Personal Wealth Management / Market Analysis

Corrections: Scary Random Dips That Shouldn't Hurt Your Portfolio

While media are calling for a correction, no one can reliably predict them-doing so is an exercise in futility, in our view.

Between North Korea, loud protests, terror strikes and hurricanes, 2017 probably feels anything but calm. Yet for stocks, it has been one of the calmest years on record. According to The Reformed Broker, the S&P 500's maximum drawdown (i.e., drop from most recent high) this year is the lowest in the index's history. Yet far from enjoying the ride, investors seem to be waiting for the proverbial other shoe to drop and hit markets with a correction. We've seen several pundits arguing one is "due" and warning folks to prepare. While we, too, think investors should always be ready for volatility, it isn't because a correction is particularly likely to strike now. Nor do we think it's possible to skirt them. Corrections are unpredictable and impossible to time with precision repeatedly, and in our view, investors who try typically end up doing more harm than good.

A lot of articles play fast and loose with the term "correction." Some get it right, portraying corrections as short, sharp sentiment driven drops of around -10% or worse that end quickly. Others say "correction" but really mean "bear market," which is a deeper, longer, fundamentally driven decline of -20% or more. We even saw one article call for an "80% correction," which would actually be a devastating crash that makes a typical bear market look like child's play. This distinction is important. Because bear markets are usually longer, slower and have identifiable fundamental causes, it's possible to detect one as it forms and avoid a chunk of the downside. Not so with corrections, which are short and violent. By the time you realize you're in one, chances are it's just about over, making selling a risky proposition.

Corrections' speed wouldn't be a problem if they were predictable-but they aren't. Articles trying to predict them or saying one is more likely now base the claim on the length of time since the last correction ended-19 months. That's just over the historical average of 18 months between bull market corrections.[i] But averages aren't predictive. Corrections are random-they start any time, for any or no reason. This bull market began in 2009. We had two corrections in 2010, two in 2011, one in 2012 and then none until 2015 - 2016's. Random! It would be great if corrections operated on schedules, but they don't. The reason we regularly remind folks one could occur isn't to try to time it, but so readers can start preparing now to hang tough whenever the pullback arrives.

Why hang tough? Because the real risk associated with corrections isn't experiencing one-it's shooting yourself in the foot as you try to dance around it. It is a multi-pronged decision. When do you get out? What do you hold while out? When do you get back in? Will you really be able to nail the top and bottom?

We aren't aware of anyone who has answered all those questions correctly on a repeatable basis. The urge to sell is often strongest as corrections near a bottom-after all, the market is falling fast and folks want out. But that is the exact wrong time to sell, because you lock in losses while opting out of the impending rebound. To catch the ride up, you'd have to be willing and ready to buy back in when the proverbial blood is in the streets-when most folks don't want to buy. They prefer waiting for the all clear (which never comes). Trading costs and potential tax implications add insult to injury. But no lasting damage is done if you keep a cool head and sit tight. The challenge for most is enduring the ride down without hitting the eject button before the ride back up.

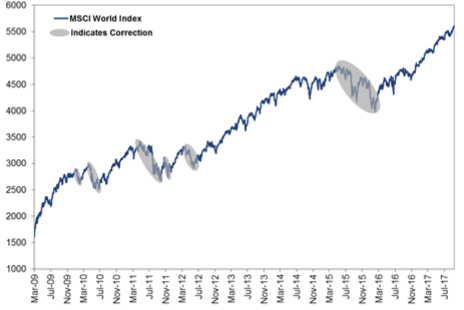

Corrections aren't fun, but they fade quickly. Ultimately they amount to short-term wiggles along bull markets' journey higher. Long-term equity investors need not fret these bumps in the road. This bull market clearly illustrates that. Its six corrections had varying duration and magnitude, but none prevented the overall rise. Markets are resilient, quickly sort out false fears and resume their climb.

Exhibit 1: Corrections in the Current Bull Market

Source: FactSet, as of 9/21/2017. MSCI World Index with net dividends, 3/9/2009 - 9/21/2017.

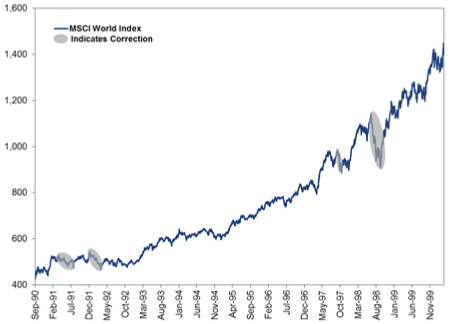

Same goes for past bull markets-randomly timed brief downturns ultimately become a blip in a longer-term uptrend.

Exhibit 2: Corrections in the 1990s Bull Market

Source: FactSet, as of 9/21/2017 MSCI World Index with net dividends, 9/28/1990 - 3/27/2000.

Corrections are a hot topic now as we regularly hit new market highs. Many in the media aim to call the top. But this isn't the right way to think about positioning. In our experience, you really can't spot that the market has topped until at least three months after. It takes time to collect data and see signs that fundamentals, not sentiment, are driving stocks lower and have underappreciated potential to keep doing so. Remembering this can help you avoid the trap of selling in the throes of a correction, only to miss the bounce back and remaining bull market returns.

[i] Source: FactSet, as of 9/21/2017; MSCI World Price Index 12/31/1989 - 9/21/2017

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

-

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

-

Expert Commentary This Week in Review | Consumer Confidence, Iran Developments, Bond Yields

2026-05-29

2026-05-29 -

Market Analysis What AI Tech Stocks Are Signaling About This Bull

2026-05-28

2026-05-28

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today