Personal Wealth Management / Market Analysis

Happy Downgrade Day!

S&P downgrades US. World doesn't end.

Six years ago Saturday, Standard & Poor's downgraded the US from AAA to AA+, which many feared sounded the death knell for US debt, rendering America the next Greece-as if taking an A off America's credit rating would send buyers fleeing and pave the way for default. It was, on all accounts, a circus. After S&P officially announced the US would join such debt-ridden basket cases as Belgium and New Zealand[i] in the AA+ club that Friday evening, they got in a war of words with the White House-which was all too happy to point out a $2 trillion error in S&P's math. So the rater scrambled, re-pinned its decision on Congress for taking too long to raise the debt ceiling earlier that week, and made plans to hit the talk show circuit bright and early Monday morning to really whip up the frenzy. Apparently they were successful: The S&P 500 plunged 6.6% that day, and pretty much everyone feared the 21st century's second financial crisis was here.[ii] Meanwhile China seized the moment, lambasting America's "debt addiction" and calling for a new global reserve currency. Chicken Little was probably running around, too.

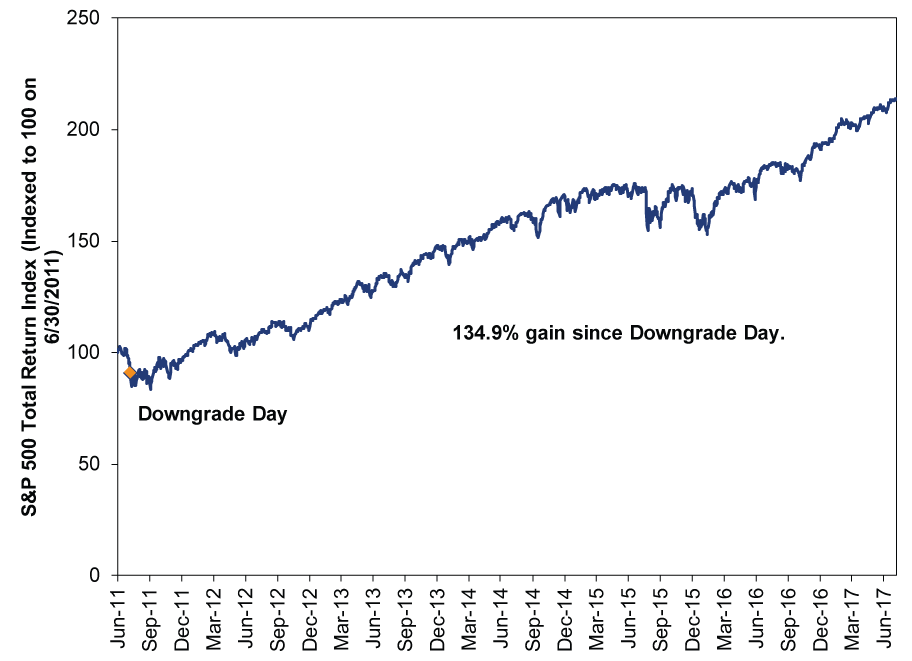

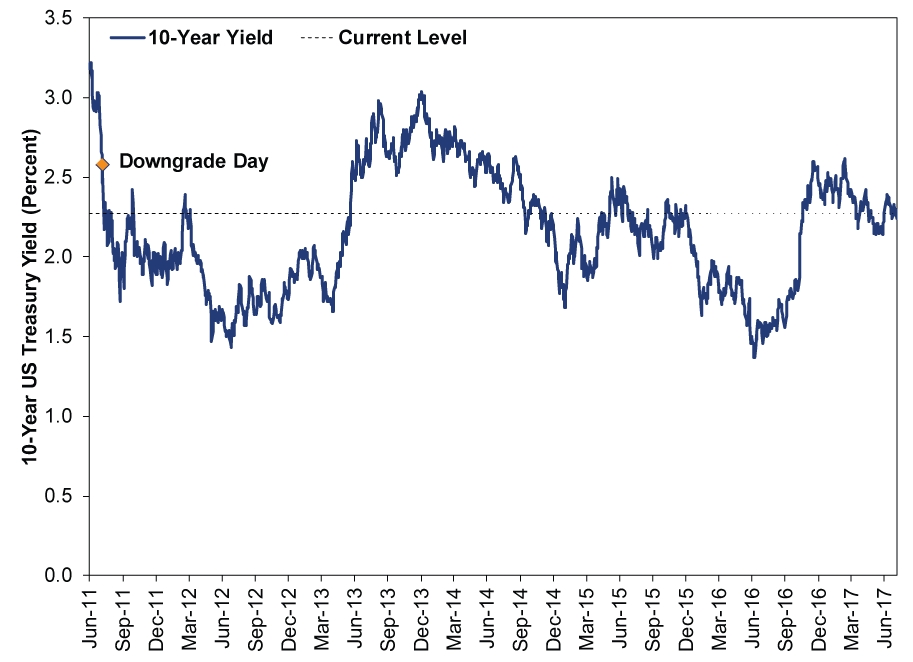

Today it's clear the sky hasn't fallen. Uncle Sam didn't default. Investors didn't dump US Treasurys en masse. China upped its holdings.[iii] Interest rates didn't soar. Stocks didn't implode. Capital markets didn't have to reorganize around a new safe-haven asset. Nor did pension funds or other institutional investors. The dollar is still tops in the forex reserve world. China's yuan gained reserve currency status, and almost no one noticed. Through Friday's close, 10-year Treasury yields are still down 31 basis points since Downgrade Day.[iv] The S&P 500 is up 134.9%.[v] Here, pictures.

Exhibit 1: Downgrades Are Bullish

Source: FactSet, as of 8/4/2017. S&P 500 Total Return Index, 6/30/2011 - 8/4/2011.

Exhibit 2: What Bond Bloodbath?

Source: FactSet, as of 8/4/2017. 10-Year US Treasury Yield (Constant Maturity), 6/30/2011 - 8/4/2017.

In retrospect, S&P did the world a huge favor: They proved beyond the shadow of a doubt that nationally recognized statistical ratings organizations (NRSROs) are not all-wise, clairvoyant or especially useful. They showed firsthand that the rationale for a rating change is usually backward-looking, arbitrary or both-everyone already knew Congress was a gridlocked gaggle of sycophants who preferred grandstanding to governance. Investors, meanwhile, showed they don't much heed what NRSROs say and kept on buying Treasury bonds. As we wrote way back on August 8, 2011, the day of that -6.6% bloodbath:

Before the downgrade, one major fear was a lower rating would mean banks would have to dump Treasurys and replace them with other AAA-rated securities. However, on Monday, regulators quickly assured banks (and those who transact with them) the lower rating will not increase Treasurys' risk weighting. Instead, US debt retains its zero-weight in the global banking complex, allowing banks to hold as much as they like without raising additional capital. Thus, banks have no new incentive to dump Treasurys. Other entities that might otherwise be inclined to sell Treasurys due to rules requiring them to own AAA debt are small in comparison and will likely amend those mandates-keeping US debt their most viable option.

In other words, regulators thought so highly of credit ratings that they just changed their own rules to preserve the US's status as a global benchmark, whatever the raters' opinion. Banks, pension funds, central banks and individual investors kept buying all the US bonds they could get their hands on. All effectively ignored the raters, basing their decisions on their own judgment instead of a press release. They did the same in early 2013, when it was the UK's turn to get a downgrade.

Stocks proved something, too: They bounced fast, as they regularly do after big, emotional, fundamentally unwarranted slides. Within a week, the S&P 500 was above pre-downgrade levels. The next few months were still rather rocky, as stocks globally remained in a correction thanks to eurozone crisis jitters, but a new rally began in early October. Those who stayed cool when the going got tough eventually earned handsome rewards for their patience.

So happy birthday, downgrade-and thanks, S&P, for this valuable object lesson (and for being a great punching bag).

[i] This is a joke. Neither nation is a debt-ridden basket case.

[ii] Source: FactSet, as of 8/4/2017. S&P 500 total return index, daily return on 8/8/2011.

[iii] Until 2015, when it sold off a slew to prop up the weak yuan.

[iv] Source FactSet, as of 8/4/2017. US 10-Year Treasury yield, 8/5/2011 - 8/4/2017.

[v] Source: FactSet, S&P Indices, as of 8/7/2017. S&P 500 total return, 8/5/2011 - 8/4/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today