Personal Wealth Management / Market Analysis

Corporate Debt Fears in Perspective

While defaults might tick up, the corporate bond market doesn’t appear likely to implode.

As stock markets fell over the past few weeks, a parallel fear emerged: a wave of corporate bond defaults, particularly in the high-yield (aka junk) segment. Investment-grade and junk yields spiked to their highest levels since the end of the last bear market, sparking visions of companies unable to refinance debt without breaking the bank. Couple that with high issuance in recent years, and headlines are sure a long-feared corporate bond bubble is finally bursting. While we think it is reasonable to expect some defaults—particularly the longer the interruptions to business persist—we think a closer look at the issue should help assuage those broader debt crisis fears.

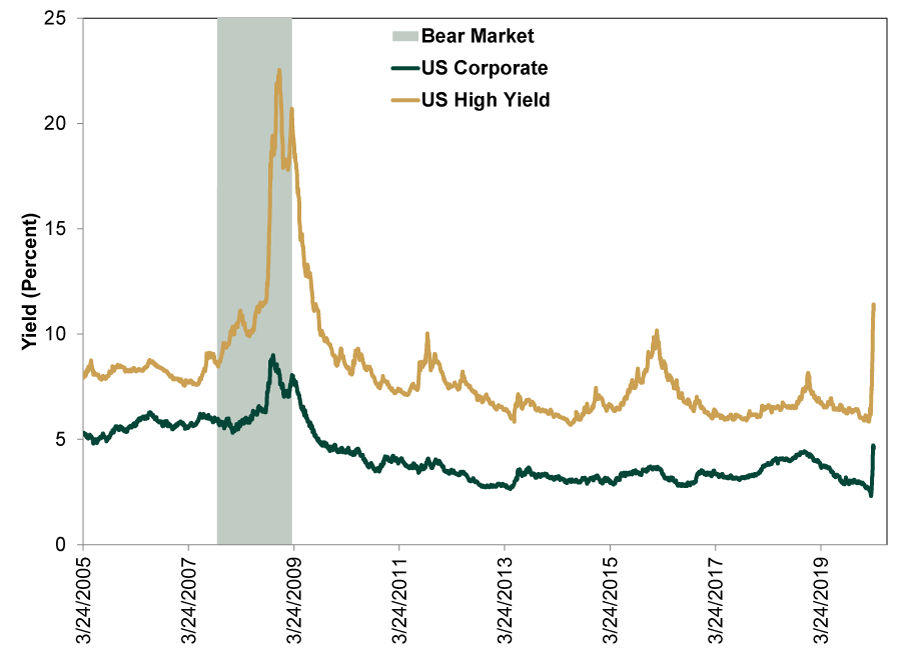

First and foremost, we think a little historical perspective is in order. Corporate bond prices can correlate highly with stock prices over short periods. Since bond prices move in the opposite direction as yields, it isn’t abnormal for corporate bond yields to spike during a stock market downturn. Notably, as Exhibit 1 shows, the spike thus far pales in comparison to the 2007 – 2009 bear market, which didn’t include a massive wave of high-quality bond defaults.

Exhibit 1: A 15-Year Look at Corporate Bond Yields

Source: FactSet, as of 3/25/2020. ICE BofA US Corporate and US High Yield indexes, yield to maturity, 3/24/2005 – 3/24/2020.

Corporate bond default generally happens under one of two circumstances: Companies can’t raise cash to repay maturing bonds, or they don’t have cash to make interest payments. That second scenario sparked some dread last week, when financial markets showed a scramble for dollars and low liquidity. But the Fed’s actions Monday helped ease a lot of those pressures and included provisions aimed squarely at corporate bonds. Several companies tapped the market on Tuesday, finding robust demand and manageable yields. The $2 trillion COVID-19 rescue and fiscal stimulus package currently being debated in Congress also includes patchwork funding solutions for corporations small and large. Again, we aren’t saying every corporation in America will emerge unscathed, but there are a lot of backstops.

High-yield debt, however, is less backstopped than investment-grade firms, as they were excluded from the Fed’s corporate bond buying program. Those yields are also much higher than their investment-grade counterparts, and the companies are less creditworthy—none of which is really new. But that doesn’t mean the whole category is under stress. The trouble is primarily concentrated in Energy firms, which isn’t new either. Energy firms, particularly smaller ones, have experienced rising defaults over the past year thanks to continually weak oil and natural gas prices, which hurt their revenues. That pain will probably continue as the OPEC price war rages on, keeping a low ceiling over crude. But it is also a known issue. As of February’s end, the trailing 12-month default rate for the broad high-yield universe was 2.4%.[i] For Energy, it was 9.1%.[ii] In mid-2016, the last time oil and gas producers had to deal with rock-bottom prices, their default rates were in the neighborhood of 20%.[iii] So don’t be surprised if this gets worse. Yet even then, the broad high-yield default rate was only around 5%.[iv] Energy’s problems weren’t a bloodbath for all high-yield issuers. It also highlights markets’ ability to pre-price defaults rather than waiting for them. Hence, the defaults in 2016 mostly rose after Energy bond yields had jumped.

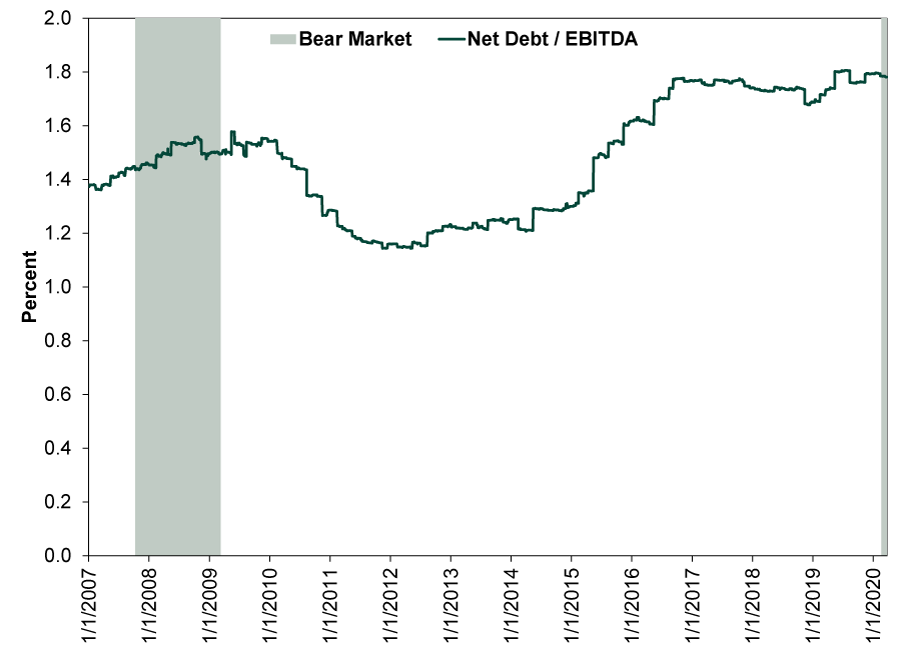

It is also important to note that overall and on average, companies entered this stretch in pretty good shape. Exhibit 2 shows S&P 500 companies’ net debt (debt minus cash on hand) as a percentage of earnings before interest, taxes, depreciation and amortization (EBITDA). That tells you the burden they have to finance with the money that comes in, which is the best indicator of how reliant they are on future sales to service debt. Present levels are in line with the last four years, around 1.8%. Now, that figure uses trailing earnings, so it doesn’t factor in the hit many companies are about to take from COVID-19 containment efforts. But note that even in the depths of the last bear market, as junk yields passed 20% and earnings plunged, major US companies broadly didn’t run into lasting, acute financing trouble.

Exhibit 2: US Corporations’ Debt Burden

Source: FactSet, as of 3/25/2020. S&P 500 net debt / earnings before interest, taxes, depreciation and amortization, 1/1/2007 – 3/24/2020.

Again, we aren’t saying all is rosy. Smaller companies operating on a shoestring—especially those in the shale oil patch—probably face a hard time ahead. Some will go under. But this is a normal feature of bear markets and, if it comes to it, recessions. Usually it is the market’s way of shaking out the excess, the weak players that can’t compete. That isn’t necessarily the case this time, as COVID-19 containment walloped the bull market and economy before the late-cycle froth could really get going. But setting aside the cause, we have seen this general movie—economic problems and spiking yields—before. Recession-era defaults don’t break corporate bond markets for good and they haven’t forestalled market and economic recoveries. Rather, they are just part of the normal cycle.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today