Personal Wealth Management / Economics

Eight Charts That Deflate UK Inflation Fears

Rising prices in the UK don't portend future struggles.

UK CPI just hit a two-year high. Oh my![i] It seemed just like yesterday the fear du jour was British deflation, which prompted BoE governor Mark Carney to write a letter. Now folks fear rising prices will outstrip wages, eating into UK consumer spending-Brexit's long-awaited wrath. Folks can't seem to be happy either way. Yet Britain's rising prices aren't an isolated incident signaling Brexit's bite-inflation gauges globally are up, and not in a problematic way. The inflation bogeyman shouldn't kill the UK's expansion or this bull market.

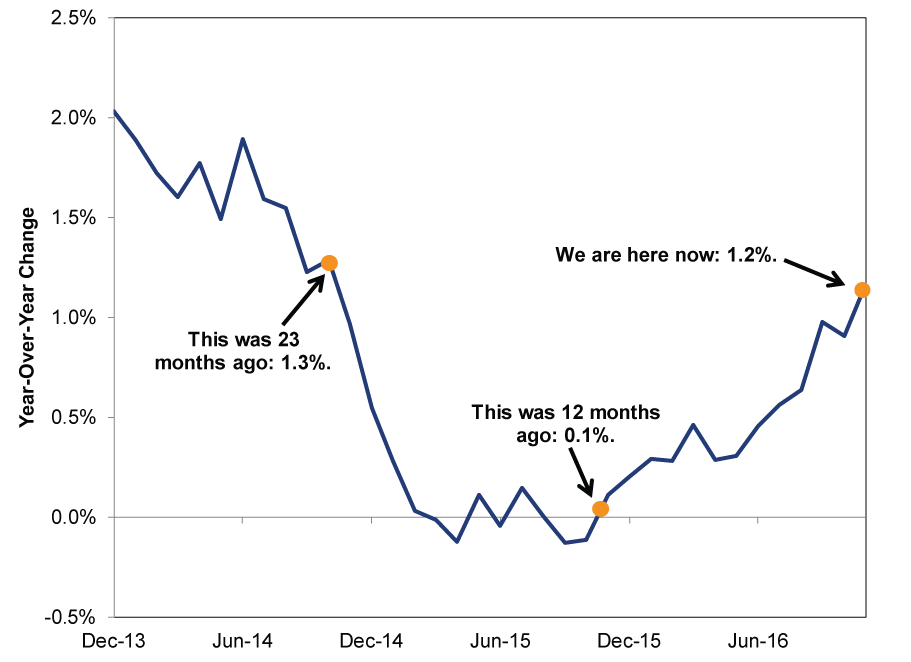

November UK CPI rose 1.2% y/y, up from October's 0.9% and the fastest annual pace since October 2014. This caps an eventful two year stretch for UK prices.

Exhibit 1: UK Prices' Wild Ride

Source: FactSet, as of 12/14/2016.

Though rising, CPI still trails the Bank of England's 2.0% annual inflation target. It is also far below levels seen in 2011. However, some BoE officials warn rising prices will hurt consumer spending, knocking the economy next year. The supposed cause? Brexit, which weakened the pound. Because a weaker currency makes imports more expensive, many fear this will drive up costs, which then get passed on to consumers. Scary! Yet rising import prices needn't whack consumer spending-these relationships are complex.

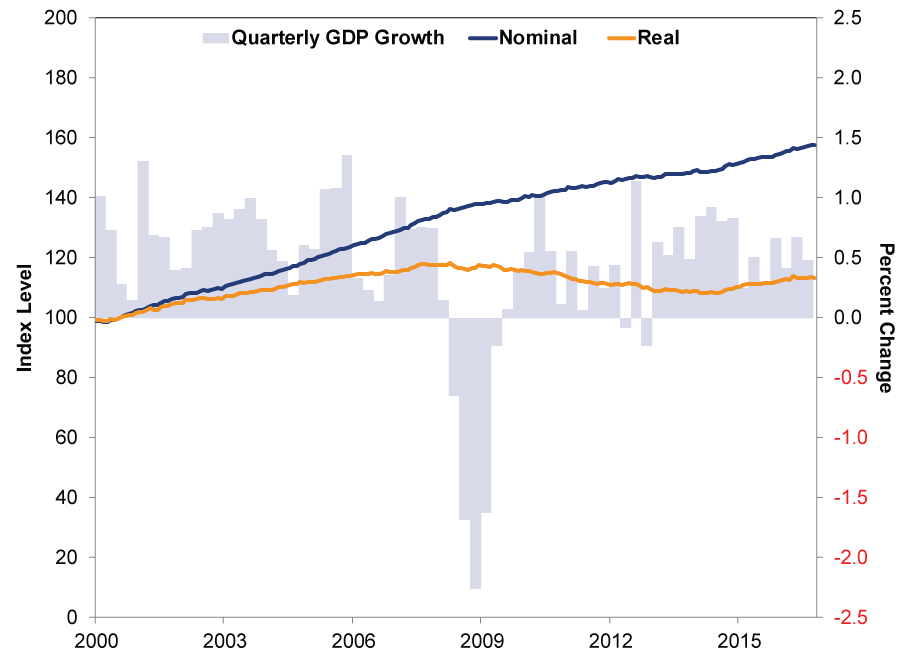

Even if prices do rise further and eventually knock real wages, this isn't necessarily a consumer death knell. Real wages fell from April 2008 to April 2014 and still remain -4.0% under that 2008 peak. BoE Governor Mark Carney recently said "real earnings have grown at the lowest rate[ii] since the mid-19th century." Yet this hasn't killed UK consumption or broader economic growth. (Exhibit 2) Even in 2011, when inflation neared 5% after a VAT hike, UK GDP grew 1.5% despite household spending's -0.7% drop. Today's conditions are better than that and don't look likely to radically shift soon, so we fail to see the big economic headwind looming next year.

Exhibit 2: Falling Real Wages Haven't Derailed This Expansion

Source: The Office for National Statistics, as of 12/15/2016.

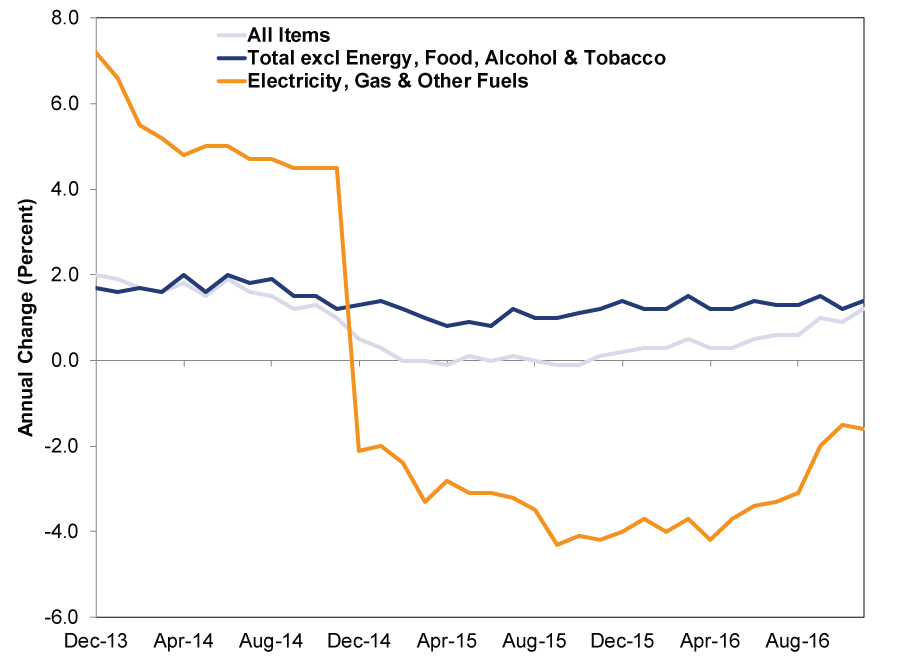

A deeper dive into CPI numbers debunks more inflation concerns. Rather than a big Brexit-induced negative, accelerating inflation reflects a volatile subcomponent: Energy prices. After suffering some big drops over the past two years, oil prices stabilized in 2016, skewing CPI downward. Moreover, Energy is about to turn positive on a year-over-year basis as early 2016's rock-bottom prices become the comparison point. A look at core CPI, which excludes volatile energy and food categories, shows most prices stayed pretty steady during the big "deflationary" stretch. And they remain steady today.

Exhibit 3: Energy's Drag on UK CPI

Source: FactSet, as of 12/14/2016.

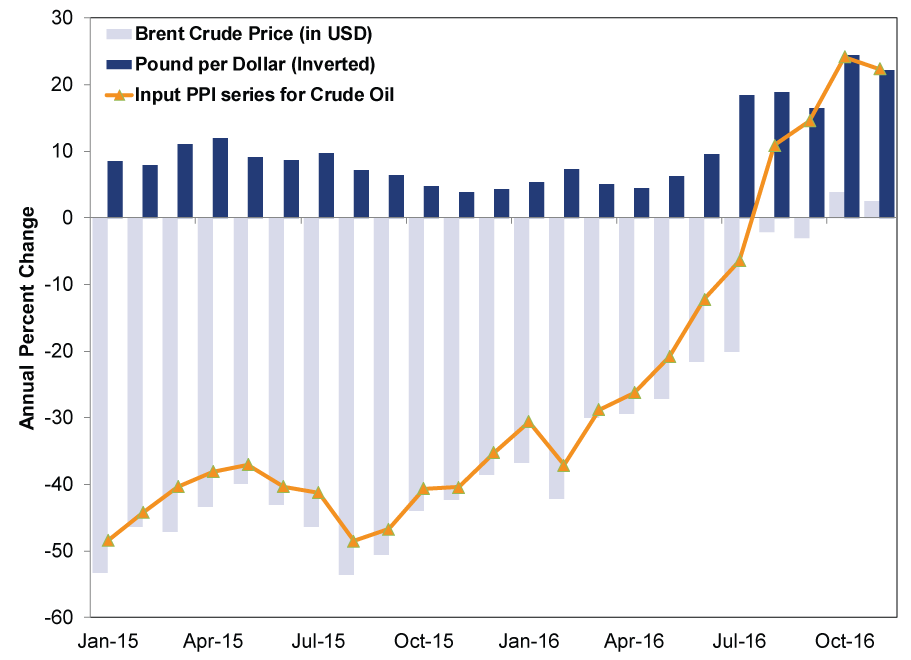

We aren't saying the weaker pound has no effect, as import prices have been rising. In November, materials and fuels bought by UK manufacturers were up 12.9% YTD while core input prices (excluding food and energy costs) grew from October's 10.3% to 11.5% YTD. As the ONS noted, the pound's relative weakness to the US dollar is exacerbating higher oil import costs.

Exhibit 4: A Weaker Pound Makes for Higher Energy Costs

Source: Financial Times, Bank of England, Office for National Statistics, as of 12/14/2016. Dark blue bars above X-axis represent depreciation of pound relative to dollar over past 12 months. Input Producer Price Index (PPI) measures imported and domestically sourced crude oil, which may be affected by other factors besides the exchange rate.

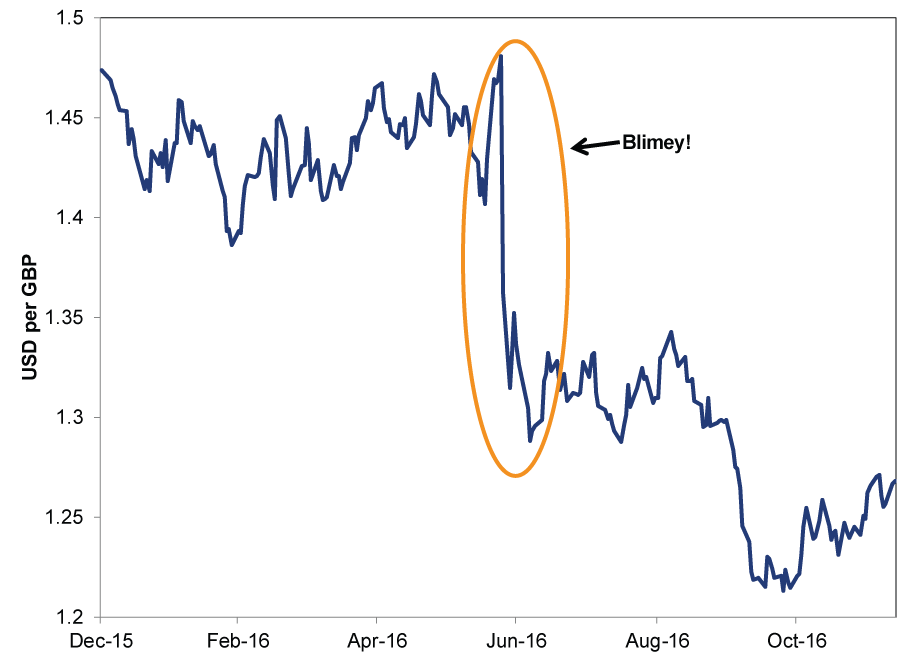

However, much of the pound's weakness happened in the Brexit referendum's immediate aftermath. This sets up another one-off scenario-similar to oil prices' big drop-that skews the data. Unless there is a renewed pound plunge, the higher inflation rates caused by the weaker Sterling will fall out of these data next autumn.

Exhibit 5: Sterling's Summertime Swoon

Source: FactSet, as of 12/14/2016.

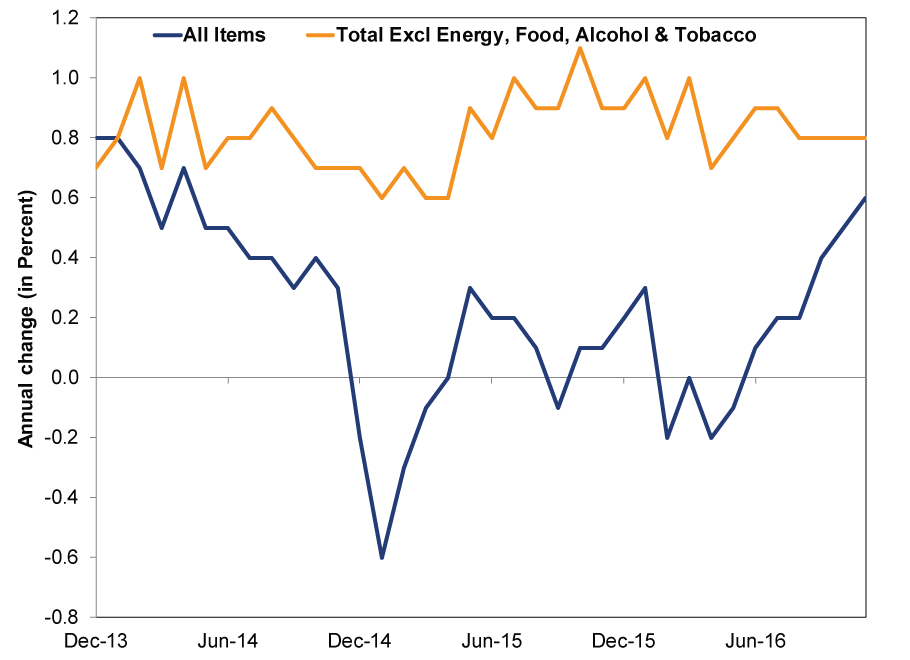

Looking more broadly, prices aren't just rising in Britain and thus a Brexit-induced phenomenon. CPI is picking up across the developed world now that Energy isn't a drag.

Exhibit 6: Eurozone CPI (All Items vs. Core)

Source: FactSet, as of 12/14/2016. From 12/31/2013 - 11/30/2016.

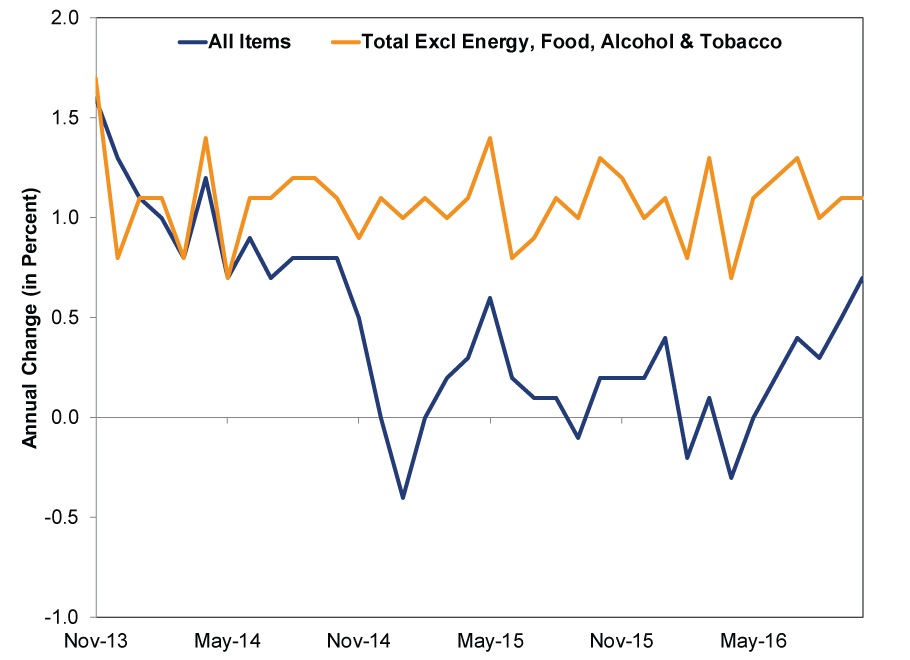

Exhibit 7: Germany CPI (All Items vs. Core)

Source: FactSet, as of 12/14/2016. From 11/30/2013 - 10/31/2016.

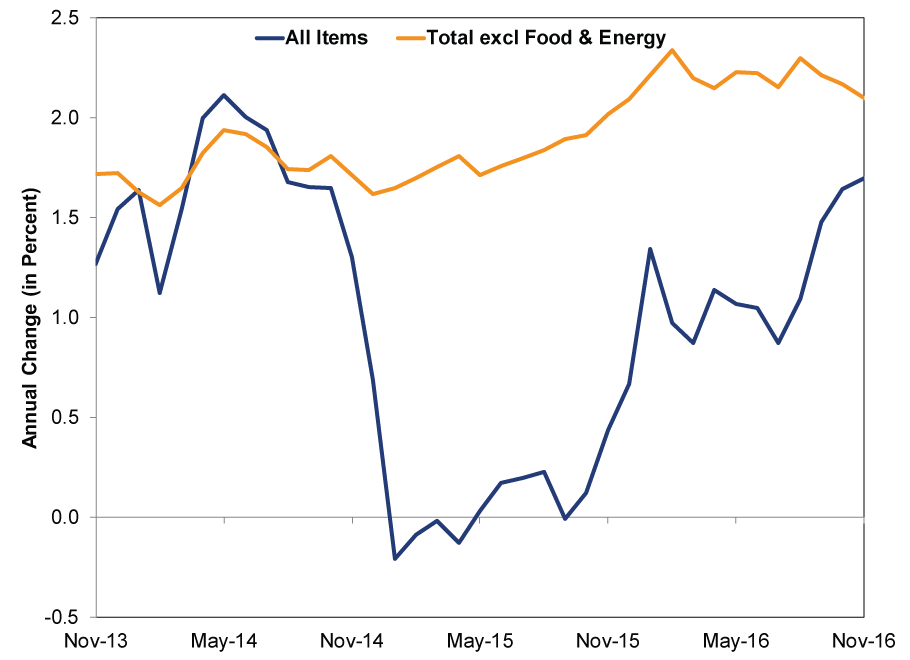

Exhibit 8: US CPI (All Items vs. Core)

Source: FactSet, as of 12/15/2016. From 11/29/2013 - 11/30/2016.

We would also add US CPI has accelerated while the dollar has strengthened. If currency were truly an outsized price driver, import prices should have plunged, taking CPI with them. Yet this hasn't happened-compelling evidence currency swings alone don't singlehandedly move prices.

These inflation concerns are yet another iteration of Brexit-related fears. Folks keep fretting the potential economic negatives, despite plenty of evidence to the contrary-most important one being, we don't know what Brexit's actual terms are yet. These worries shroud Britain's growth prospects, which look solid for the foreseeable future thanks to a steeper yield curve and healthy private sector.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today