Personal Wealth Management / Politics

History Shows Election Nerves Don’t Stress Stocks

Getting closer to an election won't automatically roil stocks.

Are US politics going to make this a cruel summer for stocks? Speculation about November's US presidential election has ramped up now that some uncertainty has faded. Donald Trump is the presumptive GOP nominee and Hillary Clinton holds a commanding delegate lead on the Democratic side. Pundits are doing pundit-y things,[i] from postulating about hypothetical matchups to speculating about what the potential winner will do once in office. There is also lots of chatter about what the near-term market impact will be, with some arguing that the closer we get to the election, the greater uncertainty will be-roiling stocks. However, this is largely backward. History shows stocks don't usually stumble as elections near. Instead, uncertainty falls as the election approaches and markets gain more insight on both candidates, getting used to the idea of either as president. Falling uncertainty is often a bullish force as the election nears. That doesn't mean stocks are certain to do great this summer and autumn-we don't make short-term forecasts-but it is powerful evidence they shouldn't automatically suffer.

The "pre-election = volatility" crowd believes the campaign trail's noise will raise uncertainty and fear about what either candidate will do once in office. However, this presumes markets will automatically hate everything candidates say-a sign of bias. While a ton of pundits analyze and speculate about what politicians say, these takes are opinions, not facts. And in an election year, political opinions bombard folks from every direction-the TV, the Internet, the newspaper and in regular day-to-day conversation.

Investors may be forgiven if they find themselves overwhelmed by all the noise, but the notion stocks are similarly unnerved isn't quite right. While in the ultra-short term, talk can stoke volatility, the sheer volume of political noise also means basically every political opinion and take gets priced in. One person's political feelings are unlikely to be radically unique or surprising-and surprises move markets. Moreover, everything discussed on the campaign trail for Democrats and Republicans alike is part of markets' discovery process, which clears up question marks about the candidates. Stocks hate uncertainty above all else, and every little nugget about what Candidate X argues or Candidate Y focuses on chips away at that uncertainty.

Stocks will price in gradually falling uncertainty well before the results are in. Markets are effective discounters of widely known information, and they don't wait for complete clarity on any event. As the election draws near, fewer unknowns will remain. At the start of year, the sheer number of candidates made it look more like the Republicans were trying to field a football team than decide on a nominee. After the Indiana primary, only one candidate remains. On the Democratic side, Clinton holds a virtually insurmountable delegate lead over Senator Bernie Sanders, though Sanders has vowed to continue campaigning until the convention.

Moreover, Congressional races will similarly garner more attention as the summer months come, and this year's could easily extend gridlock. Though the Democrats have a structural edge in this year's Senate races, seizing control means flawless campaigning-difficult to achieve. In the House, the Republicans have the edge due to incumbency and gerrymandering. Hence, a Clinton or Sanders win would likely mean more gridlock-as could a Trump win, as his outsider posturing could put him at odds with the GOP leadership.

As attention shifts towards November's general election, the candidates will start offering more specific policy proposals, indicating where their priorities lie. For example, in the 2008 presidential race, both Senators Barack Obama and John McCain promised big health care reform. Obama's version became reality, passing into law in 2010, but markets were aware that regardless of the victor, changes to the current health care system were coming-it wasn't a surprise that roiled stocks.

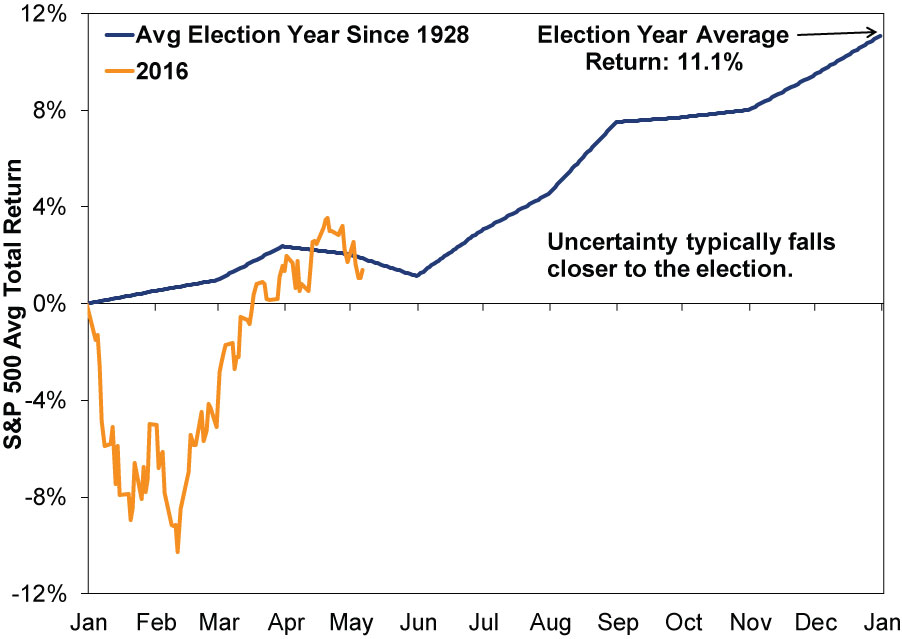

Beyond theory, market history shows stocks don't weaken when an election draws near. But before we get into that, our standard disclosure: Markets are incredibly complex and digest myriad factors. The presidential election is a political driver, and while important, it is but one factor. For instance, in 2008, FAS 157 (mark-to-market accounting) and the government's haphazard response drove that global bear market, overwhelming other factors like the presidential election. With that said, the data don't support the argument stocks weaken closer to presidential elections. Some suggest that markets trend downward in the six months ahead of November's election. However, history-as we display in Exhibits 1 and 2-shows stocks aren't typically weak in the knees as elections draw near.

Exhibit 1: AverageElection Year Returns for the S&P 500

Source: Global Financial Data, as of 5/13/2016. Average cumulative S&P 500 total return in election years since 1928.

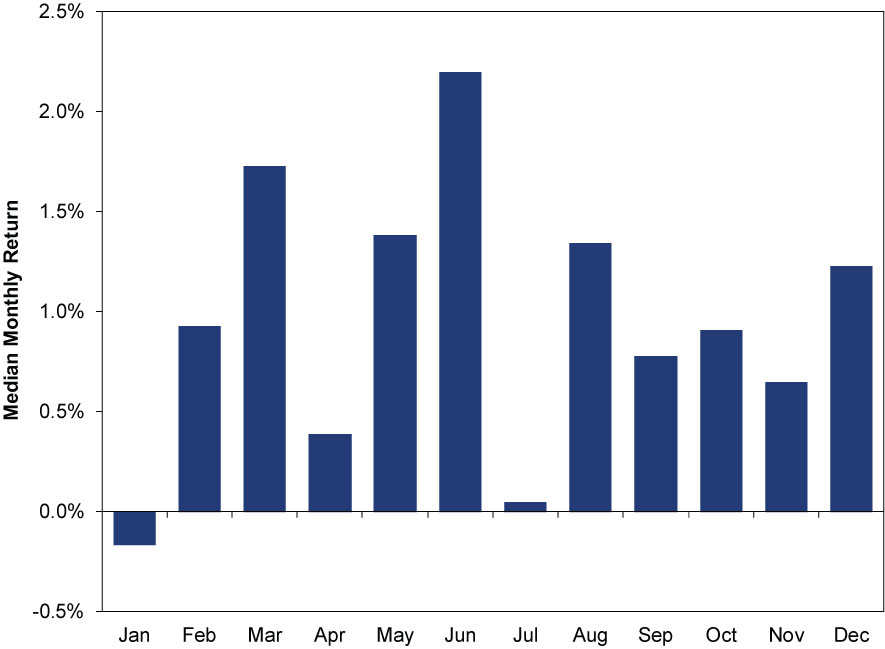

Exhibit 2: S&P 500's Median Monthly Returns During Election Years Since 1928

Source: Global Financial Data, as of 5/10/2016. S&P 500 Total Return Index during presidential election years since 1928.

While July is a shade above flat, June has the best historical median returns of any month in election years. More notably, no month in the six-month run up to the election has a negative median return. What's more, only one month (July) in that period has a lower frequency of positivity than the overall monthly average of 61.9%.[ii] History rebukes the notion stocks get antsy closer to a vote.

While pundits focus on how the 2016 presidential election "is different this time"-the four most dangerous words in investing-we encourage investors to remove their political biases: It is quite unlikely this election causes a bear market. Historically, presidential election years are usually positive-which you might surmise from the earlier exhibit-and the US tends to outperform as Election Day nears. (Exhibit 3) The fact the tech bubble and Financial Crisis hit during election years (2000 and 2008) is coincidence without causality-they had little connection to the elections.

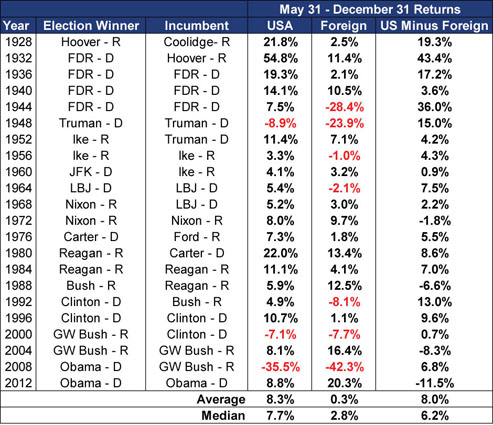

Exhibit 3: The US Typically Outperforms as Elections Near

Source: Global Financial Data, as of 1/21/2016. USA returns are the S&P 500 price index. Foreign is the GFD World Ex. US Price Index. May 31 - December returns, 1928 - 2012.*

Historically, stocks have risen in 82% of US presidential election years since 1928, with an average return of 11.1%.[iii] This is because elections are much more about talk than action, and that talk gets oodles of media attention, reducing surprises. That allows markets to digest fears and move forward. Politicians' biggest impact on stocks comes when they take action, passing legislation-which usually doesn't come with a lame-duck president in office and Congresspeople on the campaign trail. Hence, political risk is higher early in a new administration, not in election years, when they are shaking hands, kissing babies and otherwise courting the electorate.[iv]

As we get closer and closer to Election Day and the rhetoric ramps up on both sides, we suggest investors keep cool this summer and tune out the noise. Uncertainty overall will fall, not rise, this year.

[i] Pundificating?

[ii] Source: Global Financial Data, Inc., as of 5/11/2016. Frequency of positive monthly S&P 500 total returns, December 1925 - April 2016.

[iii] Ibid.

[iv] Note: That doesn't mean 2017 is automatically bearish, as gridlock could reign or other factors could swamp political drivers.

* Corrected table: Exhibit 3 initially reversed the names FDR and Hoover, citing Hoover as Election Winner and FDR as incumbent. Of course, Hoover didn't win in 1932, and was in fact quite crushed by FDR, with the electoral college margin of victory a massive 472-59. A simple oversight on our part, for which we apologize. We've corrected in this updated version.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Upcoming IPOs, US Jobs Data, Credit Card Delinquencies

2026-06-05

2026-06-05 -

Market Volatility Seek Perspective Instead2026-06-05

-

Market Analysis No Flowers for the May Jobs Report?2026-06-05

-

Expert Commentary The US Midterm Campaign Trends Ken Fisher Is Watching

2026-06-04

2026-06-04

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today