Personal Wealth Management / Market Analysis

Flat Year Yields Flat Fear

Don't fret flat returns-they aren't predictive.

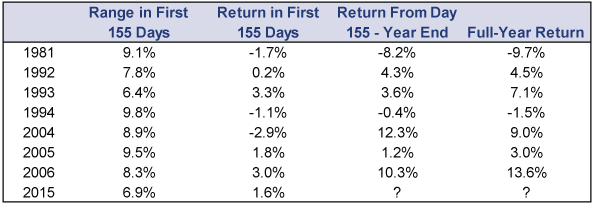

Are stocks stuck? Through Friday's close-155 trading days in-the S&P 500 was up 1.6% year-to-date. Its trading range-percentage difference between the year-to-date high and year-to-date-low-was just 6.9%, the second-lowest on record. The Dow's range was 6.7%, the lowest in its 100-plus-year history, leading many to decry it as setting a "record for futility." One firm declared "flat is the new up" and warned the world to be satisfied with another 0.4% in gains this year. Our take? These are just a bunch of interesting observations with no predictive power. Wherever stocks go over the rest of the year has nothing to do with the past 155 trading days.

We're great fans of history, but the history of similarly range-bound years tells you nothing. Since 1929, we've had just seven other years whose range in the first 155 trading days was below 10%: 1981, 1992, 1993, 1994, 2004, 2005 and 2006.[i] There is no pattern, rhyme or reason to returns over the rest of the year:

Exhibit 1: Some Arbitrary Factoids About Range-Bound Years

Source: FactSet, as of 8/17/2015. S&P 500 Price Index, 12/31/1980 - 8/14/2015.

The only takeaway from any of this, as far as we can tell, is that this year's relative flatness is rare. Big(ger) volatility is much more normal, to the extent anything in investing is "normal." Hence, we'd expect volatility to make a comeback at some point. Not necessarily tomorrow, and we aren't saying calmness begets big volatility. Past volatility (or lack thereof) doesn't predict future volatility any more than past returns predict future returns-which is to say, it doesn't. But the sheer frequency of higher volatility tells us the future is much more likely to be swingin' than not. In other words, don't let the flat wobbles lull you into thinking stocks won't do much over the foreseeable future, for good or ill.

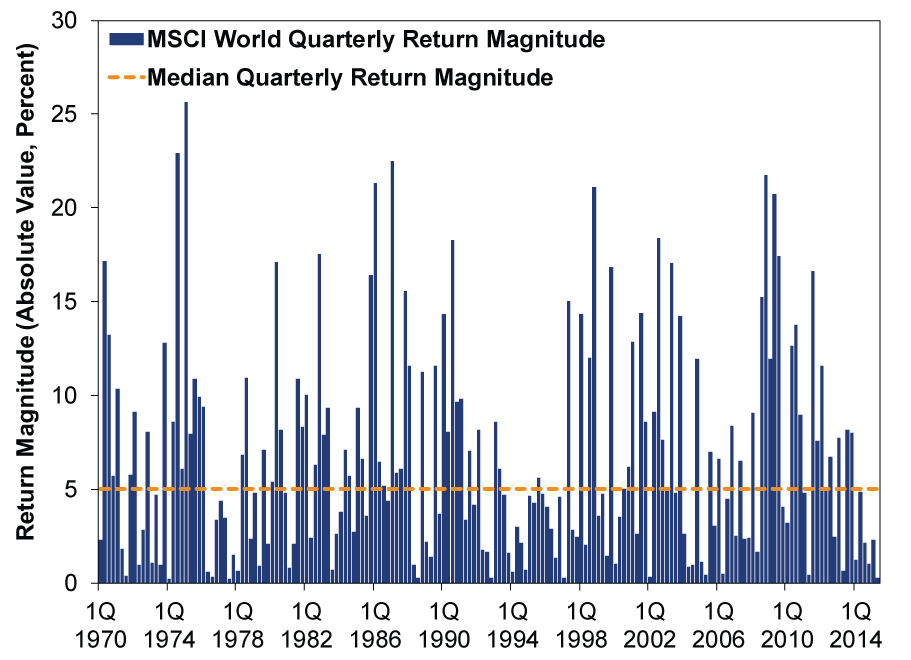

World stocks have a smaller dataset-the MSCI World Index began in 1970-and daily returns are available only to the late 1970s, but that index's quarterly volatility tells a similar story. Since the MSCI World Index was born, its median quarterly move is just over 5% up or down. World stocks last exceeded that magnitude in Q3 and Q4 2013, when they rose 8.2% and 8.0%, respectively. World stocks are up more than the S&P this year-3.3% through 8/14 (a factoid missed by most US-centric investors)-but have been similarly quiet, volatility-wise, for over a year.

Exhibit 2: MSCI World Quarterly Return Magnitude (Absolute Value)

FactSet, as of 7/8/2015. Absolute value of MSCI World Index quarterly returns with net dividends, 12/31/1969 - 6/30/2015.

Don't let the calm fool you: Stocks move fast. Since 1969, during bull markets, world stocks have exceeded that median quarterly return magnitude 72 times. Of those, 61 were positive. World returns are also frequently back-end loaded during bull markets, with roughly 40% of second halves since 1970 up double digits.

Most folks equate volatility with downside, but volatility cuts both ways-up and down. It won't take much upside volatility-the good kind of volatility-for stocks to achieve a nice bull market year. Plus, calendar years are pretty arbitrary. Don't get us wrong, we're still bullish and expect strong returns this year. But we also remember 2005. World stocks rose 7.1% that year, which is a-ok. But push your start date forward a month, to 1/31/2005, and forward 12-month returns jumped to 17%. Does it really matter if returns come between December and December or January and January? Bull markets are bull markets.

Besides, as far as we're concerned, a market forecast has one purpose: to help you figure out whether or not to own stocks. Bull market? Own stocks. Bear market? If more of the downside lies ahead of you than behind you, then reducing equity exposure can help. Flat market? As long as it's a flat market within a bull, then owning stocks is the right move for long-term growth investors.

And that's what we think we've gone through recently-a flat period in a bull market. The global economy is growing and looks set to keep doing so, as strength in the US, UK, eurozone and East Asia (ex. Japan) offsets weakness in heavy commodity producers. Politics are calm, with gridlocked governments throughout the West unable to meddle much. Sentiment is still quite tame and bordering on skeptical. There is plenty of "wall of worry" left for stocks to climb! That climb should resume at some point. No one can say when, but don't let any of this "flat stocks are soooo terrible" handwringing make you think otherwise.

[i] Those arguing stocks have gotten much more volatile over the years should probably take note that these tame periods cluster in recent years.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History COVID-Panic’s Lockdown-Low Anniversary2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today