Personal Wealth Management / Market Analysis

Flat Past Returns Don’t Foretell Future Flatness

It is a behavioral mistake to let the last year's market action influence your view of the future.

While the recent correction seems to have subsided, many investors are weary of the market flatness that has lasted the better part of the past year, presuming recently flat returns predicts future flatness-or show the "old" bull is running out of steam. With recent volatility burned into their memories, many wonder whether they'll be rewarded for equities' volatility. It is true this has been an elongated period-over 300 calendar days-of basically flat returns. However, this isn't abnormal in bull markets historically-and it doesn't foretell weak or flat returns ahead.

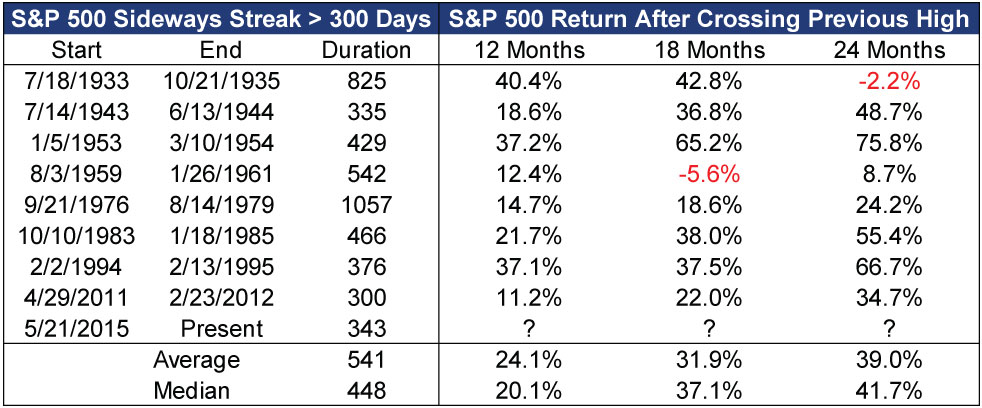

The present is the ninth flat period exceeding 300 days during bull markets since 1926 and, as Exhibit 1 shows, average returns over the 12, 18 and 24 months after they ended were solidly positive. We aren't arguing past flatness suggests big returns ahead-rather, we're telling you there is nothing predictive about flat periods whatsoever. Allowing past market returns to cloud your outlook is a behavioral investing error-it's why past-return drunk investors fail to see faltering fundamentals in a bubble. Fretting flatness foretells flatness is the same behavioral error, only a more pessimistic flavor.

Exhibit 1: Flat Point-to-Point Returns in Bull Markets Don't Foretell Weakness

Source: Global Financial Data, Inc., as of 4/28/2016. S&P 500 price returns, 1/2/1930 - 4/27/2016.

Note also, the recently flat returns are point-to-point only, which highlights a common thread in elongated flat periods: In eight of the nine periods shown, stocks suffered a correction (a short, sharp, sentiment-driven drop exceeding -10%). The exception, 1994's flat period, didn't breach -10% down, but it came close (-8.4% at its nadir).[i] Corrections never predict future returns, and they don't tell you how long a bull has left. Heck, the recent correction is this bull market's sixth since its 2009 birth, which shows such moves aren't predictive.

So don't let the correction-induced flat point-to-point returns over the last year skew your view of the path forward. And, always remember, if you need equity-like returns to finance your longer-term goals, you must be in stocks the vast majority of the time. Absent a reason to think a bear market (a lasting, fundamentally driven decline exceeding -20%) is forming, we believe the risk is higher to be out than in.

[i] Source: Global Financial Data, Inc., as of 4/28/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis New Tax Year, More British Business Tax Fear2026-04-08

-

Market Volatility How Investors Should Think About the Ceasefire2026-04-08

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today