Personal Wealth Management / Market Analysis

Don’t Yield to Pound Paranoia

The falling pound and rising Gilt yields don't threaten UK growth.

Last week, UK business news was jammed with scary-sounding headlines: The pound dropped further; inflation hit a two-year high amid laments of squeezed consumers; and spiking Gilt yields sparked concerns that UK debt will grow unaffordable. Brexit (maybe even a hard Brexit!) figured into each story-to us, with little justification. Movements in sterling, inflation and Gilts all have relatively benign, non-Brexit forces behind them, but aren't reasons to worry regardless. While higher prices and more volatility in Gilt yields wouldn't surprise, there isn't much evidence either will imperil the UK's expansion, fiscal health or stocks. Moreover, a global portfolio is your hedge against all things Brexit.

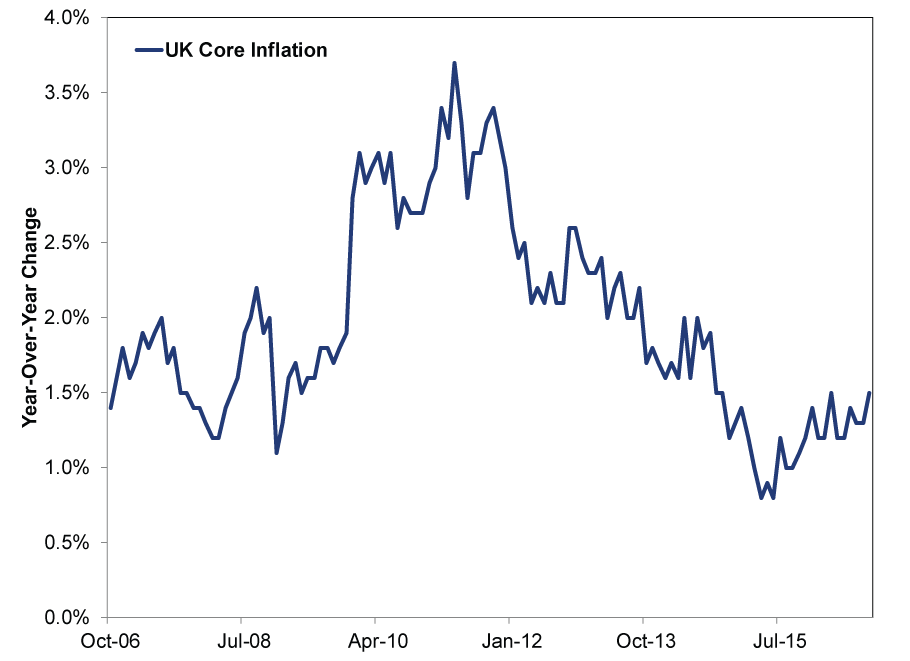

The UK's Consumer Price Index (CPI) hit 1.0% y/y in September as clothing and restaurant prices rose-the highest inflation reading since November 2014. Considering people feared deflation mere months ago, you'd think this would be welcome news. But instead, we saw lots of chatter about declining real wages and falling living standards. As ever, context is key. 1.0% y/y inflation is half the BoE's target and well beneath levels seen earlier in this expansion. Exhibit 1 shows September's core inflation numbers-which strip out more volatile categories like food and energy-are far from even recent heights. Higher levels aren't lethal, either-UK consumers didn't reel in the face of prior price increases. The Office for National Statistics notes British household spending has grown every quarter since Q4 2011. Inflation, you see, doesn't drive consumption-most consumer spending is nondiscretionary, so it doesn't sink when prices rise marginally.

Exhibit 1: UK Core CPI - Last Decade

Source: Office for National Statistics, as of 10/18/2016. CPI excluding Food, Energy, Alcohol and Tobacco.

While most agree the weak pound hasn't yet registered much in the data, they fear it'll hit supermarket shelves soon. Now, it's entirely possible prices do tick higher over the next several months: As pre-Brexit currency hedges expire, some importers' costs will rise, and they'll probably try to pass at least some of the burden on to consumers. But it's a leap too far to say this will bring runaway inflation, as supply and demand in the end market, not the seller's costs of production, have the most sway over prices. We saw this firsthand last week, when one conglomerate tried to charge the UK's largest supermarket higher prices for several food items and household goods, including that ever-beloved, ever-polarizing spread, Marmite. Said supermarket refused, citing long-running grocery price wars in the UK-they knew they couldn't competitively charge more, so they simply ceased ordering those goods until a deal (thank goodness) was reached.

Beyond anecdotes, consider Japan: The yen plunged in 2013 and stayed there for two-plus years while inflation hardly budged. The pound's history also proves the currency-inflation link is tenuous: As Exhibit 2 shows, a weak sterling (rising orange line) sometimes does coincide with higher inflation (rising blue line). But it very frequently doesn't. There are many, many more factors than just the currency explaining even the times correlations look tight-like monetary policy, energy prices and macroeconomic events with little connection to either.

Exhibit 2: Sterling vs UK Consumer Price Index

Source: Office for National Statistics, as of 10/18/2016. CPI: All items year-over-year percentage change. Sterling Effective Exchange Rate Index, January 1990 - August 2016.

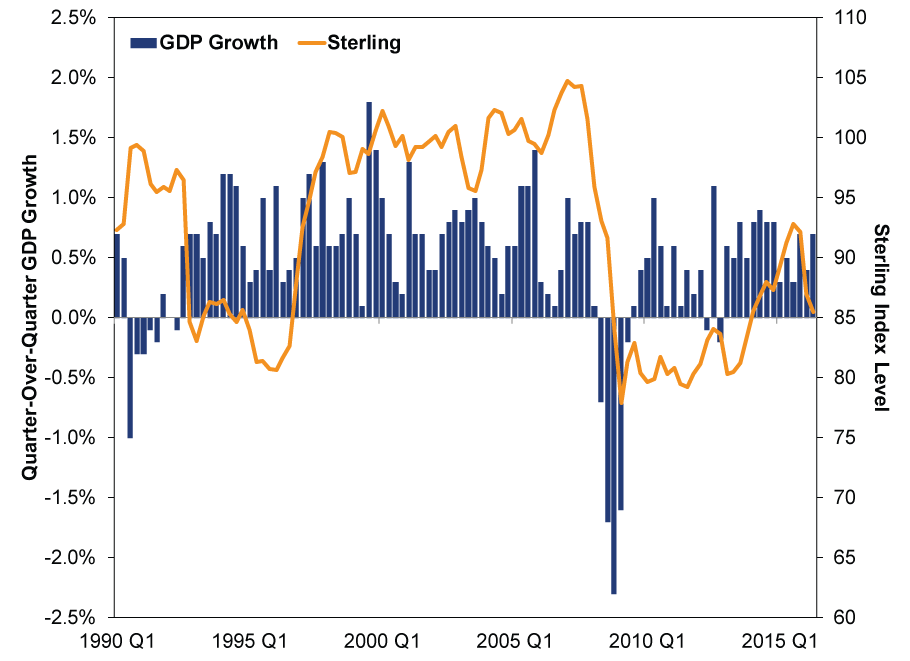

Looking past consumption and inflation, pound fluctuations (as with any currency) create winners and losers, but don't drive growth overall. Exhibit 3 shows the UK has grown and contracted while the pound was both strong and weak.

Exhibit 3: Sterling vs UK GDP

Source: Office for National Statistics, as of 10/18/2016. Bank of England Sterling Effective Exchange Rate Index. UK quarter-over-quarter GDP growth, Q1 1990 - Q2 2016.

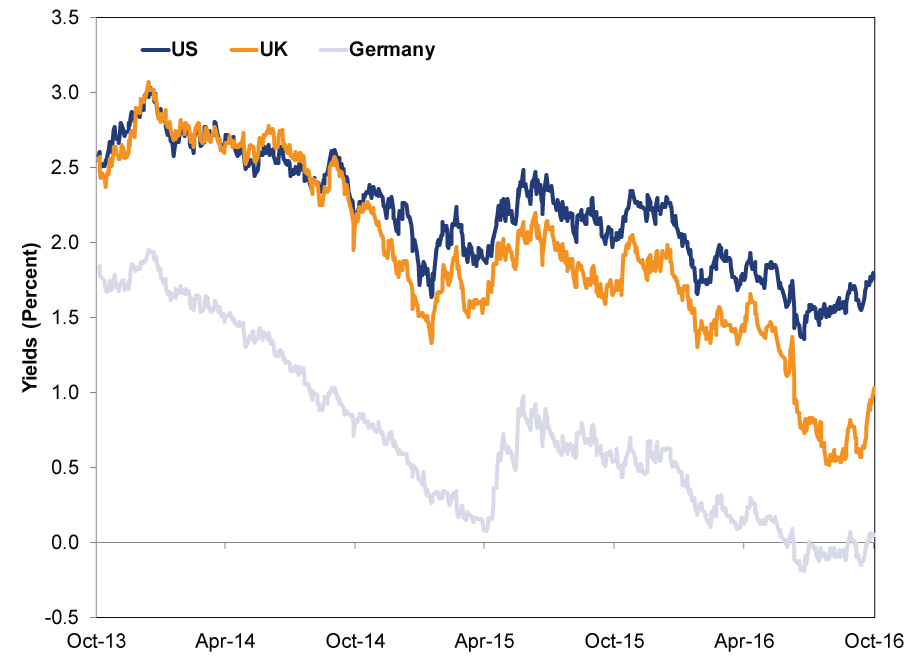

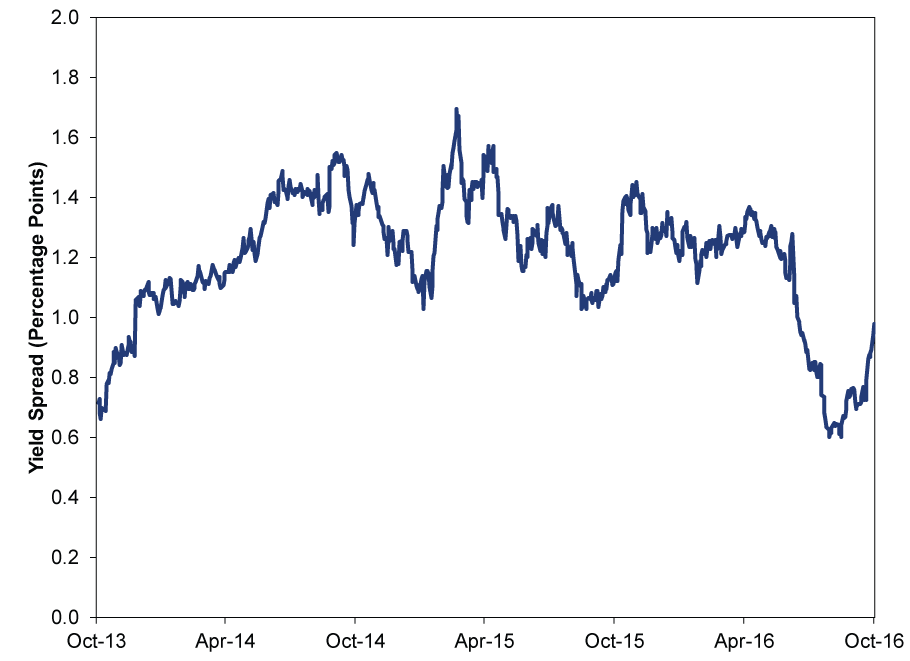

Headlines have also blared about 10-year Gilt yields rising from 0.5% in mid-August to 1.0% today.[i] But this doesn't signal a loss of confidence in the UK economy or render UK debt unaffordable. Here, too, context is key: Rising Gilt yields are part of a global move-just as falling yields were post-Brexit. Exhibit 4 shows UK yields have risen more than US Treasury and German Bund yields, but we wouldn't read all that much into it. Gilt yields fell more than the other two after the vote, and bund spreads are still far below where they were for much of 2014 and 2015. (Exhibit 5) It's a stretch to say markets suddenly see the UK as more of a relative credit risk now.

Exhibit 4: US, UK and German 10-year Yields

Source: Factset. Daily 10-year yields 10/18/2013 - 10/18/2016.

Exhibit 5: UK Minus German 10-year Yields

Source: Factset. Daily 10-year Gilt yields minus 10-year Bund yields 10/18/2013 - 10/18/2016.

Plus, bond markets are volatile-the recent upswing in yields isn't guaranteed to continue. There are forces tugging at yields from both directions, which probably means a lot of sideways bouncing, as we've seen the last few years. Yes, there are some new upward forces, the aforementioned inflation probably being one of them. Here are some others: Chancellor of the Exchequer Phillip Hammond announced recently he won't pursue prior Chancellor George Osborne's (supposedly "austere") deficit targets and may even consider a touch of fiscal stimulus, which perhaps means more borrowing and a modest increase in bond supply. Markets might also be looking to the end of the small emergency QE program[ii] enacted in the wake of the Brexit vote, which is set to expire next February.

At the same time, though, QE continues apace in the eurozone and Japan, and investors' hunger for bonds globally hasn't changed. Developed-world bond markets are highly correlated, making UK Gilts unlikely to break off from the herd and skyrocket. Plus, demand for Gilts is so high these days, the Bank of England recently failed to purchase enough bonds under its QE program. Likewise, when the BoE has attempted to sell some Gilts recently, demand reached record levels. If investors were worried about the UK's solvency, they wouldn't snap up 10-year bonds as fast as they're put up for sale, and they'd ask far more than a percent in return.

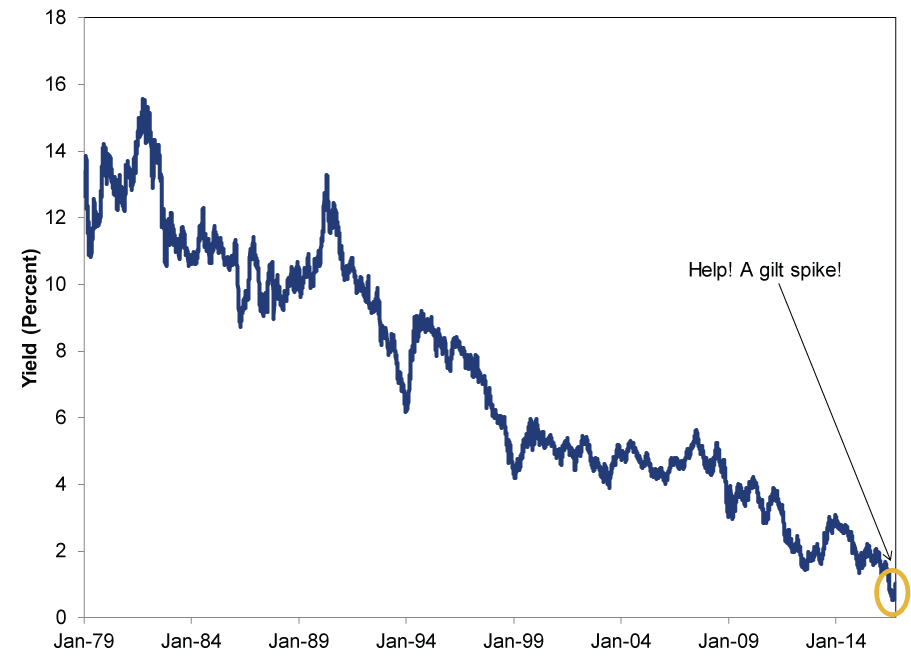

All the talk of which direction Gilts are headed overlooks a stubborn fact-rates a shade above 1% are still near generational lows.

Exhibit 6: Historical Gilt Yields

Source: Factset, as of 10/18/2016. Daily 10-year Gilt yields 1/02/1979 - 10/18/2016

Rising yields aren't an immediate threat to debt service costs, as they only affect future debt issuance. Existing Gilts are unaffected-and most debt maturing now is refinanced at lower rates. Interest payments were just 6.4% of tax revenue in the most recent fiscal year (2015-2016) and are getting cheaper, not more expensive.

Let's not forget a positive of higher Gilt yields, either-Exhibit 7 shows the UK's yield curve is notably steeper than it has been at this point in any month since June 23's referendum-bullish, as it encourages bank lending by boosting profitability.

Exhibit 7: The UK's Steepening Yield Curve

Source: Factset, as of 10/19/2016. UK yield curve (bank rate through 30-year Gilt) on 7/18/2016, 8/18/2016, 9/18/2016 and 10/18/2016.

Ultimately, rising yields and a weaker pound are mildly interesting developments, but lack much market impact-UK debt is perfectly affordable, and rampant inflation doesn't loom. Moreover, in a global portfolio, the UK is a small slice-just 7% in the MSCI World Index. If the Brexit vote's aftermath has you jittery, make sure your exposure reaches around the globe.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today