Personal Wealth Management / Economics

Drilling Deep: How Did Energy Influence US Q4 GDP’s Slowdown?

Digging into US Q4 2015 GDP growth.

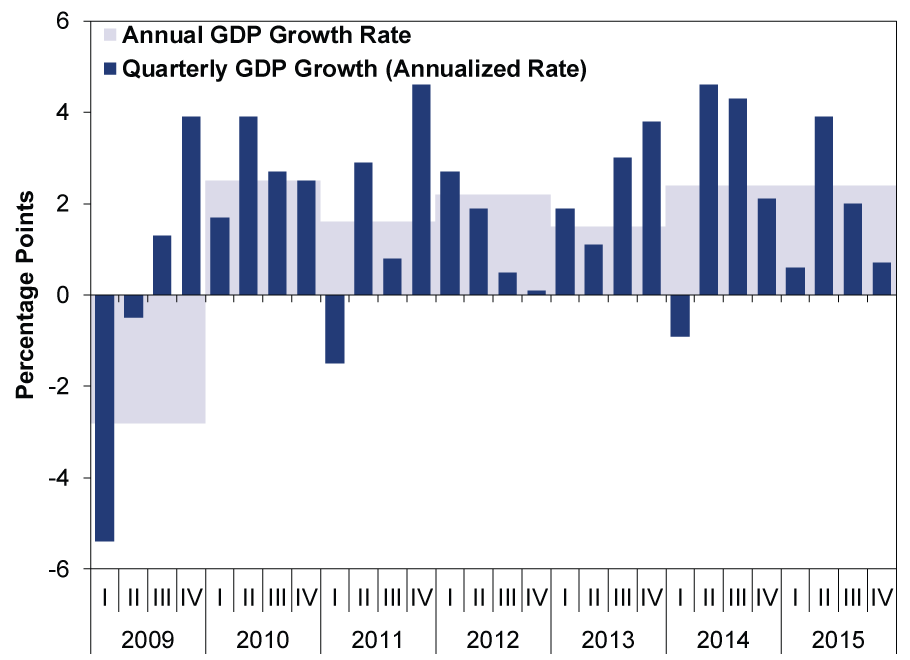

Friday morning, the US Bureau of Economic Analysis (BEA) announced US Q4 2015 GDP grew a meager 0.7% annualized, slowing from Q3's 2.0%. With this seemingly jiving with fears of a slowdown or worse, the deceleration stole headlines in short order. The Wall Street Journal dubbed it "anemic." The New York Times said , "The American economy barely grew last quarter, finishing the year much as it had started and stoking concern about its momentum in 2016." And many blame Energy, suggesting oil's drop is hamstringing the US economy. While the report is indeed a slowdown, we'd suggest that the details allude to an economy that was on fine footing at 2015's close-and that Energy isn't likely to derail growth looking forward.

First, to be clear, this report isn't stellar. But it also isn't a surprise. Wall Street analysts' forecasts ranged from 0.0% to 2.3%, with the consensus being +0.9%. So this isn't shocking anyone. And before you figure this raises doubts about the US economy's "momentum," consider that laws of physics do not really apply in econometrics. The simple fact of the matter is this is a backward-looking reflection of one slightly wonky, incomplete attempt to tally US economic performance. It is also one quarter-annual 2015 GDP data, also published Friday, showed GDP grew 2.4%, matching 2014's rate.

Exhibit 1: US GDP Growth, Quarterly and Annual Rates

Source: US Bureau of Economic Analysis, as of 1/29/2016.

Under the hood, there aren't hugely troubling trends. Consumer spending (technically called personal consumption expenditures) grew 2.2% annualized, adding 1.46 percentage points to headline growth.[i] Residential real estate grew 8.1%, adding 0.27 percentage point.[ii] Government consumption also modestly rose, adding 0.12 percentage point to growth.[iii] Business investment, however, fell, detracting -0.41 from growth.[iv] Exports fell -2.5% in the quarter, while imports rose 1.1%.[v] Combined, this means net trade detracted about half a percentage point. The export decline isn't great, but imports' rise shows domestic demand is fine.

This business investment detraction seems to be the source of the negative headlines, with many presuming there is worse ahead. And, a look at the data show two components heavily influenced the dip: transportation equipment and energy. The latter may grab your eye, considering theories regarding weak Energy sector investment quashing growth abound. The thing about this is, it isn't new. And it didn't gain steam in Q4, it fell at the slowest pace in 2015. In the year's four quarters, Energy investment fell -44.5%, -68.0%, -47.0% and -38.7%, respectively (all figures annualized rates).[vi] The table below highlights this point, showing the individual components of Private Nonresidential Fixed Investment. The red text shows the two big detractors: Energy (mining, shafts and wells) and Transportation equipment.

Exhibit 2: Contributions to Real Private Nonresidential Fixed Investment, Q1 - Q4 2015

Source: US Bureau of Economic Analysis, as of 1/29/2016.

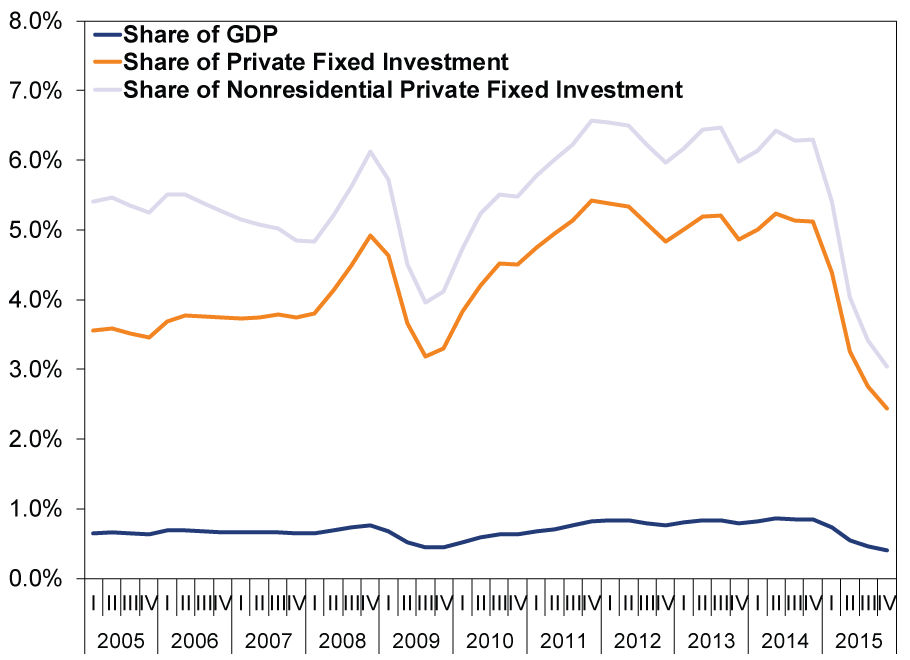

While Energy has powerfully influenced business investment over the past year, it's worth putting this in broader context. Exhibit 3 does that, showing Energy's share of US GDP, private fixed investment (business investment plus residential real estate) and business investment. As you can see, Energy's direct impact on GDP peaked at 0.87% of GDP.[vii]

Exhibit 3: Energy's Direct Impact on GDP in Perspective

Source: US Bureau of Economic Analysis, as of 1/29/2016.

Energy's contribution to GDP, private investment and business investment has already materially declined, and we didn't get an economic contraction. If it couldn't do so when it fell dramatically from a higher contribution to the US economy, it seems to us fairly unlikely to drive recession ahead.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

-

Behavioral Finance Investing Lessons From the Indianapolis Motor Speedway2026-05-18

-

Expert Commentary 3 Things You Need to Know This Week | Global Inflation, Fed Minutes, US Sentiment2026-05-18

-

In The News Around the World in Tax Policy Talk2026-05-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today