Personal Wealth Management / Market Analysis

Exports Couldn't Rescue Japanese Growth in Q1

The latest GDP figures highlight Japan’s reliance on external demand.

As the sports world waits to see whether LeBron James’ consecutive NBA finals streak will hit eight years, another streak snapped this week: A preliminary estimate showed Q1 Japanese GDP fell -0.6% annualized, missing expectations for a milder -0.2% contraction and ending Japan’s run of consecutive positive quarters at eight (its longest in nearly three decades). The previous two quarters were also revised down, including Q4’s sharp downgrade from 1.6% annualized growth to 0.6%. While the poor showing doesn’t necessarily presage further weakness, it highlights Japan’s reliance on trade to make up for tepid domestic demand. This quarter, it couldn’t—evidence Japan’s largest exporters probably provide global investors more opportunities than domestically focused firms.

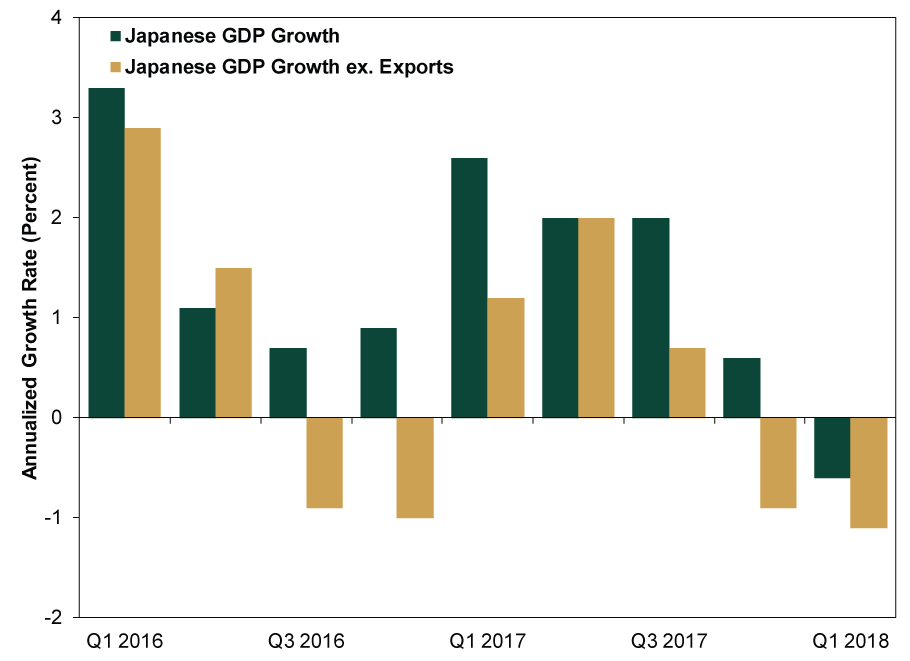

Trade was a lonely bright spot in Q1, but it still dimmed. Exports rose 2.6% annualized, a sharp deceleration from Q4’s 9.2% pace and Q3’s 8.2%. Imports—one marker of domestic demand—also slowed dramatically, rising just 1.2% annualized after notching 12.9% growth in Q4. Household spending and private nonresidential investment dipped, while overall domestic demand shrunk -0.9% annualized, its worst showing since Q4 2015. While these figures are subject to revision (either higher or lower), they indicate Japanese growth still mostly hinges on external demand. If exports falter—or domestic consumption has an especially bad quarter—headline growth probably struggles.

Exhibit 1: Ex. Exports, Japanese Growth Struggles

Source: Japan Cabinet Office, as of 5/16/2018. Japanese quarter-over-quarter annualized GDP growth with and without exports’ contribution, Q1 2016 – Q1 2018.

Now, we aren’t saying Japan is about to drag down the global economy or markets. Rather, a growing world probably pulls Japan along, as it has for a couple years. Although global growth largely underwhelmed in Q1, forward-looking indicators like yield curves, money supply and firms’ new orders suggest the expansion will continue. Thus, we wouldn’t be surprised to see Japanese exports—and GDP—rebound. Moreover, temporary factors like high vegetable prices and a fall in smartphone sales may have held down Q1 GDP, according to the Japanese Economy Minister. Record snowfall in Japan in January and February likely also played a role by keeping consumers at home and disrupting shipments.

But temporary forces can’t explain everything. Structural issues—like rigid labor markets, trade barriers and counterproductive quantitative easing policies—have weighed on the Japanese economy for years. The BoJ seems to be subtly tapering quantitative easing (QE), but slowly—and Prime Minister Shinzo Abe’s reform efforts have largely fallen flat. BoJ chief Haruhiko Kuroda recently called on the government to “take on structural reform and growth strategy,” but with Abe battling cronyism charges and September party leadership elections approaching, we aren’t holding our breath. That said, stocks move most on the gap between reality and expectations, and sentiment toward Japan seems to fathom the country’s many domestic headwinds. So rather than Japan’s issues being a reason to avoid Japanese stocks, we think deepening pessimism could eventually raise the likelihood of even so-so results beating expectations.

Therefore, while we wouldn’t encourage investors to go hog-wild for Japanese stocks, we think there are some favorable opportunities there, particularly among big exporting firms that can harness strong global trade trends. Those connected to global electronics supply chains, where Japan is carving out a niche, may also stand to benefit from the ongoing Tech-related boom. But without a marked shift in Japan’s domestic fundamentals, firms relying on Japanese consumer demand probably face tougher sledding for the foreseeable future.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News In Orbit? On Tech Sentiment and IPOs2026-05-22

-

Market Analysis Global Bond Calamity Calls for Calm Perspective2026-05-22

-

Expert Commentary This Week in Review | UK Politics, Fed Developments, IPOs

2026-05-22

2026-05-22 -

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today