Personal Wealth Management / Economics

Consistently Taxing

A look at some historical facts in honor of 2012’s tax day.

US taxpayers got a reprieve this year—no, rates aren’t lower, nor will the government be handing out automatic refunds to everyone (though that would be nice). But they do get to file two whole days later than usual! (Because April 15 fell on a Sunday and April 16 is Emancipation Day, which is recognized in Washington, D.C.) This being an election year to boot, tax rhetoric has been particularly heated—with both presidential candidates releasing 2011 tax returns and finger-pointing from both sides about who is and isn’t paying their “fair share” (however that’s defined).

As political agnostics, we refrain from weighing in on those particular questions. But potentially more useful is a quick look at some US tax system facts:

- Aside from a short-lived version funding the Union’s Civil War related expenses, the federal income tax was first instituted in 1913—the top rate was 7%.

- Just four short years later, the War Revenue Act of 1917 increased the top rate to 67% to help fund World War I—a 52 percentage point increase over 1916’s rates.

- The top rate peaked at a hefty 94% in 1945.

- According to some analysts, the tax code contained just 11,400 words in 1914.

- In 2010, that number was closer to 3.8 million. (For comparison’s sake, War and Peace has a little over 560,000 words; the Declaration of Independence has 1,337; and the Gettysburg Address has a scant 270 or so words. Heck, without amendments, the US Constitution—the document defining who has the authority to write the tax code in the first place—has only about 4,500.)

- According to the IRS’s Taxpayer Advocate Service, individuals and businesses spend roughly 6.1 hours annually preparing and filing their taxes.

- By one count, the national cost of complying with US tax laws in 2008 was around $163 billion.

Some of these may seem shocking numbers—and no doubt lead some to conclude we need tax reform. To an extent, we agree—as we’ve saidbefore, a simpler and overall flatter tax code would likely free businesses and individuals to spend valuable resources currently devoted to tax preparation (and no doubt tax avoidance) on much more productive uses. Like increased discretionary spending, business expansion and investment, hiring and so on.

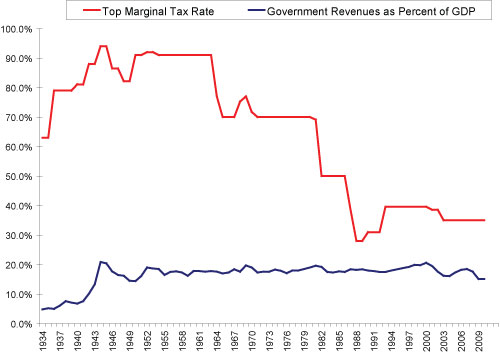

But the interesting thing about the US tax code is that as varied as it’s been, in the post-war era, the percentage of GDP federal tax revenues constitute has hovered pretty consistently around 18% (see Exhibit 1).

Exhibit 1: Historical Tax Revenues Versus Top Marginal Tax Rates

Source: Fisher Investments Research, Tax Policy Center.

Meaning whether top rates have been 50% or 90%, that hasn’t much impacted the amount of revenue the government collects relative to GDP. Indeed, in 1982, after President Reagan cut the top tax rate from 69.13% to 50%, tax revenues as a percent of GDP dropped a mere 0.4 percentage points. (Note that doesn’t mean the government received less revenue.) And when President Johnson (acting on the proposals of JFK) cut the top rate from 91% in 1963 to 77% in 1964, tax receipts as a percent of GDP only dropped 0.2 percentage points. One could no doubt parse the data for more similar examples.

The logical conclusion seemingly being as top rates go up, businesses and individuals are increasingly incentivized to find ways to avoid paying those top rates—thus, the billions of hours and dollars spent seeking savings embedded in the 3.8 million words of our tax code. Meaning, the likelihood tax rate increases are too successful at actually increasing the absolute amount the government takes in is pretty slim.

A better way to accomplish that goal? Well, we could tax politicians every time they mention rejiggering the tax code (then again, maybe they’d adjust behavior accordingly, too). In our view, finding ways the government can infringe less on individuals’ and businesses’ abilities to earn and produce likely leads to better results. Because at the end of the day, the more folks produce, the more they’ll pay in taxes—after all, the same fraction of a bigger pie is a bigger slice. Meaning to an extent, the government can have its cake and eat it, too—provided it has the restraint necessary to stand largely aside and let the private sector do its thing. But we’re not counting on that anytime soon.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today