Personal Wealth Management /

Great French-Pectations

Investors might not love French policy, but French stocks don’t seem to mind.

Lately, it seems in vogue for investors to snub France—the economy is struggling, unemployment is historically high, taxes are rising, economic policy seems a touch confused and voters aren’t happy. Yet while investors have largely turned their noses at the Fifth Republic since Socialist President FranÇois Hollande was elected last May, a funny thing has happened to French stocks: They’ve outperformed. And hard as it is for many to believe, investors’ rock-bottom expectations make France look pretty attractive looking forward.

Markets move most over time on the gap between expectations and reality. If investor expectations are high but reality doesn’t quite meet them, markets can slip. Conversely, if investors expect the worst, reality that’s just ok or even not terrible is a positive surprise, which can lift stocks. This seems to be the case for France these days.

At first blush, low expectations might seem warranted. Many recent policy proposals seem less than ideal for future growth. Exhibit A: Hollande’s proposed two-year 75% tax on incomes over €1 million. The initial income tax was later ruled unconstitutional, but Hollande persisted as the tax was a key campaign pledge and wildly popular with voters—not as a revenue raiser, but as a political statement. His new proposal is a 75% employer payroll levy on salaries over €1 million. Investors may not be great fans.

Why? Let’s run the numbers. Say a French company pays an employee €1.1 million. Since the crippling rate applies to the amount above €1 million, the company would have to pay €75,000 extra for the next two years. Multiply that by the number of high salaries a big, successful firm has on its books, and it adds up. That steals money from other avenues, like investing or purchasing new equipment—potentially limiting growth—and probably hurts profits. It’s also a big incentive to keep salaries under the effective cap, potentially robbing companies of a means of attracting top talent. The tax could deter also foreign firms from coming in, depriving France of investment. All of which, in theory, markets wouldn’t like.

The same goes for many French policies, old and new—France is no stranger to red tape. Many shops, for example, must close on Sundays. Hollande is weighing a change, but opposition is high. Meanwhile, other rules could get more restrictive. For example, Parliament is considering reducing the work week from 35 hours to 32, believing this will reduce unemployment because employers will hire more to maintain production. Noble as the intent is, the change would be a headwind. Hiring and training more workers take more money and resources—businesses might just try to get more efficient instead.

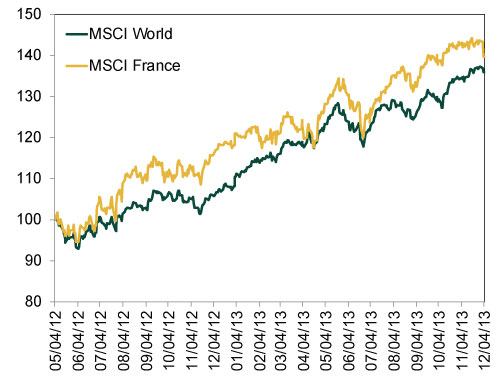

Add in a number of other tax tweaks and regulations, and you’d think investors would have any number of reasons to avoid France. Yet as Exhibit 1 shows, if an investor looked at these negatives alone and shunned France, they’d have a blind spot to one of the world’s better performing nations.

Exhibit 1: MSCI World vs. MSCI France Since 5/4/2012

Source: FactSet Data Systems, Inc., as of 12/4/2013.

Why?

As mentioned above, markets move most on the gap between reality and expectations. Throughout the eurozone, there has been a hefty gap between reality and expectations for several months. For example, most folks expected electing a Socialist leader would mean dire consequences for French stocks, but on top of outperforming the MSCI World since Hollande’s election (despite some typical wobbles and wiggles), France has also performed in line with the broader eurozone—a diverse region containing leaders from many political parties, legislation heading in various directions and economies of wide disparity in terms of competitiveness. Having a Socialist leader hasn’t carried a penalty—those biased by the label might miss that. As the region’s second-biggest economy, it benefits from the union’s continued improvement. Plus, none of Hollande’s proposals are a surprise—he campaigned on them as far back as 2011, giving markets plenty of time to deal with them before he took office. But many investors don’t realize this, keeping expectations extra low. This makes even just-ok news a positive surprise. Like, for example, Q2 GDP beating expectations (0.5% vs. 0.2%). Q3 GDP disappointed a touch but France’s positive LEI trend and widening interest rate spread suggest things will turn.

Plus, France isn’t the world—for many French firms, the world matters more. Many publically traded French firms are big multinationals. Their revenues depend on the entire world, not just France. Even if France muddles along for a bit, the global economy is growing, and many other counties appear to be reaccelerating. As Emerging Markets have grown, more and more consumers have moved up the income spectrum, spurring demand for luxury goods, apparel, cosmetics and other products offered by French retailers. Many French firms have healthy and growing market share in these nations, and their strong brand-name recognition should help them grow their foothold. Granted, France’s complicated business conditions and tax policies could create a few headaches, but these don’t always have the sweeping impact many assume—firms often find ways around them. They can shelter revenues in tax-friendlier jurisdictions, move major production to more accommodating business environments or hire employees in countries where higher-paying salaries don’t draw the taxman’s fire.

There is also potential for French policy to exceed expectations, providing a general sentiment lift. Investors’ reactions to Hollande reminds me of how markets respond to US presidential elections. Investors generally believe Democratic presidents aren’t great for business, which drives down expectations when they win, creating room for markets to be happily surprised when Democrats turn out not to be as hostile to business as feared. We’re already seeing signs Hollande isn’t quite as anti-business as many believe, and he could easily moderate further. Proposals aren’t laws—they can be watered down or abandoned. Hollande has already backed away from some tax proposals, like levies on agricultural trucks or savings accounts and taxes on businesses’ gross operating profits. In recent days, Prime Minister Jean-Marc Ayrault even vowed to overhaul—and simplify—France’s tax code over the next year. I wouldn’t be surprised if this trend of moderation continued. The proposed 75% tax lasts only two years. While temporary taxes can become permanent, if this one takes effect and impedes growth, Parliament can let it expire. Hollande’s reward for campaign promises is the lowest approval rating of any modern French president—voters don’t like wobbly growth. He has a powerful incentive to pass policies enabling businesses and households to bounce back.

That’s something few expect—along with ok growth and globally successful French businesses—which suggests there are nice opportunities for investors who can look past some occasionally discouraging developments. It may seem counterintuitive to some, but successful investing is often about going against conventional wisdom, doing what others think is wacky. So be a little wacky—vive la France!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today