Personal Wealth Management /

Europe’s Improving Health

Those focusing on weak French data are ignoring the bigger, more important eurozone picture.

“France is a drag on the eurozone.” “France’s debt load in ‘danger zone.’” You can’t venture too far into financial news without reading how France’s weak economy will spiral out of control (a big stretch) and choke the eurozone recovery. But in our view, focusing on possible weakness in one country misses the forest for the trees. Simply, the eurozone today is light years away from where most expected a year, two or three ago. The periphery is climbing back, yields are at pre-euro crisis levels and the economy is growing again—and looks likely to keep it up.

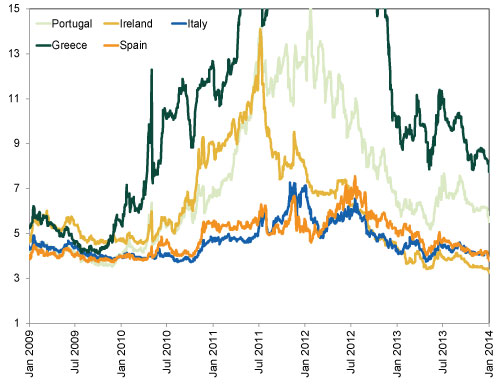

Take peripheral sovereign debt yields, shown in Exhibit 1. Yields spiked in 2011 and 2012 as fears of a disorderly collapse reached their apex. Many feared high borrowing costs would price Italy and Spain out of capital markets—forcing them to request full sovereign bailouts—and make it difficult for Ireland and Portugal to come back from their own bailouts. (And Greece was Greece). But now yields are close to—and in some cases, below—pre-crisis levels. The eurozone is still here, and investors have much more confidence in the periphery’s ability to honor its debts (except, perhaps, Greece).

Exhibit 1: Peripheral Eurozone Sovereign 10-Year Bond Yields

Source: FactSet Data Systems, Inc., as of 1/8/2013.

And in Ireland, they’re lining up to buy more of it! Ireland officially exited its bailout program in December, and its first post-bailout debt auction occurred Tuesday. Demand was through the roof. Bids passed €14 billion for a €3.75 billion lot of 10-year bonds, and the average yield was just over 3.5%. The success drove benchmark 10-year rates to 3.27% in the secondary market in the wake of the auction—down from over 14% in 2011 and at an 8-year low. GDP is also growing, having risen 0.4% q/q in Q2 and a hot 1.5% q/q in Q3 (that’s 6.1% annualized).

Portugal is also faring well. It, too, is growing—up 1.1% q/q in Q2 and 0.2% in Q3, led by business investment. Parliament is still battling courts over austerity measures (many are illegal under the socialist constitution), but the country has met bailout targets, held successful debt auctions and appears on track to exit its bailout later this year as scheduled. Italy is also improving some. It’s still in recession, but political uncertainty has lifted some as a splinter group from former Prime Minister Silvio Berlusconi’s party threw its support behind Prime Minister Enrico Letta, making his government more workable. The Supreme Court’s decision to chuck the byzantine electoral code added additional stability. Spain exited its recession in Q3 2013, with +0.1% q/q GDP growth. It exited its bank bailout program, too, and private demand for troubled banks is robust. Borrowing costs at Thursday’s auction reached their lowest levels since Spain joined the euro, and demand exceeded the target. Greece is still Greece—the government forecasts growth and a primary budget surplus for 2014, but they’ve also alluded to a potential third debt default. Though, judging from yields, investors don’t seem terribly shocked. What matters more than defaults is that Greece is still in the euro—and likely stays there with politicians still committed to supporting the currency.

In short, the eurozone periphery has defied expectations. And the broader eurozone is doing the same on the economic front. Eurozone retail sales increased 1.4% m/m in November—the largest monthly increase since 2001 and well above expectations for 0.1%. Sales were up across much of the region. Germany logged a solid 1.5%. Portugal rose a robust 3.1%, and Spain rose 1.9%. But perhaps the biggest surprise came from Europe’s alleged new “sick man.” French retail sales grew 2.1%, a counterpoint to those who claim contracting PMIs mean automatic recession.

Not that France will carry the region along—Germany, the biggest economy, likely does most of the pulling, and a recent manufacturing report suggests it’s chugging right along. November German factory orders beat expectations, rising a seasonally adjusted 2.1% m/m and 6.8% y/y. Domestic orders rose 1.9% m/m, and orders from outside the eurozone rose 3.5% m/m—a sign demand abroad is also healthy. Orders from the other 17 eurozone nations were flat—not wonderful, but not evidence of cratering demand.

But factory orders are just one indicator of demand growth—they show a small subset of future business investment. The Leading Economic Index (LEI) paints a more complete picture and has been a fairly reliable predictor of recent eurozone trends. It’s up six months straight. Germany, Spain and yes, even France all show rising LEI trends.

Not that the eurozone starts firing on all cylinders from here. Its recovery likely remains slow and uneven—especially as banks continue deleveraging. But what matters more for stocks is the gap between reality and expectations. France and the other eurozone countries needn’t do amazingly for markets to do well, they just need to do better than most people expect. With most seemingly expecting a double dip recession and deflationary spiral, slow and uneven growth should be a good enough surprise.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today