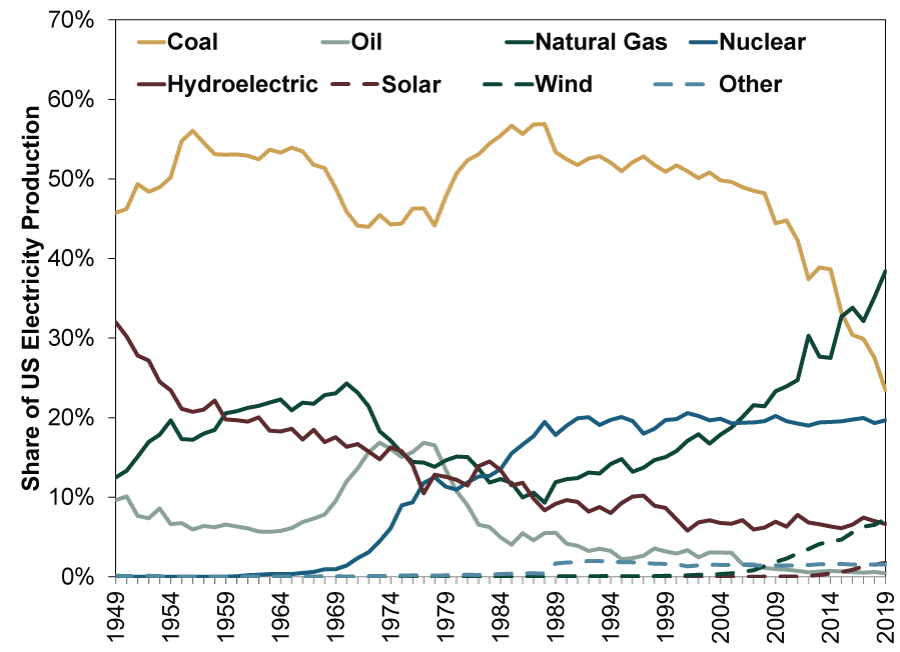

Exhibit 2 hints at why coal’s share plunged so much. Electric utilities are coal’s biggest demand driver by far, and US utility demand for coal has fallen off a cliff since 2008.

Exhibit 2: US Electricity Production by Source, 1949 – 2019

Source: Energy Information Administration, as of 7/30/2020.

Now, that year happened to coincide with the financial crisis, which likely triggered much of the initial drop. That also happened to be the year Barack Obama was elected president, with cleaner energy one of his campaign talking points—and this is where many injected politics into coal’s plight.[ii]

When coal failed to rebound after the economy resumed growing, many cited political policies—clean air mandates and such—as responsible. Critics called it a “war on coal.” Perhaps political policies played a role, to the extent they helped drive the rise in wind power production. But the change in administrations in 2016 did nothing to change coal’s trajectory. That shouldn’t shock, because it wasn’t renewables or policy or anything else stemming from Washington that impacted coal’s fortunes. Natural gas waged the actual war on coal, to the extent that term makes sense. Its march continues. As Exhibit 2 shows, natural gas became the primary source fuel for US electric utilities in 2015. While it, too, has suffered from the coronavirus this year, the overall trend is up.

The shift that has sunk coal’s fortunes coincides with the rise of America’s shale oil and gas fields’ production. The huge output growth in US natural gas from shale fields in Texas, Oklahoma, North Dakota, Pennsylvania and elsewhere sent supply surging—and slashed prices relative to coal. That decline mitigated the chief advantage that gave coal its edge for most of the post-war era: Its abundance in America kept prices low relative to other sources. Market economics knocked King Coal off its throne.

Again, there are no huge, direct investment takeaways from this. But it is a minor lesson in questioning political narratives. We believe there is huge value in that practice for pretty much any investor.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today