Personal Wealth Management / Market Analysis

Economic Growth Seems Plenty Durable

Do recent US and UK economic data show weakening growth?

Should investors worry the developed world's economic stalwarts seem to be slowing? Headlines think so. US December durable goods orders fell -3.4% m/m, "stirring growth concerns." Q4 UK GDP grew 0.5% q/q, closing 2014 with "waning momentum." But in our view, neither of these reports supports the notion the US and the UK are weakening-their underappreciated strength should still help drive this bull market.

Yes, on the surface, this was a yucky durable goods report. Excluding volatile transportation orders, orders were down -0.8% m/m. "Core" capital goods orders-non-defense capital goods orders excluding aircraft-fell -0.6% m/m. And since core capital goods are considered a leading indicator of business investment, some experts downgraded their estimates for Q4 GDP.

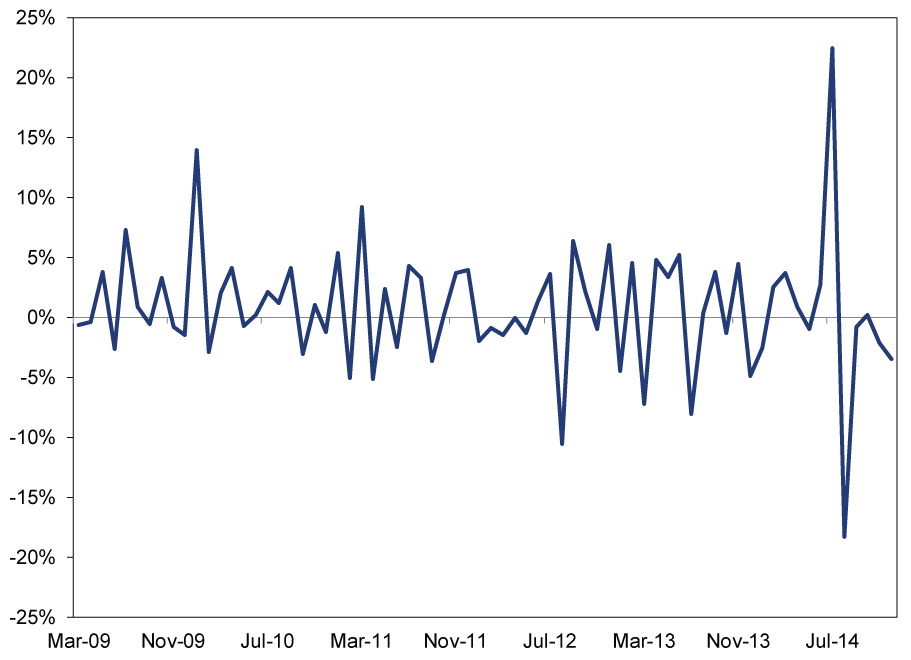

But context, as ever, is key. Durable goods data can be noisy, making it dangerous to infer much from one month's movement. This bull market and expansion have seen many durable goods drops, but growth overall continued and markets marched higher (Exhibit 1). Heck, even the present four-month slide in core capital goods orders isn't wonderful, but consider: Core capital goods orders fell in eight of nine months from December 2011 to September 2012-yet the US kept growing. This latest slide doesn't automatically indicate a worrisome long-term trend.

Exhibit 1: Durable Goods Orders, Month-Over-Month Change

Source: St. Louis Federal Reserve, as of 1/27/2015. Manufacturers' New Orders: Durable Goods, seasonally adjusted, 2/27/2009 - 12/31/2014.

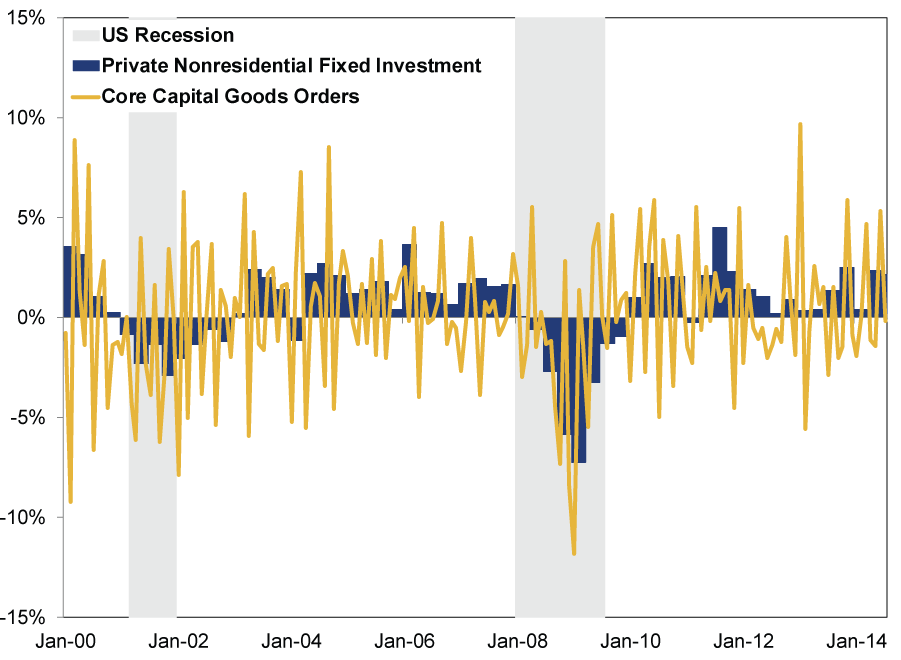

Nor does it automatically mean business investment dives. Capital goods-items like computer equipment or industrial machinery-are just one segment of business investment. The category also includes software, R&D and structures. This is a big reason why business investment usually doesn't reflect core capital goods orders' ups and downs. Moreover, business investment, though important, isn't a leading indicator for the broader economy. It isn't wholly indicative of growth's current or future prospects. (Exhibit 2) Consumer spending, real estate investment and trade matter, too.

Exhibit 2: Core Capital Goods Orders and Business Investment

Source: St. Louis Federal Reserve, as of 1/27/2015. Manufacturers' New Orders: Nondefense Capital Goods ex. Aircraft, January 2000 - June 2014; Real Private Nonresidential Fixed Investment, January 2000 - June 2014. Recessions as listed by NBER.

On to the UK, where some headlines glossed over GDP's 2.6% rise in 2014-its highest since 2007-and bemoaned Q4's 0.5% q/q growth, the year's slowest. Look a bit deeper, though, and there just isn't much evidence Britain is teetering. The slowdown came from construction (-1.8% q/q) and production (-0.1% q/q). Construction is notoriously volatile, not a make-or-break segment. Production's fall is tied largely declining North Sea oil and gas output, a long-running issue. Manufacturing output-more indicative of UK industry-rose 0.1% q/q. Construction and production comprise just 21% of GDP. Services, which comprise nearly 80% of GDP, rose 0.8% q/q.

Now, it is tough to draw huge conclusions from this preliminary estimate, since it doesn't include the spending breakdown or trade numbers. However, there isn't anything alarming about service-led growth in a service-based economy. Those claiming otherwise cite longtime fears of an "unbalanced recovery"-which stems more from failure to meet the government's arbitrary economic targets. Having heavy industry play a larger role is a political goal, not an economic necessity. A strong services sector is a normal byproduct of economic progress and just fine.

All this hubbub is a good reminder not to latch onto any single statistic as a sign all is well or ill in any economy. No one report-not even GDP-will tell you everything. Taking a big sample is key, and today's big sample indicates overall growth, countering the "weakening" US and UK meme. For the US, ISM's December services and manufacturing purchasing managers' indexes (PMIs) stayed well above 50 (the divider between growth and contraction)-55.5 for manufacturing and 56.2 for services-with forward-looking new orders hitting 57.3 and 58.9, respectively. The Leading Economic Index (LEI) rose 0.5% in December-its fourth consecutive monthly rise-implying growth continues. Retail sales rose 0.4% in Q4. In the UK, Markit's December PMIs for manufacturing (52.5), construction (57.6) and services (55.8) all point to expansion. December retail sales also rose 0.4% m/m (2.3% q/q in Q4), highlighting UK consumers' strength. Overall, data imply the US and UK are in fine shape economically.

In our view, headlines' reactions to these numbers say more about sentiment than reality in the developed world's strongest economies. Expectations are still pretty low, giving reality room to surprise-bullish for stocks.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today