Personal Wealth Management / Economics

Employing Patience

A shrinking workforce took the shine off August’s falling unemployment rate, but history shows the economy can grow and employment improve as labor force participation falls.

The BLS released August’s Employment Situation report Friday, and it was a decidedly mixed bag. Headline unemployment fell from 8.3% to 8.1%, and the US added 96,000 jobs—not too shabby, at first blush. But analysts broadly expected 130,000 new jobs, and the falling headline rate’s primary driver was a 368,000 drop in the workforce.

Like the unemployment rate, the workforce tally is subject to volatility. In any given month, it’s likely folks retire, go back to school, or decide to stay home with their families or to care for an aging relative. Perhaps some elect to take an extended break to travel. Yes, as many outlets were quick to point out, some do get discouraged and quit seeking work, but it’s far from certain 368,000 people made that decision in August. And of those who did, it’s entirely possible some change their mind soon—monthly data are fickle.

Hence, as ever, we’d suggest looking longer term: Today’s labor force is still 971,000 higher than one year ago. Unemployment, meanwhile, is fully one percentage point lower than in August 2011, and over 2.3 million more people are employed. Broad labor market improvement, it seems, continues.

Improvement, however was not the story in many mainstream reports on Friday’s release. Instead, many focused on the 63.5% labor force participation rate—the lowest since 1981, when women began entering the workforce in earnest. On the surface, a lower percentage of Americans working or looking for work may seem a not-so-great development. And certainly it’s not great for those who truly have given up their job search. Yet, when measuring the economic impact, it’s important to take a higher-level view—specifically, what’s happened to total US output as the participation rate has arced?

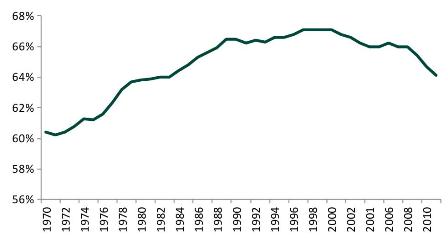

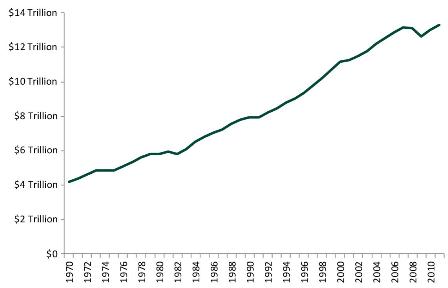

Exhibits 1 and 2 plot the US’s labor force participation rate and real annual GDP from 1970 through 2011.

Exhibit 1: US Labor Force Participation Rate

Sources: St. Louis Federal Reserve, US Department of Labor.

Exhibit 2: US Real GDP

Sources: United Nations Statistics Division, US Bureau of Economic Analysis.

Since the participation rate peaked in the mid-1990s, we’ve added trillions of dollars of annual GDP. Real output is at an all-time high and growing. A lower labor force participation rate doesn’t appear to have materially impacted our economy.

Nor does it mean the labor market has weakened over time. Exhibit 3 shows total US employment over the same period. As we’d expect, employment has followed the same general pattern as economic growth.

Exhibit 3: Civilian Employment of All Persons in United States

Sources: St. Louis Federal Reserve, Organisation for Economic Cooperation and Development.

However, employment has regularly tracked the economy at a delay. And the current delay, it seems, lies at the heart of today’s broad frustration with the US labor market. Improvement is happening, just not fast enough (whatever “fast enough” means). The fact employment has historically lagged the broader economy by a few months or years—and that employment regularly remains in recovery long after the economy resumes expanding—is likely cold comfort to those directly impacted. As is the fact slow employment improvement should be expected to follow the US’s recent slower economic growth. In fact, job gains may remain slow a while longer. But we see nothing suggesting economic forces have so radically changed that employment no longer lags the economy.

Importantly for equity investors, slow employment gains and lower labor force participation typically don’t have much bearing on future stock returns. Markets are discounters—and since unemployment is a late-lagging indicator, the economic factors contributing to Friday’s report have likely long been reflected in stock prices. Looking ahead, with corporations healthy and fundamentals overall better than widely appreciated, the stage seems set for future gains, growth and—eventually—jobs.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Rate Decision, US-Iran, Inflation in Europe

2026-06-19

2026-06-19 -

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today