Personal Wealth Management / Market Analysis

Here Come the Downgrades

Credit ratings are opinions, not market drivers.

Now that major developed nations have signed off on trillions of dollars’ worth of COVID-19 economic response packages, they are starting to ratchet up bond issuance in order to pay for all of it. We have started seeing concerns about massive government debt increases trickle through the financial news arena, and over the weekend, one associated milestone occurred: Fitch downgraded the UK’s sovereign credit rating to AA-, citing the pending bond blitz. If recent history is a reliable guide, this will be only the beginning—not the end—of downgrade chatter. Hence, we thought it would help to highlight how markets have responded to sovereign credit downgrades over the past decade.

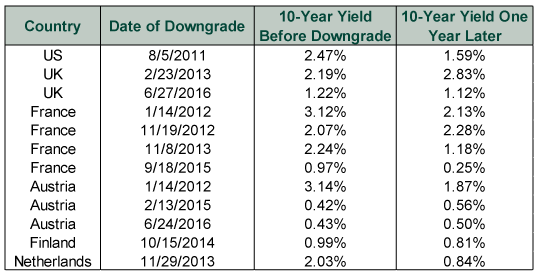

The standard fear when debt issuers get downgraded is that investors’ perceptions of their creditworthiness will also degrade, causing interest rates to rise and making debt more difficult to issue and service—a self-fulfilling prophecy. Yet as Exhibit 1 shows, this hasn’t historically been the case. Several nations, including the US, have lost their top credit ratings over the years. Some received multiple downgrades. Yet none of their interest rates soared. In many cases, long-term yields fell.

Exhibit 1: A Brief History of Sovereign Downgrades

Source: FactSet, as of 3/27/2020. 10-year benchmark government bond yields on the last trading day before the downgrade date referenced and one year after that date.

We think the reason downgrades don’t cause yields to spike is simple: Credit ratings are opinions based on widely known information—information bond markets have already priced in. Ratings also don’t alter the main drivers of bond demand. US Treasury bonds are high on everyone’s list due to the unmatched depth, liquidity and stability of US capital markets. That didn’t change when Standard & Poor’s downgraded Uncle Sam’s credit rating amid 2011’s debt ceiling standoff, citing political bickering. The ratings agency registered its opinion—and investors registered their own. The market’s collective wisdom is a much better determinant of any nation’s creditworthiness, in our view.

Regardless of what raters might have to say on the matter from here, we think markets can easily absorb the new debt about to hit the wires. This is anecdotal evidence, but after the UK announced plans on Tuesday to double its scheduled bond issuance this month, the 10-year gilt yield … didn’t move. It closed Monday at 0.31%.[i] And at market close Wednesday? 0.31%.[ii] Strictly from an interest cost perspective, if ever there were a time to ratchet up debt and lock in dirt-cheap funding costs, this is it. Same goes for the US, where 10-year Treasury yields are at 0.61% as we type.[iii]

So, in our view, whether or not raters continue to have a negative opinion on the matter, a investors don’t need to add a sovereign debt crisis emerging from all these government response plans to their list of imminent market risks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

-

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

-

Expert Commentary This Week in Review | Consumer Confidence, Iran Developments, Bond Yields

2026-05-29

2026-05-29 -

Market Analysis What AI Tech Stocks Are Signaling About This Bull

2026-05-28

2026-05-28

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today