Personal Wealth Management / Market Analysis

Gold: The Pyrrhic Hedge

What are you willing to pay for this mythological hedge?

Gold is down.

Yes, we know, you don't need to come here to find that pithy, to-the-point observation. That is all over the news, triggering a wide array of ruminations about what it all means. But the thing we find striking is that the media seems to think this is new, surprising, big news. It is none of those, of course, and we continue to believe gold has little-to-no place in a long-term investor's diverse portfolio.

For years, gold has been a hot topic among investors. Newsletter writers hock it. Pundits and commentators speculate wildly on how high it will rise. Some even try to divine the true size of China's unpublished gold holdings (in metric tonnes, of course). Yet for all the talk since 2009, owning gold versus stocks during this bull market has most often been the wrong move. That's right, gold-something we're often told has an inherent value[i]-hasn't added value during most of this bull market.

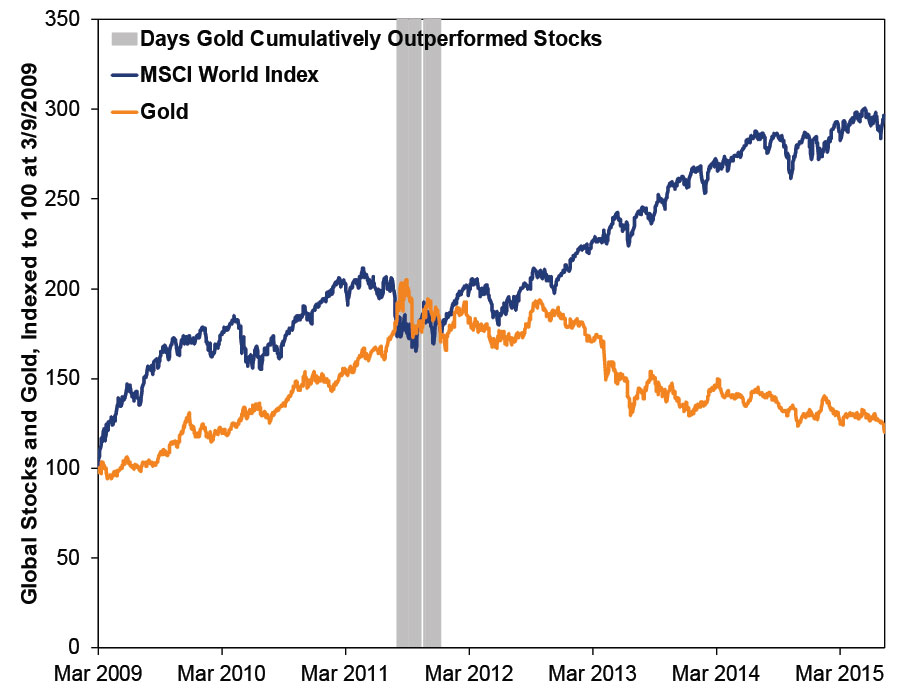

It might shock you to learn that since March 9, 2009-the end of the financial panic-gold is up just 19.6% cumulatively. By contrast, world stocks are up 196.4%. That is not a typographical error; gold is up only one tenth as much as stocks. Viewed another way, the equity bull market, through Monday's close, is 1,661 days old. Gold's cumulative return exceeded stocks' for only 80 of those days, all of which fell between August 8, 2011 and December 12, 2011. (Exhibit 1) That's it! And that isn't even dating from gold's September 5, 2011 peak. Since then, Au is down a whopping -41.7% while world stocks are up 69.1%. Put simply, there is far too much supply of gold relative to demand (like many commodities).

Exhibit 1: Above the World for 80 Days

Source: FactSet, as of 7/21/2015. MSCI World Index returns with net dividends and gold returns, indexed to 100 at 3/9/2009. 3/9/2009 - 7/20/2015.

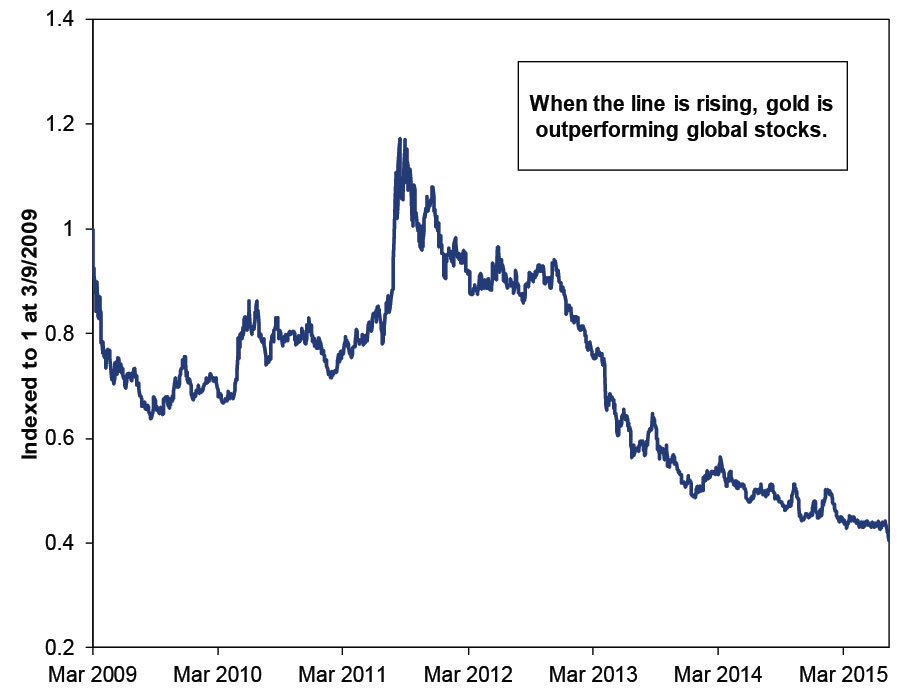

Now, each of these is dating to the start of a cycle-the equity bull in the former case, the golden bear in the latter. Yet the point remains: Vastly more often than not in this cycle, gold has been a drag relative to stocks. Exhibit 2 shows gold returns divided by world stocks-when the line is rising, gold is outperforming. It just isn't rising very often in this cycle.

Exhibit 2: Gold and Stocks

Source: FactSet, as of 7/21/2015, Gold and MSCI World Index returns with net dividends, both indexed to 1.

Some will argue this is all just returns, and the reason you buy gold is to hedge against something (inflation, deflation, equity bear markets, war, panic, etc.). Now, we don't believe it actually hedges against any of those things (as many have discussed lately). But even if you believe gold is a hedge, our question today is, "At what cost?"

Hedges have prices, and for gold, that cost is missed opportunity in equities, primarily. Exhibit 3 shows you the various opportunity costs of hedging with gold in this cycle from our two starting dates. We assumed the investment of $1,000,000 with varying allocations to gold and compared that to 100% stocks over two time periods: The beginning of the equity bull market through the present; and the beginning of the golden bear through the present.

Note: In both cases, even a 10% allocation to gold has a six-figure price tag. So, considering that, is it worth it?

Exhibit 3: The Opportunity Cost of Au - Hypothetical Growth of $1 Million in Various Allocations

Source: FactSet, as of 7/21/2015. Gold and MSCI World Index returns with net dividends.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today