Personal Wealth Management / Market Analysis

Don’t Let the House’s Tax Plan Tax Your Nerves

A firsthand look at how even tax cuts create winners and losers—a big reason tax changes lack meaningful market impact.

They say life’s only certainties are death and taxes, but we’d add a third: Politicians endlessly debating taxes. This is why we were half-tempted not to write up the House GOP’s shiny new tax proposal for you, dear readers: As much as there is to discuss, the likelihood tax reform happens exactly as this bill envisions is somewhere between zero and close-to-zero. Senate Republicans are set to release their own plan in the next week or two, and both chambers will probably tear into each bill during the legislative process. The final tax bill—if it even gets that far—could have little resemblance to what the House released. And, of course, even that would be subject to debate and change. Hence, we caution anyone against thinking any of this is likely to come to fruition. But what we can do now is use this proposal to illustrate why neither tax hikes nor tax cuts have a predetermined economic or market impact. Simply exploring the fact that all tax changes—whether advertised as hikes or cuts—create winners and losers can help investors understand why there is never much material market reaction. So let’s dive in.

As you have probably seen from the media’s deluge of coverage, the House’s tax plan aims to cut corporate tax rates, adjust the incentives for US-based firms with operations overseas, and streamline the personal income tax code. The corporate tax rate would fall from 35% to 20%, below the international average, but most of the deductions firms use to avoid paying that 35% rate would go away. So-called “pass through” corporations, which includes most small businesses, would see their headline tax rate drop from 39.6% to 25%. Taxation of most foreign profits would cease, replacing the bizarre system where firms pay foreign taxes up-front and defer US taxes until they repatriate the profits. In theory, that removes the incentive to park cash overseas, helping money move more freely. But it isn’t a free lunch: Firms’ “high-profit foreign subsidiaries” (whatever that means) would face a 10% tax.

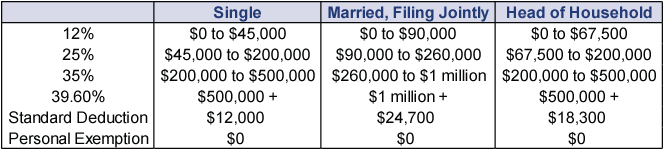

The personal income tax changes are more complex. Essentially, they reduce the number of tax bands from seven to four, eliminate most itemized deductions, nearly double the standard deduction, and remove the personal exemption. To save three thousand words, here are three pictures.

Exhibit 1: Current Personal Income Tax Brackets

Source: Tax Foundation.

Exhibit 2: Proposed Personal Income Tax Brackets

Source: House of Representatives.

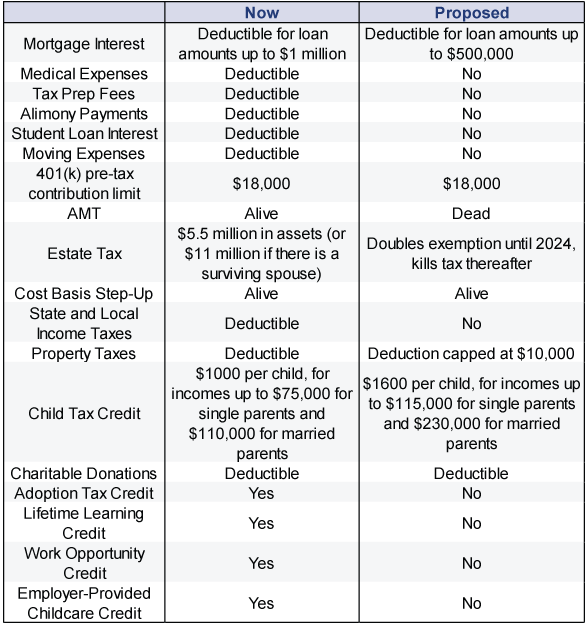

Exhibit 3: Proposed Changes to Itemized Deductions and Credits

Source: Tax Foundation and House of Representatives. The 401(k) contribution limit will increase to $18,500 next year. The point in this table is the bill doesn’t seek to change that.

Some popular itemized deductions are on the chopping block. The biggie: Deduction of state and local income taxes (SALT). Fiscal conservatives have long argued these deductions aren’t efficient or fair, as they essentially force low-tax states to subsidize California, New Jersey, Oregon, Illinois and all the rest. End the deductibility, they argue, and it incentivizes governments in high-tax states to streamline their books. Philosophically, that might make sense. But it doesn’t change the fact that workers in high-tax states benefit from the deduction and could be worse off if it ends, depending on what other itemized deductions they take. The bill’s proponents argue doubling the standard deduction and reducing the tax rate that most income will be subject to should make up for the SALT deduction, but this is oversimplified. Should this “tax cut” pass as-is (again, far from assured!), many taxpayers in high-tax states will pay more, not less.

Adding insult to injury for folks in high-income-tax states, the House’s plan would partly preserve the property tax deduction. This is also a case of picking winners and losers, as many income tax-free states—most notably, Texas—make up the difference with high property taxes. They are technically high-tax states, but we guess the House Ways and Means committee has decided this is a more socially acceptable form of high taxes, and one the rest of the country should subsidize.

There are some other contentious wrinkles, as the above tables show, but the SALT issue shows why there is so much grumbling over these tax “cuts.” For some households, they will probably be stealth hikes masquerading as “cuts.” It’s human nature for losers to feel the pain of that loss more than winners enjoy a similarly sized gain, and this emotional reaction can weigh on sentiment. This is why it isn’t a foregone conclusion that big tax cuts would lift investor sentiment and stocks. The reality is just too mixed—a big reason tax “cuts” aren’t inherently wonderful for stocks. Not that they’re bad. Rather, they’re just sort of there.

As for corporate taxes, while the rate cut sounds big, don’t overrate corporate tax changes as an economic or investment driver. Enduring tax reform could have an impact, as predictable tax rates raise the incentive for businesses to make long-term investments. But it is hard to see anything that might pass now having permanence. While the corporate tax rate is “permanent” in the sense that it doesn’t have a preset expiration date, Congress has already laid the groundwork to pass the final tax bill with a simple majority. Anything passed along party lines, by a vote or three, is quite easy for the other party to undo whenever they take power. If businesses don’t have confidence the lower rate will stick, it’s an incentive to make hay while the sun shines: make short-term investments that pay off before the next administration comes in, rather than long-term investments that pay off far in the future and will be subject to some unknowable tax rate.

Our view of potential tax changes is different than most others’ opinions. As you might have gleaned from the SALT handwringing, tax debates can stir uncertainty. The House’s proposal has done this to an extent, and it wouldn’t surprise if the Senate’s eventual plan stirred up another round. Uncertainty probably lingers throughout the debates, amendments, votes and reconciliations. Just getting past the debate, regardless of the final bill and whether it passes, would probably help investors get more clarity. Even if you don’t love whatever Congress does, at least you know the lay of the land. That enables you to get on with it and plan.

As for your personal finances and the tax plan’s potential impact, it’s too early to get worked up with cheer or fear. Again, this is just one proposal. The Senate will have another. Then we’ll likely have a flurry of amendments as special interests chip away at it, as they always do. Intraparty gridlock should also help water down the tax changes. While high-income-tax states have mostly Democratic governments, they do have Republican representatives in the House, and these folks probably want to get re-elected next year. Erasing their constituents’ tax goodies would be a really poor campaign strategy. So stay cool, be patient, and wait to see how these political pressures shape this bill over time.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today