Personal Wealth Management / Market Analysis

Currencies’ Short-Term Wobbles Balance With Time

Two charts help put the dollar’s recent moves in perspective.

As the dollar’s slide versus the euro continues hogging headlines, so do misperceptions about currency swings’ impact on portfolio performance. As we showed last month, yes, the weak dollar does add to US investors’ returns on eurozone stocks, since Americans get the stock’s actual return plus the currency appreciation. But we don’t think this should play much of a role in determining whether to emphasize eurozone stocks in a global portfolio. Currency cycles and geographic leadership shifts often don’t line up. Here is another reason not to get too hung up on currency moves for good or ill: Though they can affect returns in the short run, they tend to even out over time.

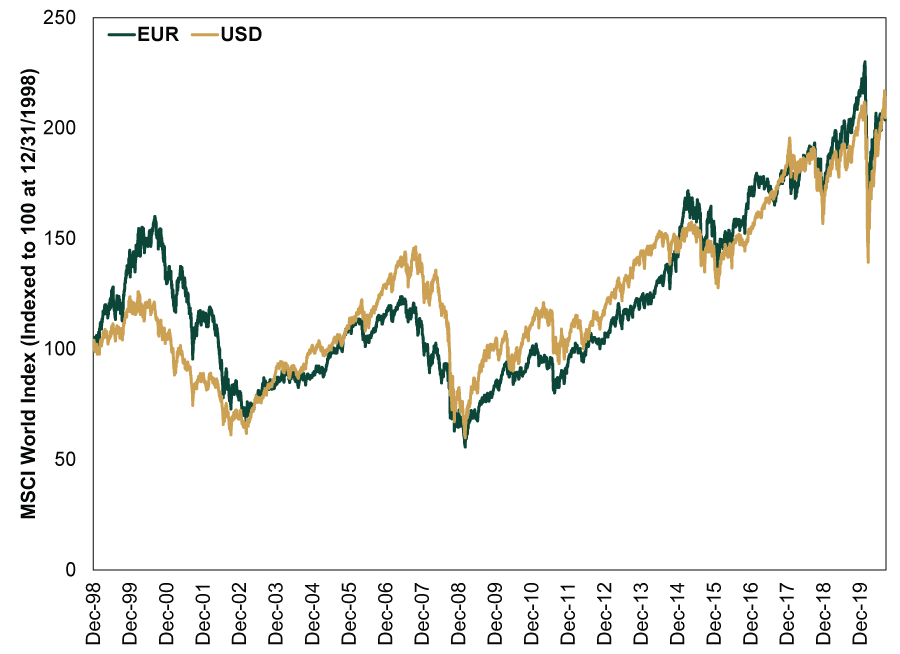

Exhibit 1 shows this darned near perfectly, in our view. It shows the MSCI World Index’s daily price return in euros and US dollars since the euro’s birth on January 1, 1999. As you will see, the two lines often deviated—sometimes by a decent margin. But now, despite all those fluctuations, they are in basically the same spot. In dollars, world stocks’ price return is 108.4% over this span. The euro-based return is a shade behind, at 106.1%.[i]

Exhibit 1: Different Journeys, Same Destination

Source: FactSet, as of 9/15/2020. MSCI World Index price level in USD and EUR, 12/31/1998 – 9/14/2020. Price returns used in lieu of total due to daily data availability.

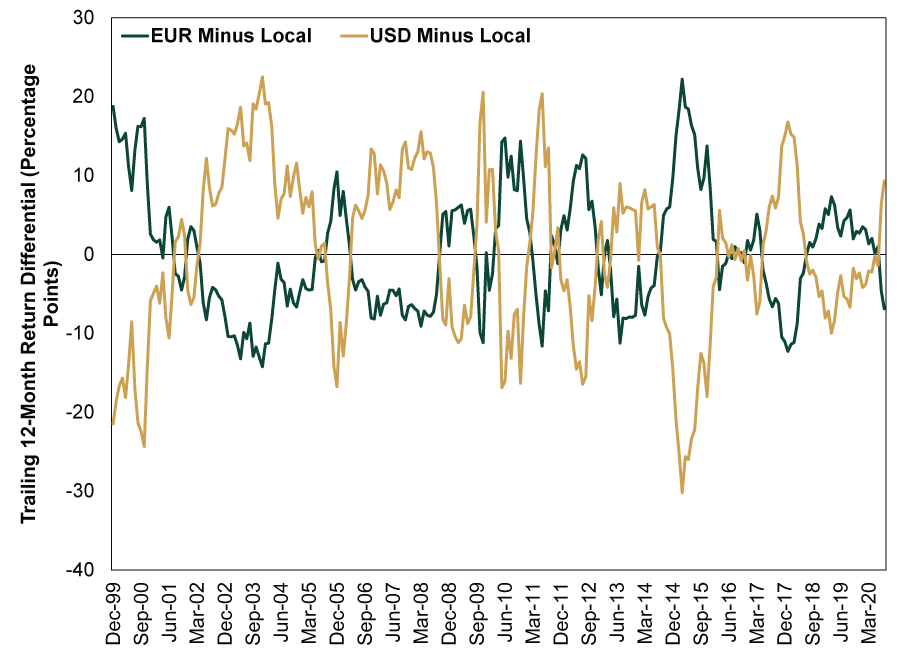

Now, this doesn’t mean you need to wait 20 years for currency moves to even out. As Exhibit 2 shows, the short-term skew fades relatively quickly. This chart shows the gap between trailing 12-month returns in local currency (each company’s currency of issue) and euros and dollars, respectively. The gap flips often and irregularly—too frequent and random to position a portfolio around, in our view.

Exhibit 2: Short-Term Currency Effects Are Just That

Source: FactSet, as of 9/15/2020. MSCI World Index monthly return with net dividends in local currencies, USD and EUR, 12/31/1998 – 8/31/2020.

In our view, currency swings shouldn’t inspire fear or greed—just patience and discipline. Reacting to them, like reacting to any form of market volatility, amounts to positioning for past performance—a recipe for error. Staying cool and thinking long-term are pretty much always more beneficial in the long run, and we think this is the wisest course today.

[i] Source: FactSet, as of 9/15/2020. MSCI World Index price return in USD and EUR, 12/31/1998 – 9/14/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the Iran Flare Up2026-07-08

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

-

Market Analysis Can Germany Engineer Faster Growth at Last?2026-07-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today