Personal Wealth Management / Economics

Golly Gee Whiz Willikers, It’s Q3 GDP!

We looked at the second estimate of Q3 US GDP so you didn't have to.

Coming off the Thanksgiving weekend (perhaps with some new gizmos and gadgets from Black Friday), investors were treated with more positive news on Tuesday: The US economy grew a little quicker than initially projected-and the advance estimate was already the fastest rate in two years! So proclaimed the Bureau of Economic Analysis (BEA) in its second estimate of Q3 GDP. While this says nothing about America's near-term prospects, it does provide further evidence the economy stands on solid ground.

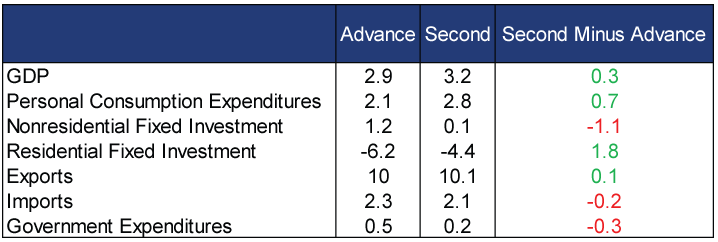

The second estimate of Q3 GDP was revised to 3.2% annualized, slightly higher than the advance estimate's 2.9%. Personal consumption expenditures (consumer spending), which comprise approximately two-thirds of economic output, was revised up from 2.1% to 2.8%. On the not-as-positive front, business investment was shaved down from 1.2% to 0.1%. Real estate investment was revised up from the initial estimate's -6.2%, but still negative (-4.4%).

Exhibit 1: Advance vs. Second Estimates of Q3 2016 GDP and Select Components

Source: BEA, as of 11/29/2016. All figures are seasonally adjusted annualized rates.

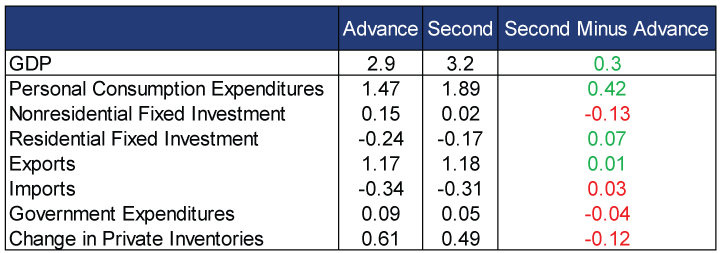

When everyone cheered the initial estimate's acceleration, we noted the uptick was mostly due to a rise in some of GDP's "squishier,[i] more volatile components" like a one-off surge in soybean exports, inventories and government spending, while the pure private sector components were in line with their longer-term trend. Still growing fine, but not suddenly stronger. The same is true in the second estimate. Inventories were revised down a bit but still contributed about half a percentage point. Imports were revised lower, but GDP math counts this as positive (even though they represent domestic demand, which, last we checked, is important). The positive revision to consumer spending is nice, but business investment's downgrade isn't exactly great-especially when you consider R&D investment fell -5.4%, which is a sign you can't tie all the weakness to oil. (Though oil did play a big role, judging from the -30.1% and -17.6% declines in mining investment and transportation equipment, respectively.) Then again, some choppiness is normal, and R&D spending was coming off Q2's 17% jump. So we wouldn't draw sweeping conclusion from one bumpy quarter.

Exhibit 2: Revisions to Contributions to Percent Change of Q3 2016 GDP

Source: BEA, as of 11/29/2016. All component figures are in percentage points.

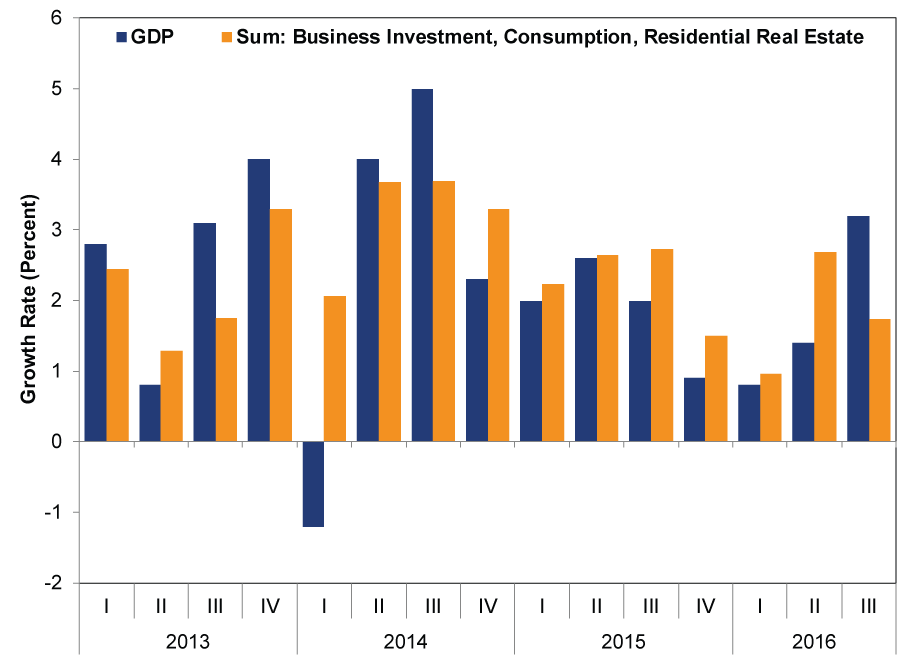

Plus, when you isolate the pure private sector components-consumption, business investment and residential real estate-Q3 remains in line with recent quarters.

Exhibit 3: Headline GDP vs. Sum of Private Sector Components

Source: BEA, as of 11/29/2016.

The BEA also released the first estimate of Q3 corporate profits, which rose $133.8 billion (6.6%) annualized-quite the turnaround from Q2's -$12 billion (-0.6%) decline. Domestic nonfinancial corporations' profits grew the most, rising $76.5 billion (6.5%) and erasing Q2's -$56.1 billion decline. Domestic financial corporations' profits grew $50.9 billion (11.5%).

Q3 S&P 500 corporate earnings echo this. As of 11/25/2016, 493 companies have reported and earnings growth is expected to be 3.2% y/y-much better than preseason estimates of -2.0%.[ii] Excluding the long-struggling Energy sector, earnings are up 6.7% (exceeding expectations of 1.3%). Soon Energy should be less of a drag. Oil prices have stabilized a bit and the year-over-year comparisons are more favorable now that higher oil prices are out of the calculation. With this skew going away, S&P earnings should be even higher in the next few quarters.

While GDP and corporate earnings are backward-looking, they do confirm things weren't nearly as bad as many folks feared, which may allow investors to finally start feeling a little sunnier. Remember all those concerns about an "earnings recession" earlier this year? S&P 500 earnings have been in the red since Q2 2015, but exclude Energy, and they contracted only once during that stretch. More notably, that "earnings recession" didn't portend broader trouble. GDP kept growing and has accelerated over the year. Better-looking data make extant underlying trends more visible to the investing world, which can help those mythical animal spirits. We aren't arguing investor sentiment has definitively turned the corner and will become broadly optimistic, as skepticism has been unusually dogged during this bull market. But a bit of extra cheer is in the air these days.[iii]

As a friendly reminder, Q3 GDP will be revised again, many times, over many years. But future revisions should mean little to nothing for stocks-they have already priced and moved on from whatever happened in July - September. However, forward-looking indicators like The Conference Board's Leading Economic Index (LEI) suggest near-term growth prospects look solid, providing more fuel for earnings.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today