Personal Wealth Management / Market Analysis

Greek Debt Talks Start With a Shocking Twist

Everyone left "emergency" talks happy and optimistic, but don’t hold your breath just yet.

Greece is back in the headlines, and in years gone by, this would mean the world's most entertaining political circus is back in town. But it seems times have changed. Even though it had the attendant protests and Molotov cocktail-throwing, Sunday night's austerity vote didn't threaten to take down the government. Monday's emergency meeting of eurozone finance ministers (aka the "Eurogroup") was a hug-fest, not a shouting match, and Greece's rep wasn't mentally water-boarded. There were no threats, lines in the sand or ticking time-bombs. No one called anyone else a criminal, as far as we know.[i] (We know, shocker, right!?!) There wasn't a deal, but-in grand eurozone tradition-they agreed on a plan for a plan, and everyone left happy. So happy you might even question why we're writing this, but six years after the first bailout, we know better than to hold our breath. Greek negotiations have a long history of collapsing on the home stretch, and this round could still implode before Greece's next big payment is due in July. Consider this your advance notice-and reminder that whatever happens in Greece, global stocks shouldn't much care.

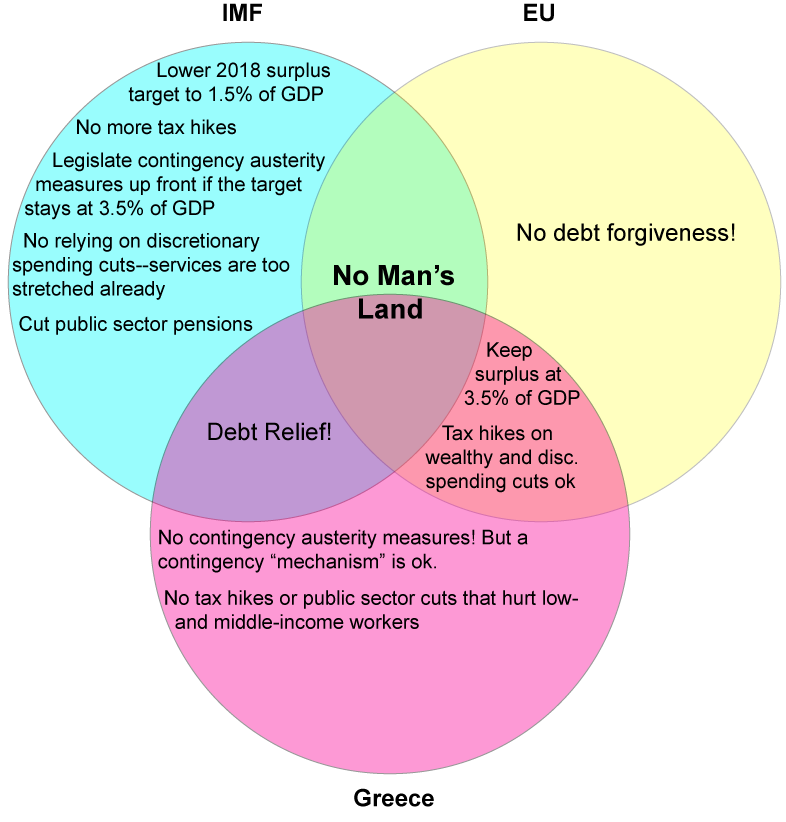

This time Friday, it didn't look like things would go this well. Greece still hadn't passed the reforms necessary to pass the first checkpoint in last July's bailout-a review process that has dragged since last autumn. Meanwhile, the Greek government, still hung up on a leaked IMF teleconference transcript that implied the IMF was keen on pushing Greece to the brink to force a compromise, was accusing the organization of unnecessarily stalling the review. To clear her name, IMF chief Christine Lagarde sent the Eurogroup a letter explaining her beef with Greece and Europe's progress and outlining the IMF's additional demands. (Naturally, it leaked.) In response, Greek fin-min Euclid Tsakalatos sent his own letter basically saying, no way. Exhibit 1 illustrates the state of the debate as Parliament convened Sunday using the Cadillac of Explanatory Images, the Venn Diagram.

Exhibit 1: Who Wanted What

Source: Art.

Needless to say, the gaping hole in the middle looked like a problem. Not a Critical Week for the EuroTM problem, as Greece doesn't technically need its money till early July, but getting there. EU leaders don't want to do anything Greece-related during the final weeks of the UK's "Brexit" referendum campaign, lest they do something to alienate UK voters. Britain's referendum is June 23, so leaders wanted the Greek saga wrapped by May 24's Eurogroup-otherwise, it would be crunch time after the referendum.

But then stuff started happening. Greece passed a suite of measures to broaden the tax base, raise the VAT and other taxes and overhaul the pension system-including cutting payouts and raising worker contributions. European Commission President Jean-Claude Juncker took stock and said Greece had "basically achieved" the first review's conditions, and they could start talking about debt relief. German Vice Chancellor Sigmar Gabriel called Greek debt relief a must. Finance ministers arrived to the Eurogroup meeting with big smiles and left with even bigger smiles and a roadmap to compromise on the last issue between Greece and its money, those contentious contingency austerity measures. To placate the IMF, Greece and the eurozone decided to play along with the request, but they used Greece's proposal as the baseline and just gave it a couple more teeth. Instead of legislating more cuts and whatnot up front-which would have almost no chance of passing-they'll pass a rule allowing the President to enact "across the line" cuts by decree if they miss budget targets. Greece now has two weeks to get this done.

Amazingly, even debt relief got a hearing and a roadmap. Eurozone leaders are still opposed to outright forgiveness, so the IMF's goal of taking Greece's debt from 180% of GDP to 120% was a nonstarter. Instead, they dropped all references to debt-to-GDP and considered Greece's "annual gross financing needs" and debt affordability-and created a three-step plan. Between now and 2018, when the bailout finishes, they will investigate "optimizing Greece's debt to lower repayment costs." In 2018, if Greece meets all its commitments and still needs help, they'll probably lower interest rates or extend maturities. And if, in the long run, Greece behaves but still needs relief, they'll cross that bridge when they come to it.

Now, there is still a lot of room for this to fall through. A lot. The IMF still hasn't signed up, and the eurogroup won't do anything without the IMF-eurozone leaders (specifically German Chancellor Angela Merkel) could never sell it to their Parliaments or voters. Greece still must pass that contingency mechanism. And, based on six years of evidence, they could all change their minds tomorrow.

So while Greece seems well on its way to getting its money on May 24-and several eurozone finance ministers have said it looks likely-we don't blame anyone for being skeptical. But whether they kick the can again or talks implode, the market impact should be minimal. We've had six years of Greek can-kicking now, and it hasn't stopped the bull market. Nor did countless stalemates, two defaults in 2012, multiple fallen governments and Greece's missed IMF payment last year. The euro crisis did cause a deep correction in 2011, but the world has moved on since then. The euro's very survival doesn't depend on Greece's continued membership. The financial system is backstopped, firewalled or whatever metaphor you prefer. People fear for eurozone banks, but their Greek exposure is minimal-they took massive haircuts in that first 2012 default. Most Greek debt now belongs to eurozone governments, the ECB, the IMF and vulture funds, all of whom are well equipped to take a loss in a few decades when it comes due, if need be.

Markets have long known there are three outcomes where Greece is concerned: They kick the can repeatedly, they default and stay in the euro, or they default and "Grexit." The Grexit possibility has confronted global stocks time and time again, with less visible impact each time. There is simply no shock factor, and surprises move markets.

[i] Yes, we know, you could probably throw a "...yet" at the end of all these sentences.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today