Personal Wealth Management / Market Analysis

Divid-ENDing

Some high-profile dividend cuts illustrate the danger of chasing yield.

All analogies are bad analogies, but here's one anyway: If you're going to chase something, make sure you're chasing a thing that you can actually catch and keep. Not something that can vanish and leave you empty-handed. For instance, many investors love chasing yield-REIT yields, master limited partnership (MLP) yields, high bond yields and shiny high dividend yields. REITs, MLPs, junk bonds and high-dividend stocks have plenty of points in their favor[i], and all can add value at times. But buying any security for its yield alone is a fool's errand. Dividends aren't carved in stone. For the latest proof, look no further than a wave of dividend cuts in Energy and Materials, which is quickly erasing one of the few positives commodity bottom-fishers could cling to.

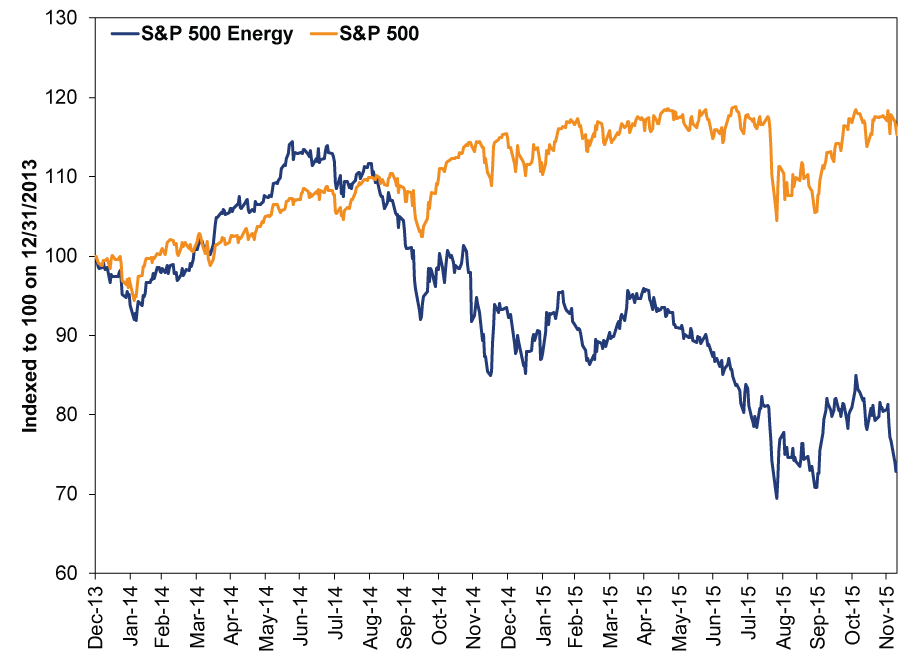

Here is a picture of what Energy stocks have done since last year.

Exhibit 1: Energy Takes a Beating

Source: FactSet, as of 12/9/2015. S&P 500 Energy and S&P 500 Total Return Indexes, 12/31/2013 - 12/8/2015. Indexed to 100 on 12/31/2013.

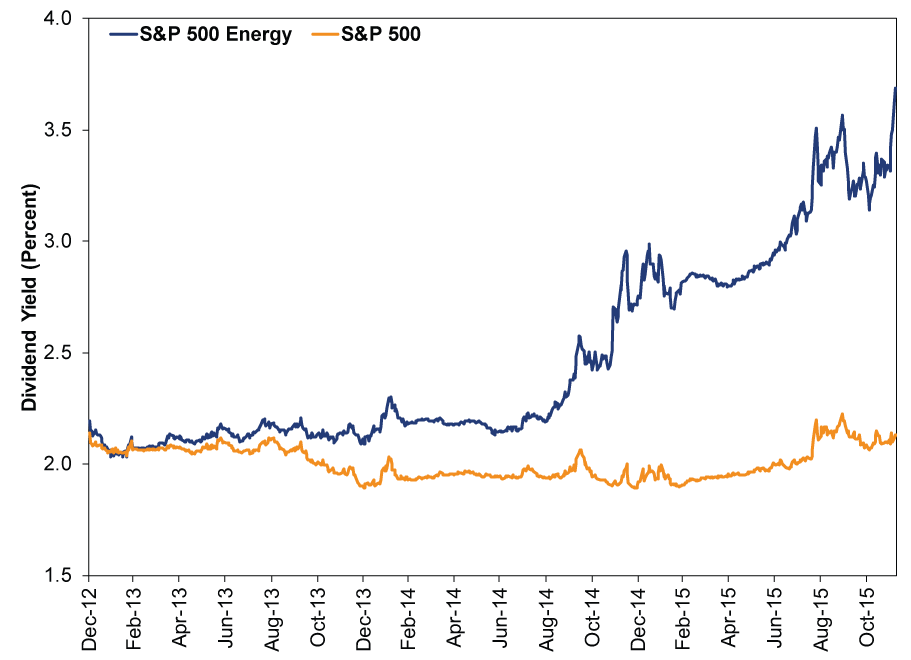

Here is a picture of why many investors still crave them.

Exhibit 2: Energy Yields Win?

Source: FactSet, as of 12/9/2015. S&P 500 Energy and S&P 500 dividend yields, 12/31/2012 - 12/8/2015.

Materials are largely in the same boat, albeit to a smaller degree-down, though not as much as Energy, and with a modestly higher dividend yield than the S&P 500.

For many, these high yields are supremely attractive. At a time when 10-year US Treasurys can't crack 2.5% and European yields are stuck below 2%, high dividends in certain equity sectors seem like a wonderful solution for investors who fall into the "yield is the only way to generate investment cash flow" trap. (And it is a trap-see this.) But they aren't. We love a good dividend as much as the next guy and gal, but dividends are unreliable. When companies get in trouble, dividends are often the first thing to go. We saw this in 2008, when Financials dividends evaporated. And now we are seeing it in Energy and Materials, where a dividend bloodbath escalated this week. Here is the casualty list thus far:

Kinder Morgan cut its dividend by 75% on Tuesday, from 51 cents a share to 12.5 cents. This will drop its dividend yield from 12.5% (which, as The Wall Street Journal noted, exceeded a Greek 10-year bond yield) to about 3%.

Anglo American scrapped its dividend on Tuesday. It had paid 85 cents a share, which before Tuesday represented an 8.5% yield.

Freeport-McMoRan suspended its dividend on Wednesday. It had been yielding 3%. Now it will yield nothing, and it has lost nearly 70% of its market value this year.

Energy and Materials dividend cuts are hogging attention now, but they aren't a new phenomenon. Italian oil company Eni SpA shaved nearly 30% off its dividend in March. Glencore suspended its dividend in September and issued a bunch of new stock, erasing yield and adding insult to injury by diluting existing shareholders. Oil driller Chesapeake Energy scrapped its dividend in July-a "watershed" moment for a company that kept its payout intact throughout 2008's financial crisis.

It seems fair to say more cuts will follow. Some firms have done all they can to get lean and mean without stiffing shareholders, cutting investment and scrapping planned projects but protecting dividends. But that was when oil prices were higher, in the $40s and $50s. Now they are below $40, and if they stay there, many firms will have to re-reevaluate their plans. Yes, existing oil wells remain cost-effective in many American fields, most notably the Permian Basin. But falling prices hit revenues any way you slice it, and many firms globally will likely need to hunker down as the supply glut slowly corrects.

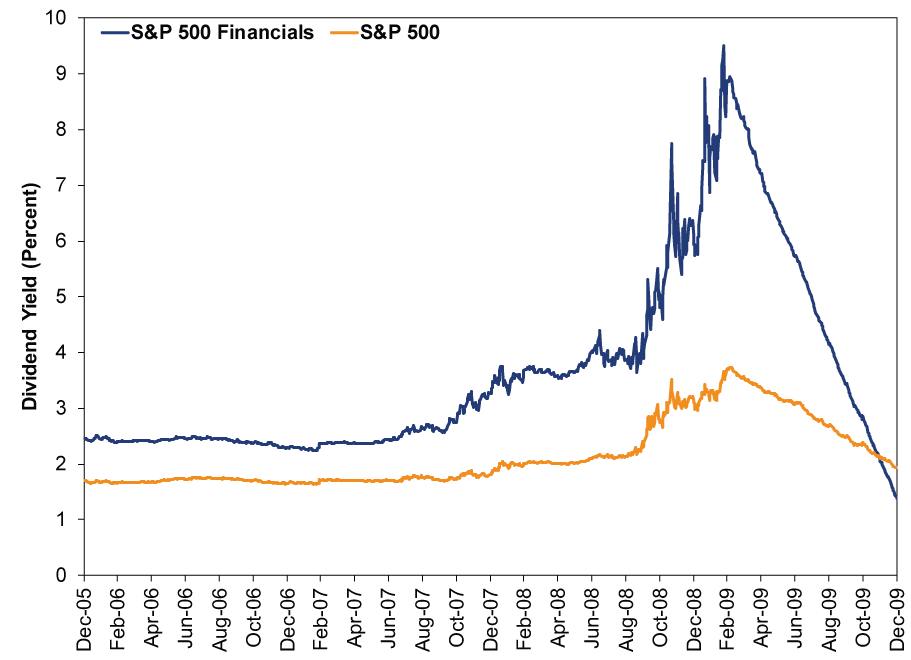

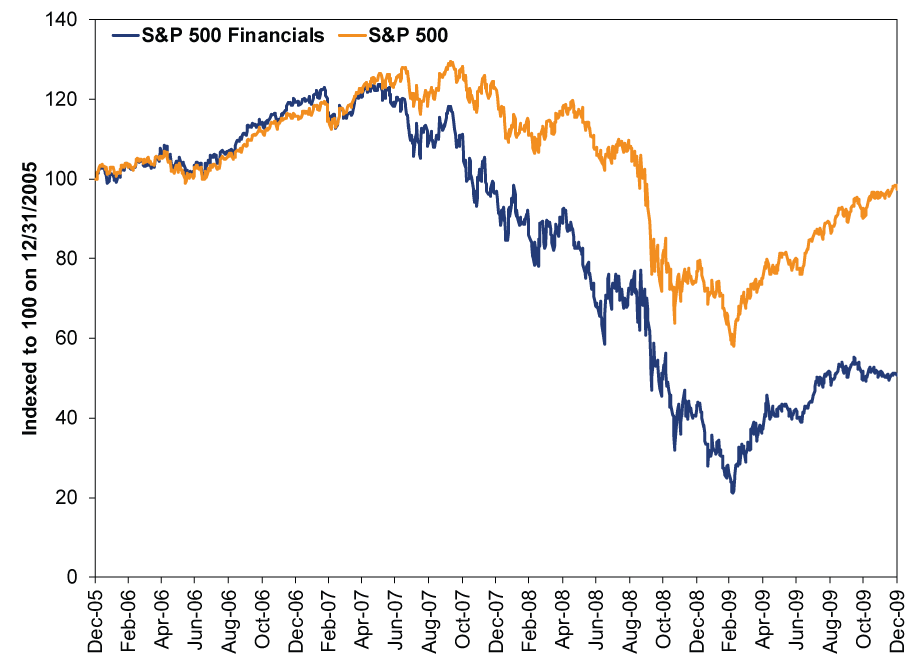

The fact that so many oil firms yield near 10% underscores this. Dividends might feel like free money, but like any investment return, they are compensation for risk taken. High dividend yields signal high risk-the risk the next dividend won't get paid. It isn't unlike a high bond yield. Markets drive bond yields higher when they require a greater reward for higher risk. It's often the same with a dividend yield. There is always a tradeoff between risk and reward. Exhibits 3 and 4 should erase any lingering doubt otherwise.

Exhibit 3: The Sad Tale of Financials Dividends ...

Source: FactSet, as of 12/9/2015. S&P 500 Financials and S&P 500 dividend yields, 12/31/2005 - 12/31/2009.

Exhibit 4: ... and Financials Stocks

Source: FactSet, as of 12/9/2015. S&P 500 Financials and S&P 500 Total Return Indexes, 12/31/2005 - 12/8/2009. Indexed to 100 on 12/31/2005.

Chase yield at your peril. Again, high-dividend stocks have their time and place. So do Energy and Materials stocks. But unless you invest for total return and weigh the fundamental pros and cons carefully, you could overlook big risks. Freeing yourself from the shackles of yield will expand your options and, most likely, give you a better shot at reaching your long-term goals.

[i] Except for nontraded REITs, which have no points in their favor, in our view.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today