Personal Wealth Management / Market Analysis

Don't Believe the Energy Hype

Energy stocks have outperformed lately, but they still face many headwinds.

Is it time to jump into Energy stocks? After suffering alongside oil prices since mid-2014, Energy stocks have crushed the S&P 500 since late January, leading many to wonder if Energy's bloodbath is finally over and investors should hop on the bandwagon. If you're among those tempted, stay cool: Frenzies are rarely worth following, and fundamentals aren't on Energy's side. Energy's time will come, but we don't think it's here yet.

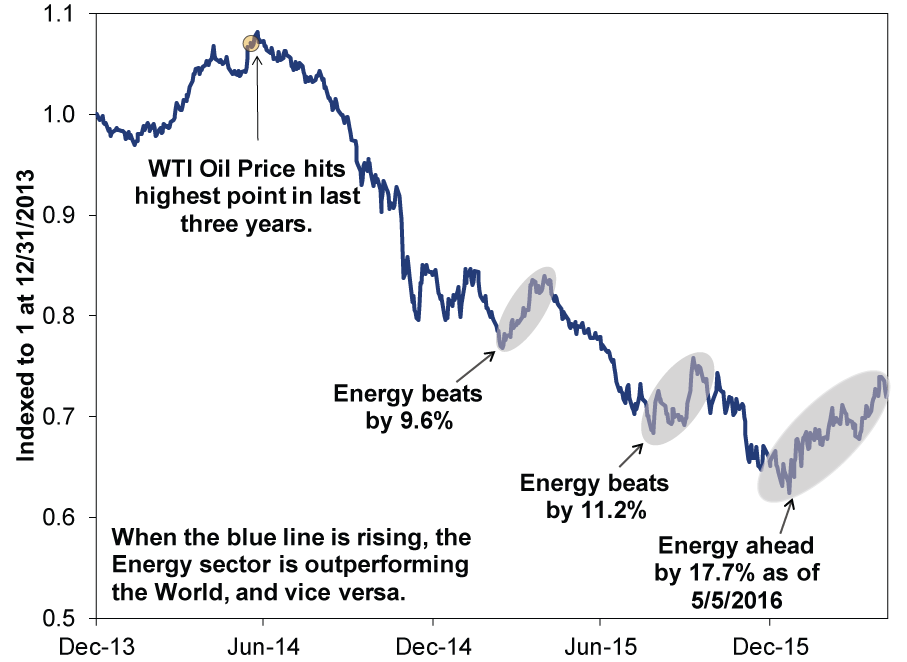

Most Energy firms' earnings and revenues depend on oil prices, which are up over 50% since January, fueling the hope and hype. But oil has had false dawns before, and this isn't Energy's first market-beating stretch since mid-2014 (Exhibit 1). Those runs proved to be short-term countertrends, and this one quite likely follows suit.

Exhibit 1: Energy Countertrends Are Normal

Source: FactSet, as of 5/6/2016. MSCI World Energy Sector divided by MSCI World Index, 12/31/2013 - 5/5/2016. Returns include net dividends. Shading indicates periods of Energy outperformance exceeding 8%.

In both crude oil and Energy stocks, investors seem far out over their skis. Both are moving on hopes global oil production will soon fall, rather than any reasonable likelihood that it actually does. Yes, US production began falling in mid-2015, and some OPEC members have jawboned about freezing output. But for now, world output is still at record levels and well above demand.

According to the International Energy Administration, global oil supply totaled 96.1 million barrels/day in March, exceeding demand of 94.8 mb/d. That surplus doesn't appear likely to vanish soon. US producers have shut down the least efficient wells, but technological advancements let firms produce more from many other existing wells. Plus, a sizable backlog (or "fracklog") of shale oil wells have been completed but not yet hydraulically fractured. When prices rise, firms can lock them in via futures contracts, complete the wells and begin pumping.

Elsewhere, oil-reliant countries like Russia and Brazil have boosted output because government revenues rely on oil rents. The lower prices fall, the more they must pump just to maintain revenue and public spending. While Russia and some OPEC nations discussed freezing output at current levels, conflicts of interest thwarted them. Iran wants to rebuild market share after years of Western sanctions, and Russia and Saudi Arabia said they won't freeze unless Iran does. And even if they do, a freeze isn't necessarily an outright cut-production from these countries would remain at very high levels.

Oil cycles often turn much more slowly than many presume-it frequently takes years due to new production's high costs and long lead times. After spending billions to find and tap new supply, firms can't turn off the spigots just because prices have cratered. They must recoup costs. So they pump, while cutting exploration to reduce costs, laying the groundwork for lower output and higher prices in the future. That's about where we are now. Investment in exploration and new wells has already cratered in the US, UK and elsewhere. As more mature wells taper off, output should naturally fall. But it will take time, particularly once you account for Russia and OPEC.

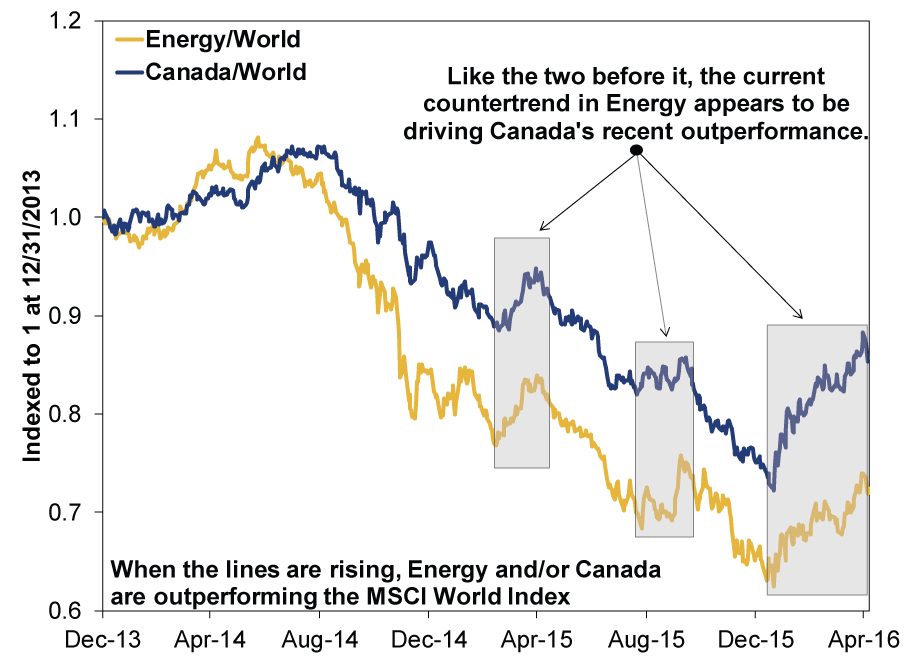

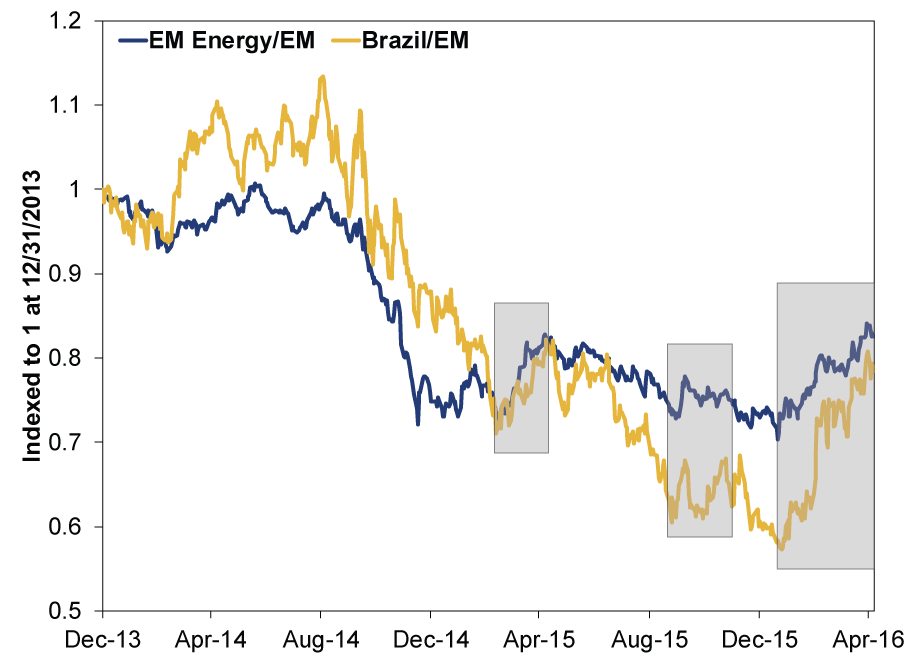

That means other oil-related rallies likely fizzle sooner rather than later-like big bursts in Brazilian and Canadian stocks. Both are highly correlated to commodities, as natural resources stocks account for a huge slice of market capitalization. Both have underperformed the world since mid-2014, yet both have enjoyed brief bursts of outperformance in sympathy with Energy's countertrends.

Exhibit 2: Canada and Energy Are Strongly Correlated

Source: FactSet, as of 5/6/2016. MSCI Canada divided by MSCI World Index and MSCI World Energy Sector divided by MSCI World Index, 12/31/2013 - 5/5/2016. Returns include net dividends.

Exhibit 3: Brazil's Countertrend Rallies Also Track Energy's

Source: FactSet, as of 5/9/2016. MSCI Brazil divided by MSCI Emerging Markets, 12/31/2013 - 5/5/2016.Returns include net dividends.

Other variables matter too, but without a sustained recovery in commodity prices, these countries likely won't be able to maintain outperformance. If the resource rally fails to gain traction, and prices resume sliding, Brazilian and Canadian stocks may falter as well.

Eliminating any major category from your portfolio creates a risky blind spot and reduces diversification, so we don't think it's wise to ignore Energy entirely. But we think it's best to limit exposure to the biggest integrated oil and gas producers. They have stronger balance sheets and are hurt less by low oil prices. Some business units benefit when prices are low, cushioning the more vulnerable units. Also, with deep pockets, these firms can easily acquire assets from small distressed producers. Let them do the bottom-fishing for you as the industry consolidates.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News In Orbit? On Tech Sentiment and IPOs2026-05-22

-

Market Analysis Global Bond Calamity Calls for Calm Perspective2026-05-22

-

Expert Commentary This Week in Review | UK Politics, Fed Developments, IPOs

2026-05-22

2026-05-22 -

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today