Personal Wealth Management / Market Analysis

Fear and Loathing and European Politics

Investors needn't fear recent political developments on the Continent.

Political uncertainty is stoking fear across much of the developed world. In the US, pundits pontificate about the potential negative market impact from either a Donald Trump or Hillary Clinton presidency. Similarly, recent and upcoming votes in the eurozone's four biggest economies-Spain, Italy, France and Germany-have contributed to an environment of fear and loathing across the Continent, causing many to miss the region's overall fine economic results. Time and again, forecasted political "disasters" have had a limited impact on the fundamental environment in Europe. The Brexit vote increasingly appears to have had little economic impact, with the most recent data pointing to the 14th consecutive quarter of expansion in Q3. Even long-beleaguered European Financials stocks are doing better, as issues like negative interest rates and regulatory changes have failed to live up to fears. While the upcoming votes might bring minor political shifts, all appear unlikely to result in big, sweeping change. Instead, they likely push governments deeper into gridlock-an underappreciated positive-which reduces uncertainty and legislative risk.

Spain

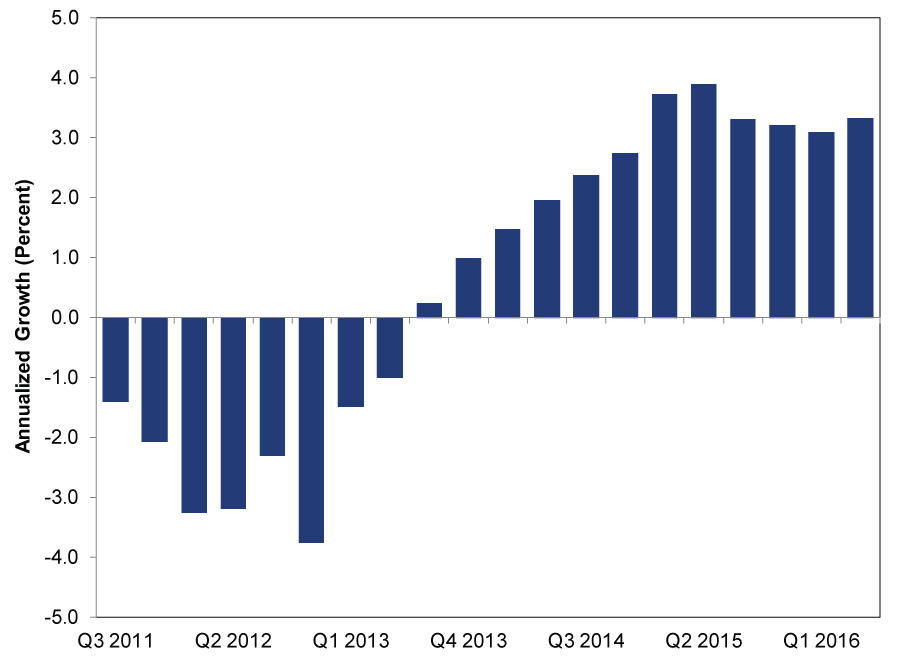

Spain is likely headed to its third general election in a year after its fragmented parliament failed to form a government following June's election. Prime Minister Mariano Rajoy of the center-right Popular Party (PP) was unable to win a confidence vote to form a minority government with upstart, centrist Ciudadanos. If neither Rajoy nor the opposition Socialist Party is able to form a government by Halloween, Spanish voters will return to the voting booth-potentially on Christmas Day.

While many feared the lack of a government would damage the economy, data show little evidence it has. Thanks to reforms passed in recent years, Spain has been one of the fastest-growing developed economies, with GDP expanding 3.2% annualized in 2016's first half.[i] Political gridlock likely prevents meaningful changes to those reforms, allowing Spain's increasingly competitive private sector to drive growth.

Exhibit 1: Spanish Growth Is Chugging Along

Source: FactSet, as of 9/9/2016. Seasonally adjusted annualized GDP growth on a quarterly basis, Q3 2011 - Q2 2016.

Italy

Italy appears set to hold a constitutional referendum in November, widely seen as a vote of confidence in Prime Minister Matteo Renzi's government. Renzi is seeking to facilitate lawmaking and make governing coalitions more stable-addressing a problem for Italy, which has needed political reform for decades. After Renzi announced the referendum in July, initial polling showed more voters were against the PM's proposals than for them. The fear here is that if the referendum fails, the government will collapse, fresh elections could follow, and the anti-establishment Five Star Movement might fill the vacuum-introducing even more uncertainty.

However, besides polling's spotty recent history, political instability in Italy is nothing new. Markets are very familiar with the country's constant political turnover, with five governments over the last 10 years. While reforms would be a long-term positive, a failure to pass or a significant watering down wouldn't surprise markets, sapping away negative shock power. Further, Italy makes up less than 1% of global stock markets[ii] and just about 2% of global GDP[iii]-not nearly large enough to wallop global growth or the current bull market.

France and Germany

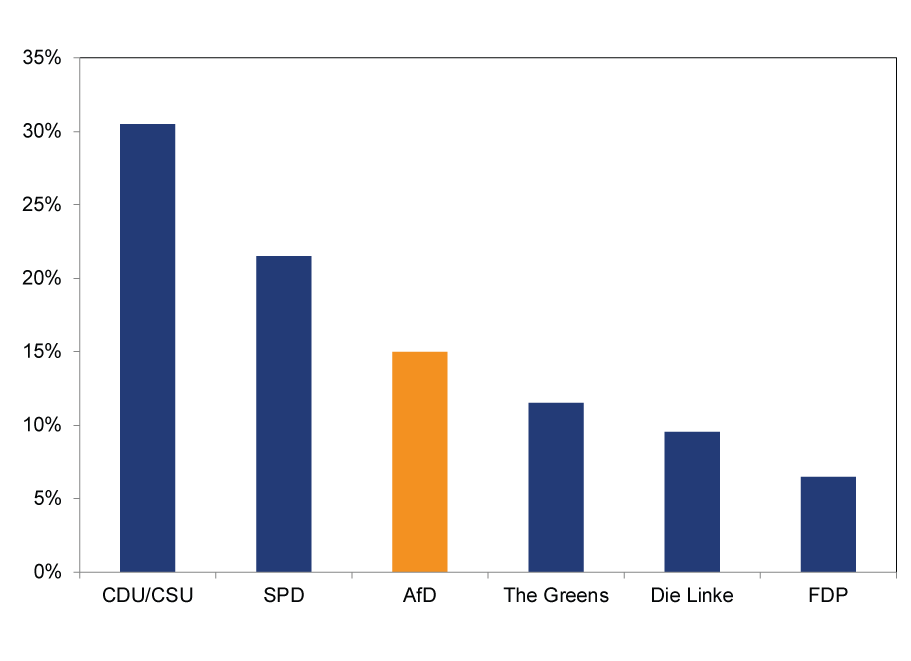

France and Germany will hold general elections in 2017-France in the spring, Germany in the fall-and in both, there is anxiety over the rise of far-right parties and the potential instability they represent. France's Front National and Germany's Alternative für Deutschland (AfD) have had relatively strong showings in recent polls, but both are still far from winning the presidency or forming a government.

In France, polls indicate the Front National's presidential candidate Marine Le Pen will do well in the first round of an election-winning approximately 27% of the vote-but she is expected to lose to nearly every other candidate (other than incumbent FranÇois Hollande, who is unlikely to get his party's nomination) by a double-digit margin in the next round. This echoes the Front National's past performance in regional elections. After a strong first round in December elections, the mainstream Socialist and Republican parties coordinated efforts to defeat Front National candidates in round two, denying them even a single regional victory.

In Germany, the AfD had a strong showing in the Mecklenburg-Vorpommern regional election, but ultimately, they won only about 20% of the vote, good for second place. Nationally, they are polling around 15%. While good for a relatively new party, they are still just third nationwide. Moreover, the AfD would struggle finding coalition partners to form a government. Their rise likely foreshadows more gridlock, rather than a shift in political policy.

Exhibit 2: The AfD Trails the Traditional German Parties

Source: INSA; as of 9/5/2016

Plus, mainstream politicians have already started toughening their language to curry favor with populist voters ahead of the election. Consider the Transatlantic Trade and Investment Partnership (TTIP) with the United States: German Vice Chancellor Sigmar Gabriel, potentially the Social Democratic Party's candidate for chancellor, called the deal "de facto failed" while France's Hollande withdrew his support for any agreement through the year's end-signs of their willingness to stall free trade talks to placate their constituents.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Interesting Market History Six Years On, Lessons From the COVID-Lockdown Low Endure2026-03-25

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today