Personal Wealth Management / Economics

Don’t Fret the Q1 US GDP Slowdown

While growth was slow in Q1, it isn't a harbinger of worse to come.

The US economy grew just 0.5% (SAAR) in Q1, missing expectations of 0.7% and triggering all sorts of handwringing in the financial press. Slowest pace of growth in two years! Biggest drop in business investment since the recession! Consumers still not spending their gas savings! Far be it from us to try to sugar coat any of this, as it surely wasn't a great quarter, but it also doesn't mean much for stocks. This entire bull market has occurred against a backdrop of below-average growth, so a sluggish quarter is just more of what stocks have enjoyed for about seven years now. Moreover, the Q1 GDP report is a flawed view of economic activity that stocks have already lived through, priced in and moved beyond. Stocks look forward, not backward, and Q1's so-so results have no bearing on future growth.

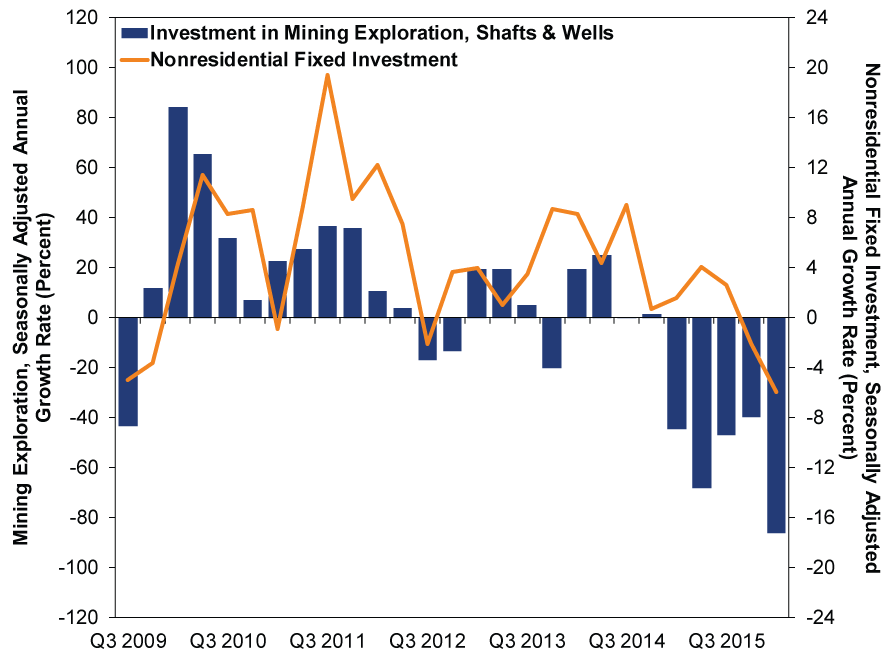

Though growth slowed across almost all categories, many focused on the -5.9% drop in business investment-a plunge on par with the last three recessions. Considering swings in business spending tend to drive economic cycles, the jitters are understandable. But falling business investment isn't always a harbinger of recessions. While it's unusual for business investment to fall this much during an expansion, it isn't unprecedented. In Q1 1987, business investment fell -9.1%, but no recession came. Sizable one-off drops also occurred in 1967, 1956, 1952 and 1951-smack in the middle of economic expansions. There is a strong reason to believe this drop should prove to be a blip, not a sign the broader economy is about to go kaput: Once again, the cratering Energy industry bears a lot of the blame. Investment in mining structures-which includes oil wells-fell -86%, the worst reading ever. That one category detracted -3.4 percentage points from business investment, making it responsible for more than half the drop.

Exhibit 1: Mining's Drag on Business Investment

Source: Bureau of Economic Analysis, as of 4/29/2016. Investment in Mining Exploration, Shafts and Wells and Nonresidential Fixed Investment, Q3 2009 - Q1 2016.

The widely known manufacturing pullback-a global phenomenon-also played a role, judging by the weakness in components tied closely to heavy industry, like transportation and industrial equipment. Meanwhile, categories tied more closely to the service sector held up much better-investment in computers and software rose. R&D spending rose as well, which would be odd if firms were broadly cutting back in anticipation of tough times. If you're retrenching, you probably don't plow money into long-term projects that may or may not pay off years down the line. You focus on the now and get lean and mean.

At some point, Energy's impact should wane, making strength elsewhere more evident. Quarterly investment in mines, shafts and oil wells has fallen -70% since Q3 2014. Energy is now a smaller part of the economy than it was before oil's big drop. If shrinking Energy didn't throw the overall economy into recession by now, with Energy investment now at a much lower base, the chances it suddenly tips the US into recession from here seem slim.

Business investment didn't monopolize the punditry's disappointment. Consumer spending also got some attention, as its 1.9% growth was the slowest in a year, and spending on durable goods fell for the first time since 2011. Some say this is evidence consumers are not spending their savings from cheaper gas elsewhere. And hey, maybe they're right! It was always questionable whether vastly cheaper energy costs would much boost non-energy spending. Saving them and paying down debt were viable alternatives. More importantly, consumer spending has been quite variable during this expansion. It has bounced back from slow quarters before, and there is no reason to believe a longer slowdown must be in order now. But even if consumer spending doesn't reaccelerate, stocks have already proven they can do fine if people aren't spending like crazy.

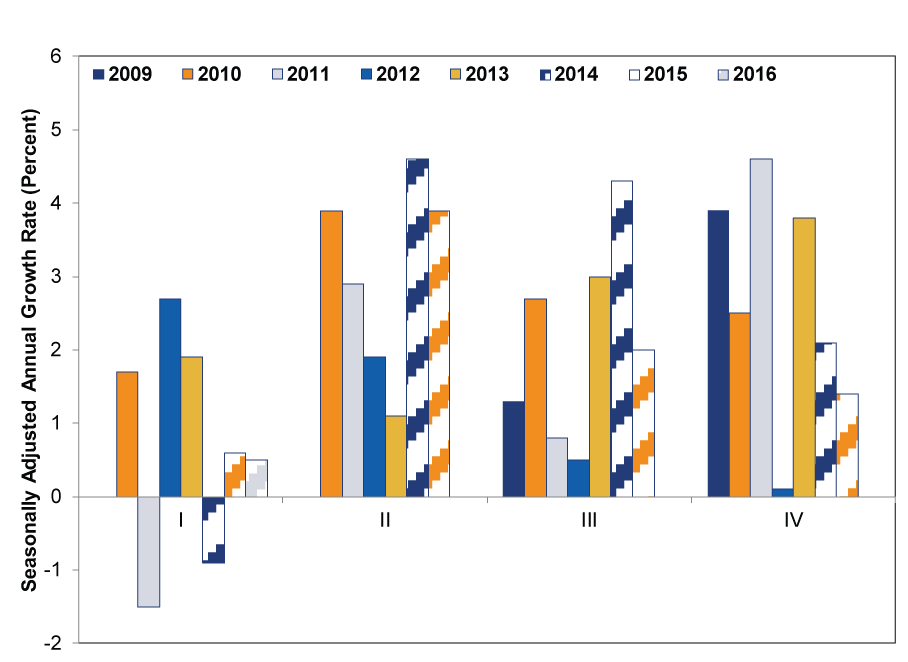

As for the broader growth rate, we can't help but wonder if there are some lingering issues with seasonality. Even after the BEA tweaked their seasonal adjustments to account for a long string of Q1 growth being noticeably weaker than other quarters, there is still a definite trend.

Exhibit 2: GDP by Quarter

Source: Bureau of Economic Analysis, as of 4/29/2016. GDP, seasonally adjusted annual rate, Q3 2009 - Q1 2016.

Who knows if their new methodology more accurately gauges Q1 growth. This is also just the first estimate, based on incomplete data. It will be revised several times and may end up higher (or lower).

Regardless of revisions, stocks are forward-looking and have long since moved on. This is the end of April. The GDP report covers January, February and March. Stocks have already lived through that and are looking toward the future. The GDP report is merely a late-arriving post-game recap, and an imperfect one at that. For stocks, what matters is how the economy does over the foreseeable future, and how that squares with expectations. Most suspect growth will pick up over the balance of the year, though not by much. With the Leading Economic Index high and rising, money supply growing nicely, loan growth fast and other forward-looking indicators pointing positively, growth should continue.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 25 - May 292026-06-01

-

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today