Personal Wealth Management / Market Analysis

Coal’s Trump Card a Bust

The new administration wants to save American coal-but natural gas may stand in the way.

Coal country has struggled in recent years: A just-released report by the International Energy Agency notes that firms in various stages of bankruptcy control over half of US production. The sector employs just 50,000 people now, down from over 250,000 in 1980. The bulk of the losses are concentrated in Appalachian states like West Virginia and Kentucky, where mining hours are plummeting and local budgets are squeezed. Given this backdrop, it isn't surprising coal became a political issue in 2016's race, particularly since many claim the Obama Administration declared war on coal through a series of Environmental Protection Agency (EPA) emissions-trimming rules. Whatever you think of this argument, President-elect Trump garnered broad support in America's industrial heartland[i] in part by promising to roll back restrictions and bring back jobs. Coal, therefore, is frequently cast as a "winner" in his election, which may lead some to wonder whether now isn't a buying opportunity in this old economy mainstay. But while a lighter regulatory hand may be a small boon for the industry, cheaper and more plentiful natural gas poses a threat even a coal-friendly president can't fix.

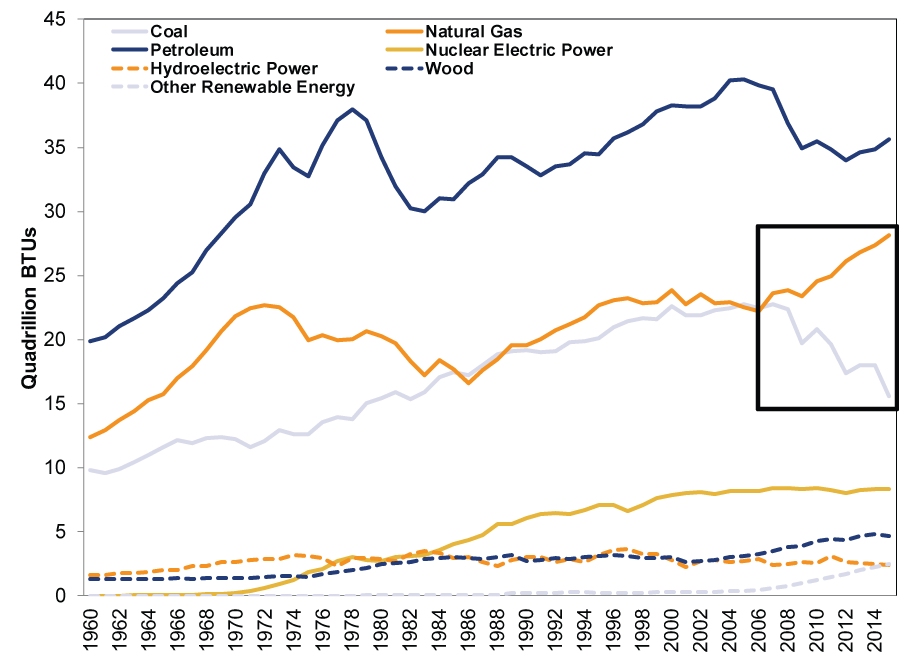

This is a tale of two energy sources. As coal firms around the world shut down, wade through bankruptcy or require state support, natural gas continues to benefit from the American shale boom. Coal used to be America's most abundant source of domestic energy-enjoying a cost advantage that kept it fueling power plants, whether folks like the associated emissions or not. But natural gas production has risen massively since the Financial Crisis, and prices are down 60% since 2008, to the point that coal's historical cost advantage is essentially gone. As a result, natural gas is gaining US market share at coal's expense-and the trend started years before the EPA's actions. Most coal-producing states were already on track to exceed the new standards when they were issued, thanks to natural gas's ongoing ascent. That's right-the EPA fired a dud in its alleged "war on coal."[ii]

Exhibit 1: US Primary Energy Consumption by Fuel Source, 1960 - 2016

Source: Energy Information Administration, as of 11/21/2016.

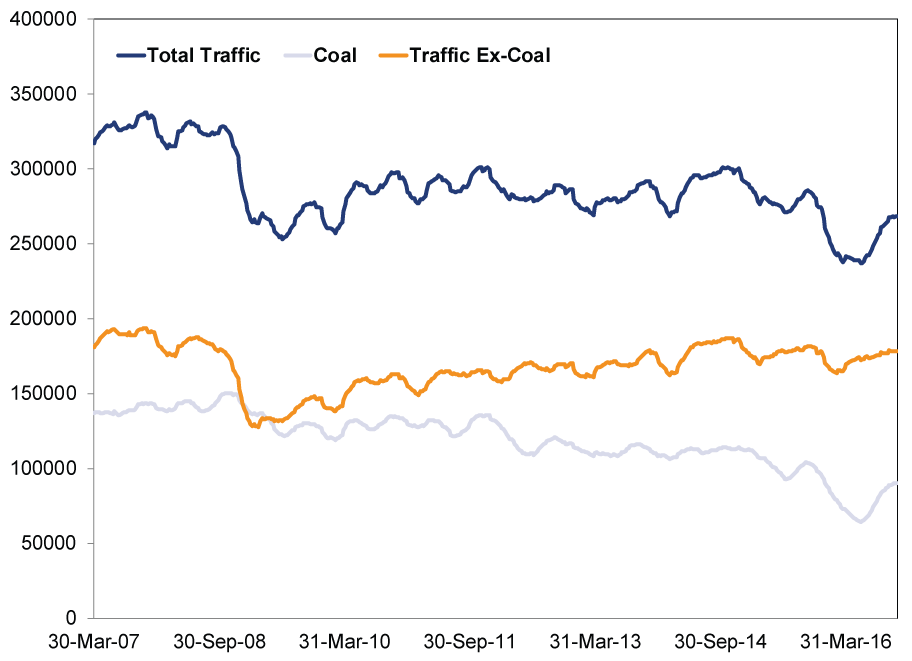

No matter your thoughts on the incoming or outgoing Administrations' respective policies, what's going on in that black box has little to do with shifting political fortunes. There is no denying coal's decline. This is why many metrics-long skewed by the industry's big influence in fueling power plants, steel mills and exports-look weak. Shipments especially: Whether by land or by sea (well, river or canal), coal must travel from mining sites to its final destinations. As Exhibit 2 shows, coal shipments by train are trending lower, while other forms of rail traffic hold steady-and that decline predates the EPA's rules.

Exhibit 2: Coal Drags Down Rail Traffic Totals

Source: Association of American Railroads, 13-week moving average of US rail traffic, as of 11/23/2016. March 2000 - November 2016.

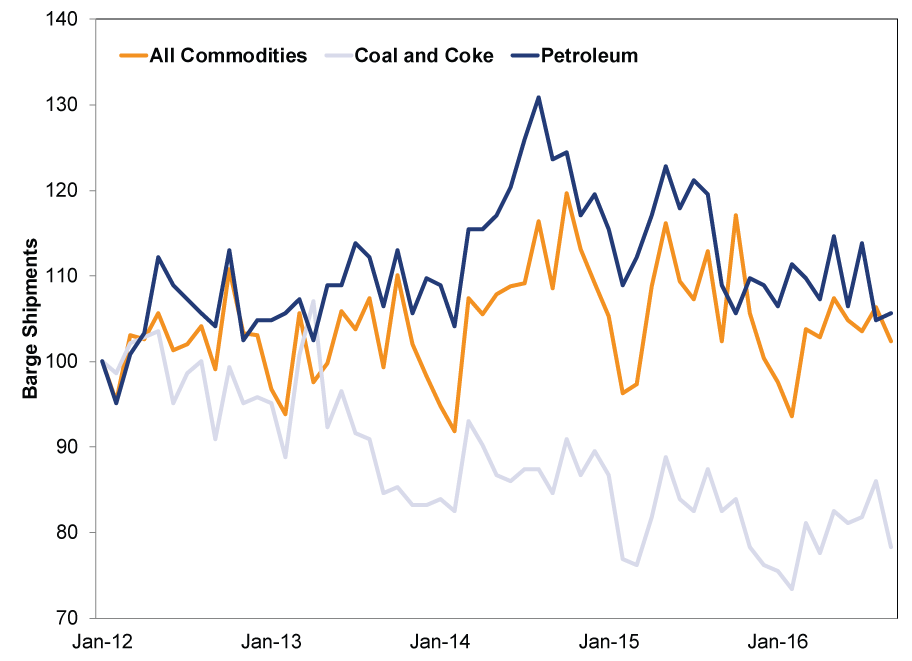

Commodity shipments on US waterways (Exhibit 3) tell a similar story, as coal and coke (a product derived from coal) weigh down the headline figure.

Exhibit 3: Coal Slows Commodities Shipments by Water

Source: US Army Corps of Engineers, Waterborne Commerce Statistics Center, as of 11/16/2016. Commodity shipments by water, January 2012 - September 2016, indexed to 100 at the start of the period.

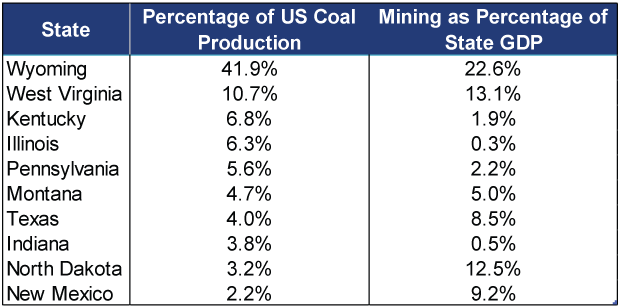

The resulting pain is concentrated in particular regions of the country: As Exhibit 4 shows, high-production states feel coal's malaise most keenly, as mining figures prominently in many of their economies.[iii]

Exhibit 4: Top 10 Coal-Producing States in 2015

Sources: State="" coal="" production="" as="" a="" percentage="" of="" US="" total:="" Energy="" Information="" Administration=""; Mining="" as="" a="" percentage="" of="" state="" GDP:="" Bureau="" of="" Economic="" Analysis=""; both="" as="" of="" 11=""/23/2016.

Importantly, although many states rely more heavily on coal, it isn't a major driver of US growth. In 2015, the industry (together with other forms of non-oil and gas extraction) contributed just 0.4% to GDP.[iv] This is probably a good thing, because coal's prospects likely wouldn't improve even if the President-elect's growing cabinet were staffed entirely by coal miners.

The symptoms of coal's displacement by the ascendant natural gas industry are everywhere. In 2015 alone, 94 coal-fired power plants closed, taking the equivalent of all Kentucky's electricity contributions from coal offline. Another 200-over a quarter of the US total-have target retirement dates today, and there are virtually no new coal-fired power plants under construction. Beyond electricity, coal is also used to fire blast furnaces for steel-this accounts for about 15% of global coal consumption. But there is a global glut of steel already, and new technologies can turn old scrap metal into new, usable steel, reducing demand for new steel. Plus, natural gas furnaces are cheaper and easier to build, and operate more cost-effectively to boot.

Around the world, the story's the same-many countries (such as Canada, France, Denmark and the Netherlands) are setting targets for phasing out coal entirely-and not because they're taking a brave pro-environment stand no matter what havoc the move might wreak on their energy supply. (Sorry, but we doubt many politicians are willing to take on that kind of reelection risk.) This is going to sound very cynical, but there is much more evidence the organic ascent of natural gas permits them to score points by acting as if their "aggressive emissions targets" are saving the day. In a nutshell, this is the current state of coal-afflicted more by new technologies and cheaper, cleaner energy sources than by governmental edicts. As a result, its fortunes (in the US and elsewhere) probably won't reverse any time soon, even with a friendlier face in the White House.

Investors thinking there is a bottom to fish here risk buying into an industry that is on life support. Certainly, there will be demand for coal at some price for years to come. But growth is likely isolated abroad-this is an export-oriented market-as some Emerging Markets nations are much more coal-reliant presently. US shale gas export capacity is very small presently, and will take years to grow. There is a window. And here the administration may be able to help, if it can ink myriad deals to export coal to willing recipients abroad. But investing based on that would be quite speculative indeed, especially since the rhetoric from the Trump administration isn't particularly pro-trade.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today