Personal Wealth Management / Market Analysis

Fisher Investments on China’s Three Pillars

China is likely poised to avoid a hard landing and continue growing, but that doesn’t mean Chinese stocks are set to soar.

In a recent article, we discussed why it’s a good thing in Fisher Investments’ view China’s not letting its currency appreciate right now given its ongoing deceleration in loan growth. However, though Fisher Investments believes this means China and the global economy shouldn’t be headed for a massive slowdown, it doesn’t mean China is a terribly attractive place to invest right now.

In fact, it could mean the opposite—at least for the rest of 2011. (In 2012, a new compelling driver appears—which we’ll cover in a later column.) Loan growth, currency movement and equity supplies are the three pillars of China. If you understand the direction of these three factors, historically, you’ve had a very good shot at predicting the direction of China’s relative performance.

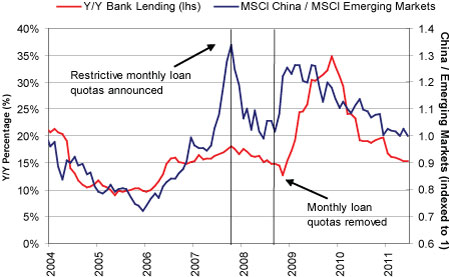

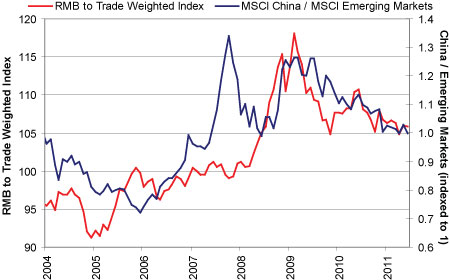

Exhibits 1 and 2 show how China’s stock market historically outperforms when loan growth is accelerating along with its currency and underperforms when the reverse is taking place. Recall that without a significant bond market, loan growth is used to accelerate the economy. Unfortunately it also creates inflation, which the rising currency helps partially mitigate. From an investor’s standpoint, such a scenario provides rising economic growth and a tailwind from currency appreciation—no wonder China’s market tends to do well during such periods.

Exhibit 1: China’s Loan Growth vs Relative Performance

Source: Thomson Reuters. MSCI China / MSCI Emerging Markets, 12/31/03-6/30/11.

Exhibit 2: China’s Trade Weighted Currency (RMB) vs Relative Performance

Source: Thomson Reuters. MSCI China / MSCI Emerging Markets, 12/31/03-6/30/11.

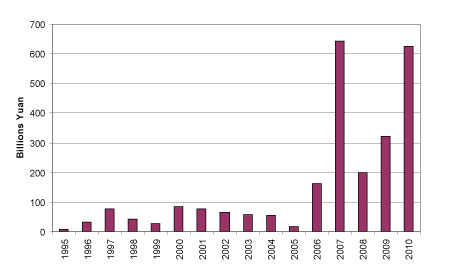

Of course that’s not the entire equation. We just covered the demand side, but just as important is the supply side—the third pillar. When equity supplies have increased dramatically or threatened to do so—like pre-2006 when uncertainty reigned over how the government would unlock the roughly 70% of non-floated shares—China’s shares have typically suffered. By comparison, during periods like the first half of 2009 when IPOs were banned and share supply creation curtailed, shares appeared to receive an extra tailwind. The timing of the IPO ban and its correlation with changes in China’s relative performance can be seen in Exhibit 3, while Exhibit 4 shows recent equity issuances.

Exhibit 3: China’s Relative Performance and the IPO ban

Sources: Thomson Reuters and Bloomberg Finance LP. MSCI China / MSCI Emerging Markets, 12/31/03-6/30/11.

Exhibit 4: China’s Equity Issuance

Source: Bloomberg Finance LP.

China’s current policy of decelerating loan growth and letting its currency depreciate on a trade-weighted basis should prevent a hard landing while reining in inflation, but it doesn’t create a positive backdrop for investors. Add on high equity issuances and the potential for more with rumors of another bank recapitalization program this year, and China appears likely to remain an engine of global economic growth (as illustrated by initially estimated Q2 2011 GDP of +9.5% y/y)—but an unattractive investment for the balance of 2011.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today