Personal Wealth Management / Market Analysis

Did the US Economy Have a Case of the Mondays?

Never judge a book by its cover, or an economy by headline data.

The latest US manufacturing and consumer spending numbers hit Monday, and if you take most coverage at face value, it wasn't pretty. "Cautious consumers hold back on spending in December as concerns rise about US economy," said one headline. "Consumer spending cooled in December as Americans padded savings," said another. Manufacturing "continued to contract," and the Institute of Supply Management's report had a "weak tone." It all left folks wondering how worried we should be and if the long-feared recession is nigh. None of these headlines really give you the full scoop. As it happens, ISM's survey showed manufacturing output and new orders rose, and when adjusted for inflation, so did consumer spending. But the widespread effort to find a cloud in a silver lining shows where sentiment is: still in the doldrums. It shouldn't take much for US growth to beat expectations and give stocks some positive surprise.

Consider manufacturing. The headline Purchasing Managers' Index (PMI) hit 48.2 in January-higher than December's 48.0, but still below 50, therefore indicating contraction for the fourth straight month. That fed the long-running narrative of a manufacturing recession that's poised to take down the US economy. But if you look at the PMI's components, it doesn't exactly look recessionary. New orders and production moved back into expansion at 51.5 and 50.2, respectively. New orders' rise is particularly noteworthy, as today's orders are tomorrow's production-it's the most forward-looking component. The biggest detractors were inventories-always open to interpretation-and employment, which is always and everywhere a late-lagging indicator. While one month doesn't make a trend, January's report has plenty of reasons for optimism.

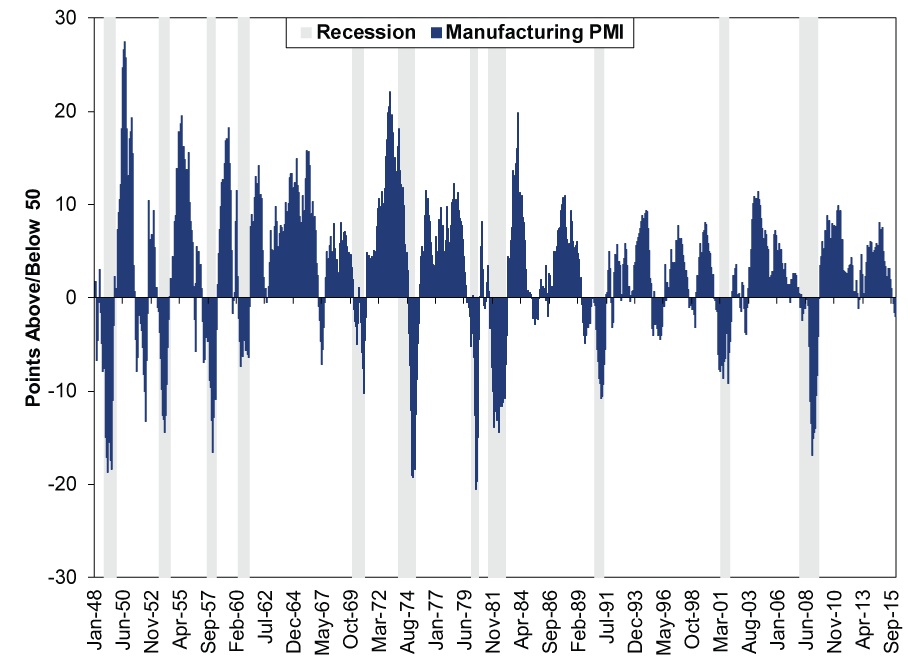

Plus, for all the handwringing about this being the longest contractionary streak since the recession ended in 2009, the actual decline is small-much smaller than you usually get in a recession. As Exhibit 1 shows, it looks much more like the 10 or so false reads since 1948. There were deeper, longer declines in the 1980s and 1990s. But last we checked, there were no recessions in 1985, 1995 or 1998. ISM's report even says that while manufacturing has hit a soft patch, the numbers are still consistent with a broad economic expansion.

Exhibit 1: ISM Manufacturing PMI

Source: Federal Reserve Bank of St. Louis, as of 2/1/2016. ISM Manufacturing PMI, January 1948 - January 2016.

The consumer spending report also pretty handily debunks much of the coverage. Not adjusted for inflation (actually deflation, since the Personal Consumption Expenditures Price Index fell -0.1% m/m), total spending fell $700 million, which the Commerce Department calls unchanged and headlines call a small loss. But when price changes factor in, that tiny drop flips to a 0.1% gain.[i] Which is not fantabulous, but also isn't a drop. Spending on goods slid a smidge in real and nominal terms, but spending on services made up for it-up 0.4% in nominal terms and 0.3% in real terms. That isn't fishing for obscure data points, either: Services are nearly 68% of consumer spending. It's by far the biggest chunk, and it's driving growth. This is good, not bad.

These two stories illustrate why we always encourage readers to look beyond the media coverage of economic data and get it straight from the horse's mouth, where it isn't cherry-picked to fit a certain narrative. Don't outright ignore the headlines, as they can help you measure sentiment, but don't forget to fact-check. When you find the bits most articles omit, you can get a more complete picture and discern the gap between sentiment and reality.

Stocks move on that gap, and right now, it's bullish. Financial media reflects and influences sentiment, and right now it's in a gloomy cycle. Reality is much better, and it won't take much to stay that way. Just modest growth should be enough to help stocks keep grinding higher.

[i] In case you are curious, excluding energy, real PCE grew +0.2% m/m.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 4 - May 82026-05-11

-

Expert Commentary 3 Things You Need to Know This Week | April CPI, Prediction Markets, Financial Fraud2026-05-11

-

Politics UK Stocks and the Starmer Scuttlebutt2026-05-08

-

Expert Commentary This Week in Review | Tariff Update, National Debt Concerns, April Jobs Data

2026-05-08

2026-05-08

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today