Personal Wealth Management / Market Analysis

Does Kris Kringle Make Stocks Jingle?

Whether or not stocks rise around the holidays isn't important or predictive.

Some believe this gentleman brings cheer to Wall Street. Photo by Blend Images - Kidstock/Getty Images.

Stocks have been choppy lately, with markets more or less flat this month, as volatility continues since last summer and fall's correction. All the wobbles during the holiday season may make it seem like Santa Claus is giving investors a lump of coal instead of the merry market returns many believe normally come this time of year. And some suggest this is a bad omen for 2016-if stocks can't rally during a typically happy period, what happens next? But is the so-called Santa Claus rally really a thing? And do down markets so far this holiday season portend trouble for stocks going forward? In short, no and no. Seasonal impacts on stocks are as fictional as Santa[i] himself, and whether or not the year closes on a high note tells you nothing about future returns.

Before we dive into the data, let's consider that like Sell in May, the Santa Claus Rally has several different time period definitions. The term was coined by Yale Hirsch in 1972 in his Stock Trader's Almanac. Hirsch suggested stocks tend to perform especially well in the last five trading days of December and the first two of January. Others consider the Santa Claus rally to be the last two weeks of the year or even the entire month of December.

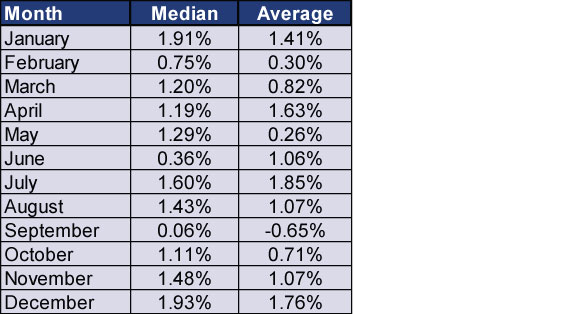

So let's explore what the data actually show. Since 1926, the S&P 500's average total return (price plus dividends) is 1.76% in December-big by comparison to other months, but not overly so.[ii] July's average return is higher. And December's big returns have some slight upward skew from huge bounces in 1991 (11.4%), 1971 (8.9%) and 1987 (7.6%). Yet two of the three periods (1991 and 1987) occur in the typically steep climbs of early bull trends. We are skeptical Saint Nick was the bullish factor causing a pop. Strip out these three years and average December returns fall to 1.50%, in line with average returns for August and November. (Exhibit 1) The median return similarly suggests December is a good month, but January's median return is statistically indistinguishable.

Exhibit 1: Average and Median Monthly S&P 500 Returns

Source: Global Financial Data, as of 12/23/2015. S&P 500 total return, 12/31/1925 - 12/31/2014

December has been positive in 67 of 89 years since 1926, a frequency of 75.3%. That is above the all-month frequency of positive returns (62.3%), but it is only a hair over the frequency of positive years, suggesting you are better off not flipping in and out of stocks on a monthly basis.

Some suggest, though, that Santa comes to Wall Street only during the final two weeks of the year. And the numbers bear it out! Since 1928, the S&P 500's median price return for all two-week rolling periods is 0.49%, while the median return for the last two weeks of December is 0.97%.[iii] But before you proclaim your belief in Santa vindicated, consider that this doesn't mean investors can count on especially big two-week returns beginning every mid-December-returns were negative during this period in 18 years.

The same logic applies to how stocks perform during Hirsch's seven-day definition of a Santa rally (again, the last five trading days of December and the first two of January). Since 1928, the S&P 500 price index's median gain for the seven-day Santa period is 1.7%, again higher than the 0.4% median for all rolling seven day periods.[iv] However, Santa has delivered a lump of coal[v] on 20 occasions-including 2014's Santa period, so this isn't some ironclad recipe to load up on stocks.

If you want to keep believing in Santa, here is your trigger warning/spoiler alert: Stop reading here. Ultimately, whatever the numbers say, the theory behind the Santa Rally suffers from a fatal flaw: It is statistical correlation without fundamental causation. Trivia. Some theorize markets soar this time of year because many invest their year-end bonuses, or because short-sellers are on vacation or even due to fund managers buying stocks that have performed well to make portfolios look good ("window dressing"). But this seems like searching for meaning in holiday times, as none of these explanations seem anywhere near big enough to materially impact a roughly $18 trillion market.[vi] If there are no fundamental reasons why stocks perform better towards year-end (or any period of time), then the fact they do is likely just a statistical aberration and is in no way a forecasting tool for any particular year-end period. Besides, if you're a long-term investor, it doesn't matter whether bursts of outsized returns come during the holiday season, the end of winter or the dog days of summer. That is particularly true if you are already invested with an eye on your longer-term goals.

Still, with December posting not-so-hot returns thus far, some who believe the Santa rally is more than just a statistical quirk suggest stocks' Grinch-y demeanor during the this joyous, allegedly bullish time bodes ill for 2016. After all, they claim using Hirsch's definition, Santa has failed to deliver a rally only four times in the last two decades, and the market was flattish twice and down twice.

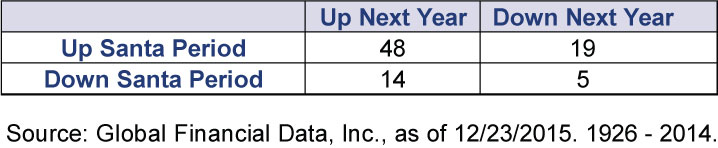

But looking at market returns over a longer time period suggests the lack of a Santa Claus rally doesn't predict poor future returns all that well. You need only go barely beyond those 20 years-to 1992, when stocks slipped -1.1% during the Santa period, but rose 10.1% the next year-to find a false read.[vii] And there are a slew of other instances where the lack of a Santa rally did not accurately forecast swooning or even flat stocks over the coming year. Stocks fell -0.6% during the 1984/85 Santa period, but then rose big in 1985.[viii] As Exhibit 2 shows, stocks rose in 62 of 86 total years since 1928, or 72% of the time. When the Hirsch-defined Santa period is up, stocks rose in 48 of 67 periods-71.6%. Of the 19 completed full calendar years following a negative Santa period, stocks rose in 14-73.6% of the time. (This year could go either way as of this typing.) There isn't anything predictive about this timeframe-true of past returns categorically.

Exhibit 2: Santa Claus Rallies or Dips Are Not Predictive

So whatever happens in the next few trading sessions, it is a mistake to believe seasonal patterns exist or predict. Stocks move on fundamentals, not calendars. Short spans aren't any more or less bullish than others, and they certainly don't tell you what's to come. Heck, because markets efficiently discount all widely known information, even if there were seasonal trends, investors would likely buy in advance, moving their effects up in time, eliminating them. Taken to its extreme, this could imply the Santa Claus Rally coming in July. Hey! Maybe that's why July is the best month! (We kid.)

[i] Please don't let your children read this sentence.

[ii] Source: Global Financial Data, Inc., as of 12/23/2015. S&P 500 monthly total returns, 1926 - 2014.

[iii] Source: Global Financial Data, Inc., as of 12/23/2015. Median 10-trading day return for the period 12/31/1927 - 12/22/2015 and final two weeks of the calendar year.

[iv] Ibid, median 7-day returns for the period 12/31/1927 - 12/22/2015 and Hirsch's seven-day periods starting in 1928 and ending 1/5/2015.

[v] Negative returns.

[vi] Especially fund managers dressing up portfolios with winners because they would likely be selling underperforming stocks as well.

[vii] Source: Global Financial Data, Inc., as of 12/23/2015.

[viii] Source: Global Financial Data, Inc., as of 12/23/2015.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today