Personal Wealth Management / Economics

(Growth) Dashing Through the Year

Thursday bore gifts a little early as indications of US growth continued and Congress reached an agreement.

The march toward the end of 2011 continued Thursday, bearing perhaps not-so-surprising gifts for the astute-minded investor. Despite consternations about European debt troubles sinking the US economy, indications of growth actually continued: LEI figures dashed, US economic growth danced and new jobless claims pranced.

LEI

The Conference Board’s US Leading Economic Indicator Index increased 0.5% in November to 118.0, following similar increases in October and September. In fact, the index has risen fairly consistently since March 2009—30 of 32 months. Recall, the index derives its value from 10 economic variables thought to best capture the country’s economic direction, while smoothing out volatility in any one metric. As with any indicator that aims to be forward-looking, LEI is imperfect, and we caution against considering it a crystal ball. However, it is true in the last 50 years a recession has never closely followed a rising LEI trend. See Exhibit 1.

Exhibit 1: US Leading Economic Indicator Index

Source: Thomson Reuters.

GDP

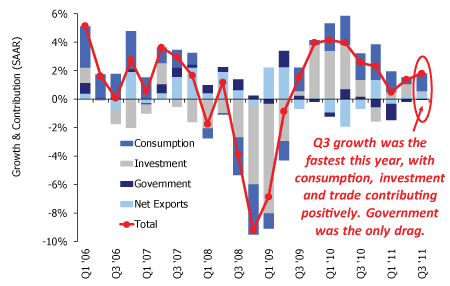

The third estimate of Q3 2011 real GDP was revised down to 1.8% (at a seasonally adjusted annualized rate) from the 2.0% second estimate. Tepid as it may be, this is still an acceleration from 1.3% growth in Q2. The downward revision reflected lower than previously estimated personal consumption growth (revised to 1.7% from 2.3% in the previous estimate.) However, about half the downward revision to consumption reflected additional spending on imports (a detractor from GDP) than previously estimated, rather than a decline in overall demand. Blame it on the somewhat wonky construction of GDP. Additionally, an unexpected increase in business investment (up 1.3% from a previously estimated 0.9% decline) was a positive. In fact, reined-in government spending—a factor the last several quarters—was the only material drag on the release. See Exhibit 2.

Exhibit 2: GDP Growth and Component Contribution

Source: Thomson Reuters, Bureau of Economic Analysis.

Of course, GDP is an imperfect indicator of US economy’s health and subject to revision again down the road (as discussed here). However, right now, it’s the best indicator we have of the country’s economic health, and the general trend over the last nine quarters indicates solid growth—despite consternation otherwise.

Jobless Claims

Unemployment has indisputably remained high following the recession’s end (a not-unusual occurrence). However, recent unemployment reports have shown signs of improvement. The BLS reported new weekly initial jobless claimed fell by 4,000 to 364,000 last week—the lowest level since June 2008. Continuing claims likewise fell 79,000 to 3,546,000—the lowest since September 2008. That said, even if the actual December unemployment rate does drop next month, it’s still elevated above the historical average. And high unemployment may continue to be an issue for some time to come. But remember: Unemployment reflects past economic weakness—in this case, a recession that ended over two years ago. As the economy continues to grow (as evidenced by the aforementioned LEI and GDP releases), expect private enterprise to continue adding jobs and working off unemployment rolls.

Another Kind of Holiday

Congressional leaders finally agreed to extend the much-debated payroll tax “holiday” by two months and begin negotiations on a yearlong extension. Recall earlier this week, the House rejected a Senate-approved bill to extend payroll tax cuts, arguing a yearlong extension would be better. The Senate, however, was already in winter recess. Had a last-minute agreement not been struck between House Republicans and Senate leadership, payroll taxes would revert to 6.2% from 4.2% on 12/31/2011. An unexpected holiday gift? Maybe not. This opens the door for more politicking early next year. What’s more, as much as we prefer letting workers keep more of the money they earn, in our view, small, temporary tax cuts like these aren’t nearly as impactful as proponents hope. Still, getting to keep 2% more of your hard-earned money is better than a lump of coal.

Merry Christmas and Happy Holidays!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Market Analysis Stablecoins Didn’t Eat the Treasury Bill Market2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today