Personal Wealth Management / Market Analysis

Greece Is the Word, Not the World

In the 99.8% of global GDP that isn't Greece, evidence suggests economic expansion continues.

With most eyes focused elsewhere (ahem, Greece), investors might have overlooked some tidbits of data confirming the global economy continues plowing forward, undeterred by the Hellenic Republic's drama. Most of these numbers didn't make the front page, but they suggest the bull stands on a firm economic ground-and this doesn't look likely to change in the near future.

Let's start with retail sales, which rose and beat expectations in America and Britain last month. While retail sales have limitations, they indicate consumer spending-a large component of economic activity-is doing just fine. US sales jumped up 1.2% m/m (2.7% y/y), prompting relief that consumers were "finally" spending their gasoline savings after months of lackluster retail results-with almost no discussion of the fact that retail sales largely omits the service sector (where most consumer spending happens). In the UK, headlines were more optimistic about the 0.2% m/m (4.6% y/y) rise, even though it was slower than April's 0.9% m/m-they simply concluded consumers were spending their extra cash on services, not gadgets and baubles. Which seems about right to us, considering the UK's retail sales gauge excludes food service, making it even narrower than the US's gauge. Full consumer spending is what matters, and retail sales won't tell you much about that, whether it's the US's jump or the UK's slowdown. Plus, it was always presumptuous to say falling oil and gas prices are big economic stimulus. Sure, they help consumers, but folks always had three choices when it comes to their gas savings: save, pay down debt or shop.

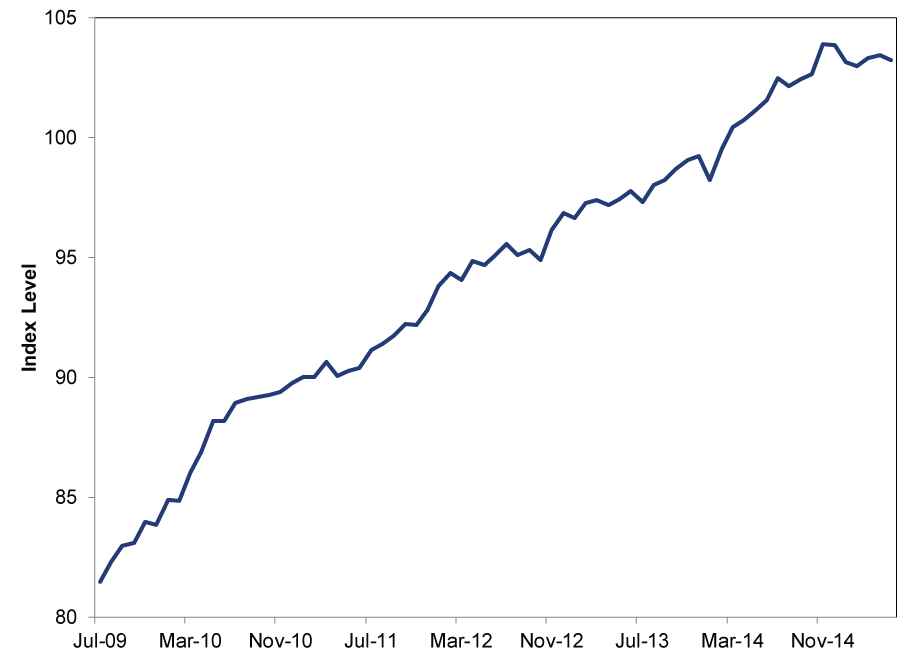

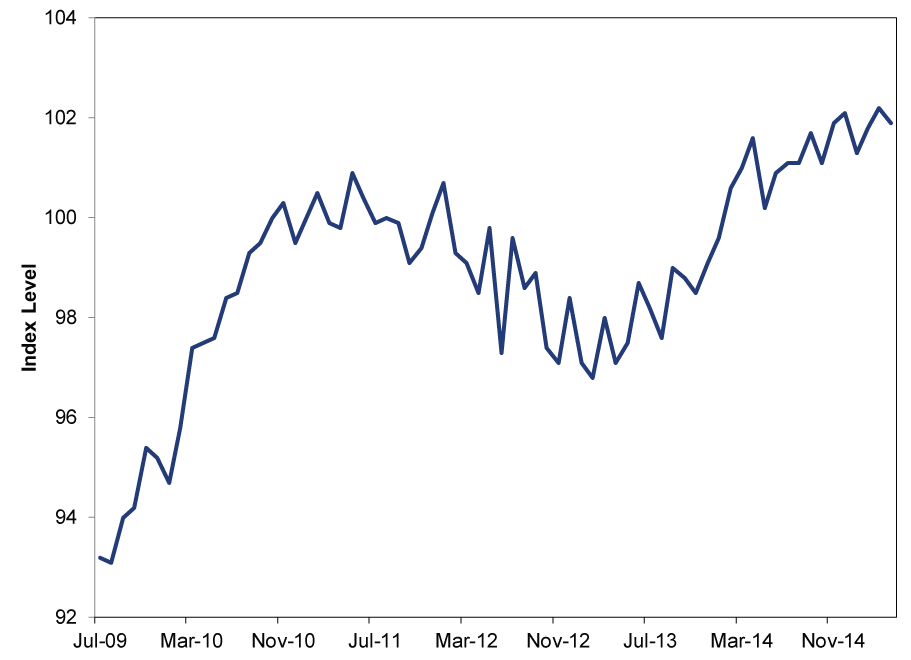

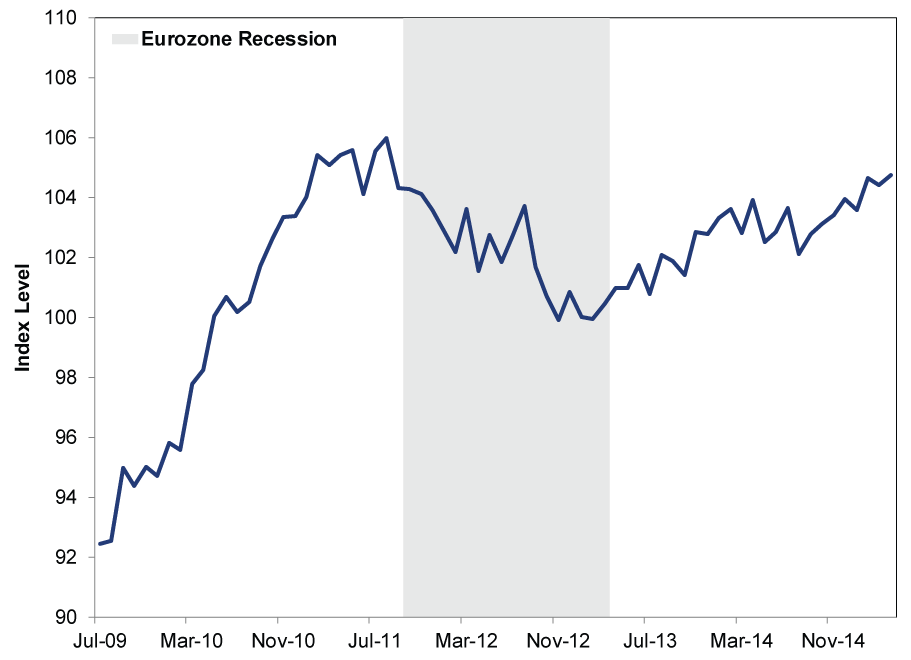

The week's industrial production data were less rosy, but we wouldn't make much of it-the developed world's factories haven't led this expansion. In the UK, April industrial production rose 0.4% m/m (1.2% y/y)-its third straight monthly rise-but mining and quarrying drove the increase. The narrower manufacturing gauge, which better reflects UK factories, contracted -0.4% m/m. Manufacturing also contracted -0.2% m/m in the US in May while industrial production missed expectations-dropping -0.2% m/m. Eurozone industrial output ticked up on a monthly basis in April-0.1% from March's -0.4%--though the year-over-year number was lower (0.8% vs. 2.1%). Some good, some meh, but all consistent with the trends we've seen throughout this expansion-choppy, uneven growth. The month-to-month bumpiness in industrial and manufacturing output hasn't prevented these regions' economies from growing overall. We don't see much (if any) evidence today's wobbles are different than past wobbles.

Exhibit 1: US Manufacturing

Source: St. Louis Federal Reserve, as of 6/23/2015. Industrial Production: Manufacturing (NAICS), seasonally adjusted, monthly, from July 2009 - May 2015.

Exhibit 2: UK Manufacturing

Source: Office of National Statistics, as of 6/23/2015. Index of Production, Manufacturing, seasonally adjusted, monthly, from July 2009 - April 2015.

Exhibit 3: Eurozone Manufacturing

Source: Eurostat, as of 6/23/2015. Index of production, Manufacturing, seasonally adjusted, monthly, from July 2009 - April 2015.

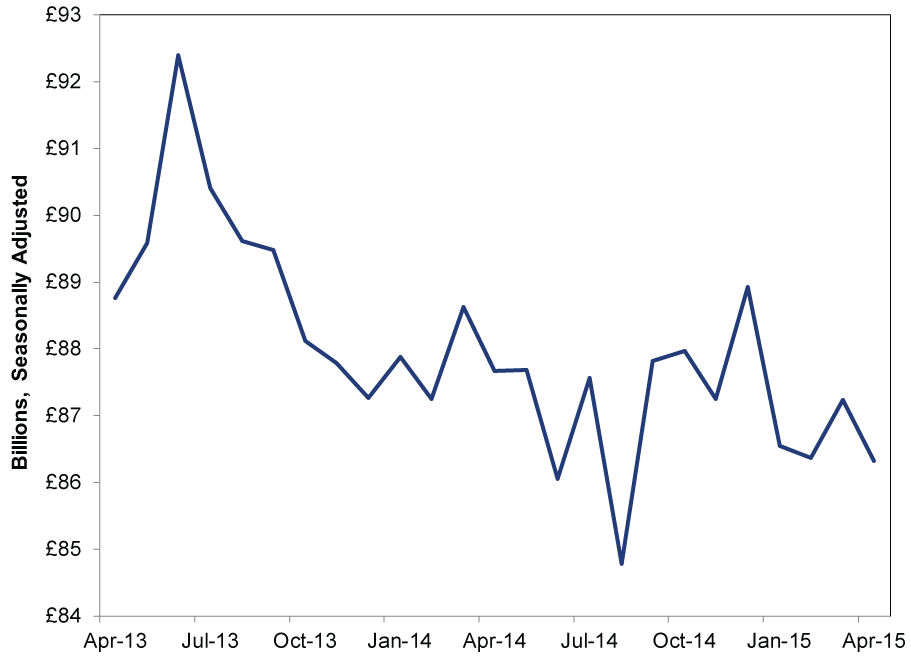

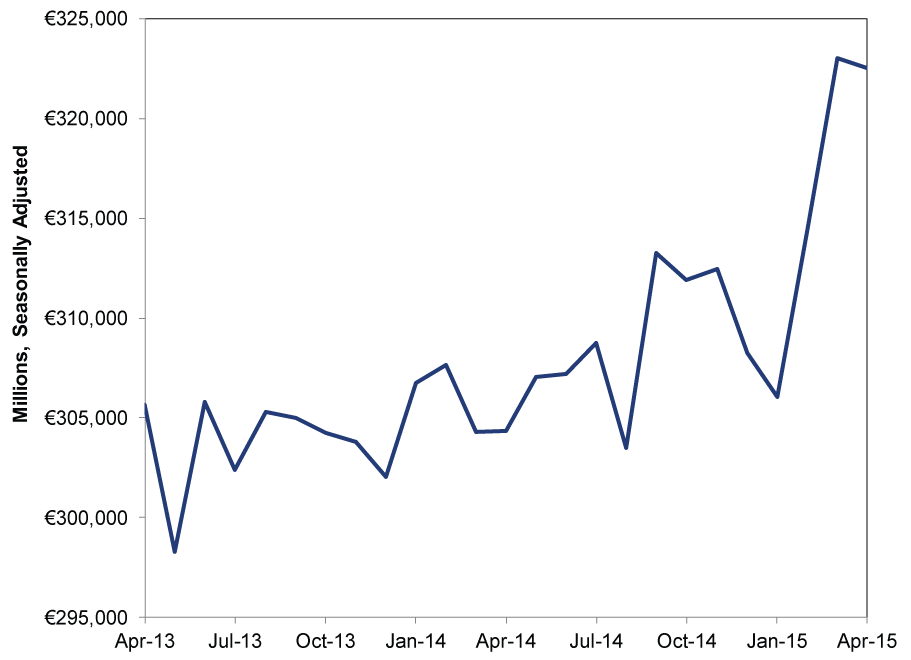

Same goes for trade, where the latest data were also mixed. Headlines often focus on trade deficits, but we think total trade-exports plus imports-is far more meaningful, as imports measure domestic demand. In April, both the UK and eurozone saw export numbers rise a bit and imports slide. UK export values climbed 1.2% m/m and imports drew back -3.1% m/m-a total trade pullback of -1.0% m/m-while eurozone goods exports rose 1.1% m/m and goods imports contracted -1.6% m/m, causing total trade to slide -0.2% m/m. But these monthly moves are in line with the UK and eurozone's total trade longer-term trends. UK trade has barely budged this entire expansion (Exhibit 4), yet it hasn't prevented the UK from being one of the developed world's fastest-growing economies. Eurozone trade has shown more of an uptrend (though still a choppy one), and it has jumped this year thanks to rising exports, making April's small dip a timely reminder monthly numbers are volatile. (Exhibit 5)

Exhibit 4: UK Total Trade

Source: Office of National Statistics, as of 6/9/2015. From April 2013 - April 2015.

Exhibit 5: Eurozone Total Trade

Source: Eurostat, as of 6/23/2015. From April 2013 - April 2015.

Japan's provisional May trade numbers, however, were just plain weak: Export volumes contracted -3.8% y/y and import volumes dropped -5.3% y/y. Japanese exporters still saw a small gain from currency conversions as export values rose 2.4% y/y, but that is where the good news ends. Yet the global economy doesn't need a rollicking Japanese expansion for global growth to continue. Japan has had three recessions since the global expansion and bull market began. This is just a testament to the fact pockets of strength and weakness persist-and can persist without derailing the bull.

But everything we just mentioned is in the past-what is to come? According to The Conference Board's Leading Economic Indexes (LEI), more growth. US LEI rose 0.7% in May, repeating April's sharp uptick, with (once again) strong contributions from the yield curve spread and Leading Credit Index. April UK LEI advanced for the fifth straight month (0.4%), putting last autumn's brief decline further in the rearview mirror. Japan's LEI stopped falling in April, ending the four-month decline, though we wouldn't exactly shout that from the rooftops-LEI trends take time to develop. And the trend is what matters. For instance, no recession in US LEI's 55-year published history has started while the index was high and rising (like it is now).

In our view, these tidbits taken together matter a whole lot more than the prominent false fears splattered across headlines (ahem, Greece). Now, the world isn't growing uniformly, but it almost never will. However, that the crowd stresses over the occasional weak reading keeps expectations-and sentiment-low, which should give this bull market plenty of room to run and "wall of worry" to climb.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Excess Fear Over ‘Excess’ Profits2026-06-25

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US PCE Inflation, Annuities

2026-06-22

2026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today