Personal Wealth Management / Economics

Deficit Hype

A broad lack of enthusiasm over the sharp drop in the US’s federal deficit suggests investors are as skeptical as ever.

How skeptical are investors? Judging by headline reactions to the Treasury Department’s annual report this week, pretty skeptical! The fiscal 2013 deficit plunged to $680.28 billion, down from 2012’s $1.089 trillion. But many headlines didn’t cheer—some bemoaned still-rising debt, while others decried the government’s apparent focus on fiscal restraint over economic growth. The former is emblematic of investors’ difficulties moving past longstanding worries, the latter a sign most folks still have a pretty backward perception of the US’s economic health. Both are bullish for stocks.

The deficit has shrunk overall and on average since 2009, and in 2013 it narrowed from both ends. Tax revenue rose 15%, partly because of minor tax increases, like the two-year payroll tax holiday’s expiration. But rising US incomes, corporate profits and investment gains also played a vital role—the tax base grew! Meanwhile, spending fell for the second straight year. You’d think this would please most observers—those who fret a weak economy might notice broad growth generated a bigger tax haul, while fiscal hawks would cheer the apparent budget discipline.

However, we’re still in the “good news is bad news” phase of this bull market. So we see statements like, “deficits are falling too far, too fast”—the pithy version of the Fed’s “fiscal policy is restraining growth” line in recent press releases. Others claim growth should be the feds’ top priority and “government belt-tightening” isn’t helping—in other words, without “adequate” government spending, the economy will tank.

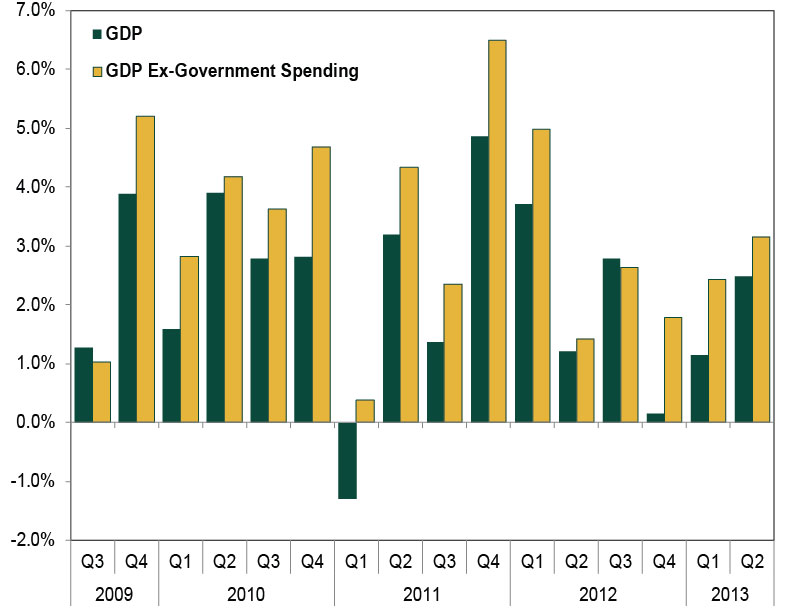

Thing is, the US relies far less on government for growth than these statements presume—the private sector comprises over 80% of the US economy. Private businesses and the tens of millions who work for them are our economic engine, and they’re doing quite well. As Exhibit 1 shows, private sector growth has more than offset government cuts.

Exhibit 1: GDP vs. GDP Ex-Government Spending

Source: FactSet Data Systems, as of 10/15/2013. US GDP and Government Consumption Expenditures and Gross Investment, seasonally adjusted annual rates, in chained 2009 US dollars, Q3 2009-Q2 2013.

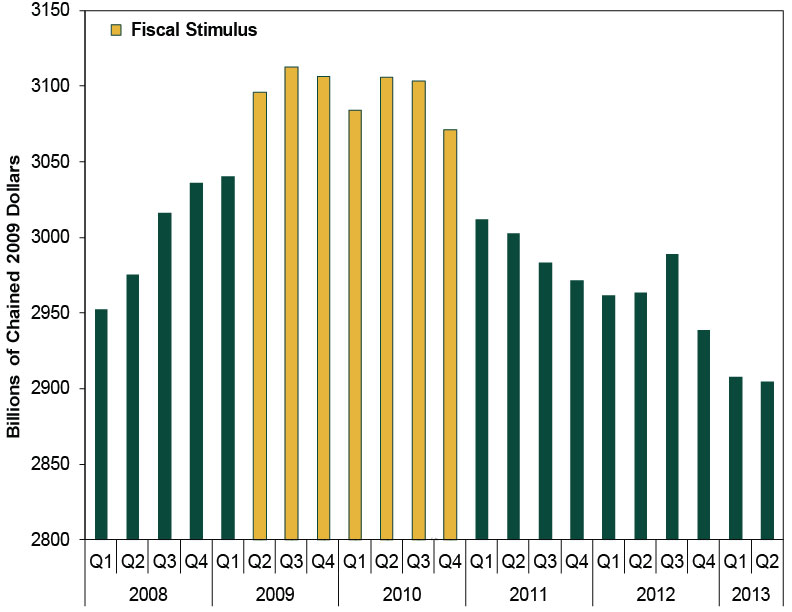

While government cuts detract from headline growth, they aren’t necessarily the full loss many assume. Federal cutbacks create room for private businesses to provide the same service—new opportunities for small business owners and entrepreneurs! Where the government isn’t spending, the private sector can step in, innovate, grow and thrive. That said, we haven’t necessarily entered some age of austerity. Think back to why deficits were so high in 2009 and 2010—largely TARP and the fiscal stimulus package. Now that the government has retreated from stimulus, deficits are creeping back to earlier norms. (Exhibit 2) This is largely how it’s supposed to work. A government boost helped jumpstart growth after the recession, keeping capital moving when the private sector stalled. Then the private sector roared back, letting the government ease off the gas. This is why GDP continues hitting new highs even with the government drag.

Exhibit 2: Real Government Spending

Source: FactSet Data Systems, Inc., as of 10/11/2013. Government Consumption Expenditures & Gross Investment, seasonally adjusted annual rate, Q1 2008-Q2 2013.

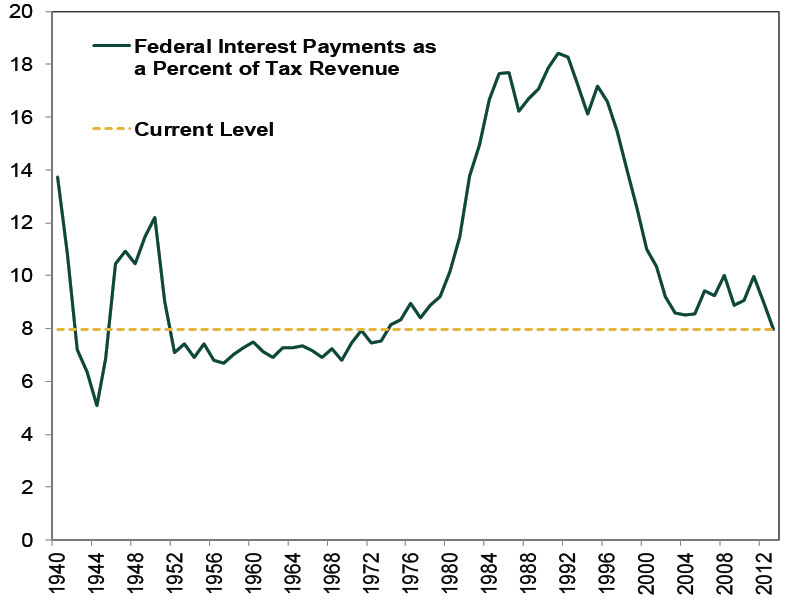

As for the ever-present debt fears, well, they may never truly fade even with the US’s improving fiscal footing. Endlessly adding more debt wouldn’t be great, but debt currently isn’t a pressing risk—yes, the total amount is rising, but the cost of servicing our debt (which is what determines sustainability) is falling. Interest payments have fallen from 10% of tax revenue in fiscal 2008 to 8% in fiscal 2013. (Exhibit 3) Even with rates rising recently, the government is still rolling over maturing debt at cheaper rates than when it was issued, so costs could very well continue falling.

Exhibit 3: Federal Interest Payments as a Percent of Tax Revenue

Source: St. Louis Federal Reserve, 1940-2013.

For investors, the good news is expectations for US growth and finances still appear pretty dim—and given the private sector’s underlying strength and our very affordable debt service, reality seems primed for an upside surprise, which should help propel stocks up the proverbial wall of worry.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today