Personal Wealth Management / Economics

Eight Straight and Counting: The Eurozone’s Underappreciated Growth Streak

The eurozone grew for the eighth straight quarter in Q1, but most pundits are only now noticing.

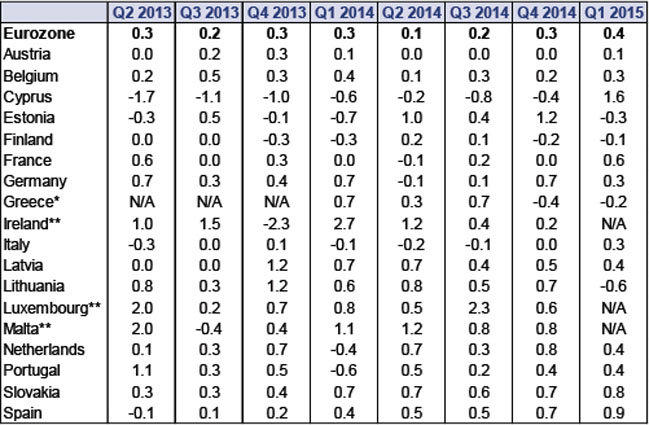

It's now eight straight, folks. That's right-the eurozone has grown for eight straight quarters following this week's report, which clocked Q1 growth at +0.4% q/q. Headlines lauded the acceleration from Q4's +0.3%-but they were quick to add caveats, like Finland's contraction and Greece's return to recession , high government debt levels, still-elevated unemployment or Germany's slower growth rate. For investors, the data themselves don't mean a whole lot-stocks are forward-looking and GDP looks backwards. But reactions to the report say a lot about sentiment-a key market driver-towards the region today.

Overall, the report was pretty positive. Twelve of the 16 reporting nations grew, and troubled Cyprus came in first at 1.6%-its first quarter of growth since 2011[i]. Spain led the major economies at 0.9%, continuing its solid run. France resumed growing and came in second among the core four at 0.6%. Italy grew (0.3%) for the first time since Q4 2013. Only Germany disappointed, slowing to 0.3%.

Exhibit 1: Eurozone GDP Growth (Q/Q, Seasonally Adjusted)

Source: Eurostat and FactSet, as of 5/15/2015. *Greece didn't resume reporting quarter-over-quarter seasonally adjusted growth until Q1 2014. They had some troubles with numbers before that. **These countries have not yet reported Q1 GDP.

All in all, growth was solid and broad-based, continuing the trend from recent quarters-a trend that seems utterly lost on the media, which continues to ignore the fact the currency bloc has grown eight straight quarters. They continue to see growth as new and probably temporary. Most couched Q1's pop as an unsustainable acceleration based on factors like lower oil prices and the early fruits of quantitative easing (QE). Soon, they warn, larger headwinds like Greece, high unemployment, high debt and a lack of structural reform will reassert themselves, and economic malaise will return.

This is all easy to pick apart. Let's start with QE. While full-fledged QE began in March, markets started pricing it in last year, when the ECB started jawboning. Long-term yields fell as investors anticipated bond-buying, and pundits argue this goosed lending and growth. But loan growth started showing signs of life before QE was a twinkle in Mario Draghi's eye. Ditto for money supply, which has accelerated for over a year. All, incidentally, while yield curves were steeper. Yield curves have flattened since then, thanks largely to bond buying. This is anti-stimulus. When yield curves are flatter, so are banks' profit margins. They borrow short and lend long, the spread is their profit margin, and slim profits discourage lending. Banks won't take risk without compensation. Loan growth picked up despite QE, not because of it.

As for the others, a question: If Greece, unemployment, debt and structural inefficiencies haven't derailed the recovery two years in, why would they have any more power now? Greece is too small for its recession relapse to tip the scales, just as its lingering depression in 2013 didn't thwart the eurozone's nascent recovery. Unemployment was higher when the recovery started than it is today and has always been a lagging indicator. Unemployment doesn't prevent growth-growth improves unemployment. Debt isn't an economic driver, and most of the troubled countries have made significant deficit reduction strides. Some have made so many strides that they've been able to loosen austerity with tax cuts, like Spain did earlier this year. Now, we won't argue structural reform wouldn't help, particularly in France (where investment continues falling) and Italy. But cyclical factors can outweigh structural issues. Cyclical factors are clearly in France's favor, and now Italy is perhaps turning the corner too. Moreover, growth is broad enough to help pull these nations along.

While sentiment is stuck in the past, dwelling on long-running perceived negatives, forward-looking indicators look promising. Service and manufacturing new orders are broadly in expansion across the continent. The Conference Board's Leading Economic Index for the eurozone rose 0.7% in March, its sixth rise in seven months. French and German LEIs each rose five of seven months through February. Spain's is up six months straight. All are consistent with a continued, broadening growth cycle.

Eurozone growth may not be the world's fastest, but stocks don't need swift growth to do fine. Just reality that beats expectations, which Europe has in spades today.

[i] If you are drawing up a national economy someday, we suggest a different plan than "be a Russian billionaire's tropical piggy bank and Greece's economic satellite." That one has not worked well recently for Cyprus.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Upcoming IPOs, US Jobs Data, Credit Card Delinquencies

2026-06-05

2026-06-05 -

Market Volatility Seek Perspective Instead2026-06-05

-

Market Analysis No Flowers for the May Jobs Report?2026-06-05

-

Expert Commentary The US Midterm Campaign Trends Ken Fisher Is Watching

2026-06-04

2026-06-04

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today