Personal Wealth Management / Market Analysis

How Not to Use Valuations

While market valuations do not predict forward returns, they are a useful gauge of sentiment.

19, 17, 27. No, this isn't a pattern-identification test. Nor is it a Fibonacci number sequence or our gym locker combo. It is also not LeBron James' salary (in millions of dollars) over the last three years, though that's close. These are three flavors of current S&P 500 price-to-earnings (P/E) ratios. All are above their long-term averages, leading many to contend that any way you slice it, US stocks are overvalued, expensive, or any other adjective you might use-hence sub-par returns must lie ahead. But valuations-no matter the flavor-do not predict future returns.

What exactly are these different P/Es? Simple! They are, in order, the S&P 500's trailing, forward and cyclically adjusted P/E ratios. Trailing earnings are the index constituents' reported profits over the prior 12 months. This is the oldest and arguably best-known P/E ratio-stock price divided by actual, reported, known earnings.

But reported earnings are ... well ... already reported-old news. Stocks look forward, so many consider trailing P/Es irrelevant. To solve this, many use forward P/Es-the second "traditional" measure-which compare prices to consensus earnings expectations for the next year. Analysts estimates often prove inaccurate, but proponents claim they are usually close enough and are at least forward-looking. Analysts currently expect rising profits over the next year-explaining why the S&P 500's forward P/E is currently the lowest of the three.

Others think traditional P/Es' real problem isn't that their denominator is backward looking or estimated, but rather, that they are so darn volatile! And not (oddly) inflation adjusted. Enter the cyclically adjusted P/E ratio, or CAPE. Created by Harvard's John Campbell and Yale's Robert Shiller, CAPE's denominator is an inflation-adjusted average of the last decade's earnings. CAPE crusaders[i] say this smooths the business cycle's occasionally big skew, providing a more accurate gauge of stocks' value. When those CAPE crusaders[ii] first founded the gauge, they claimed its original purpose was to project average long-term returns (10 years), but many have twisted this since its creation and instead use it to predict near-term returns.

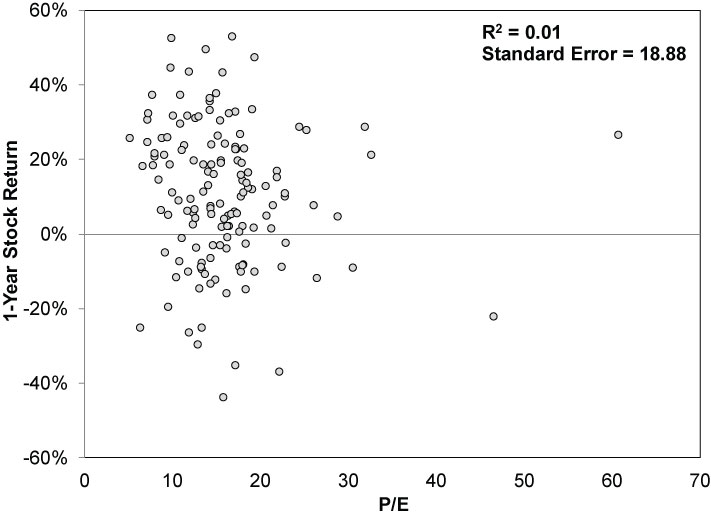

But no matter which gauge you pick, stock returns are all over the map following periods of high (and low) valuations. There is no statistical correlation between high valuations and low future returns (or vice versa). Pretty much every valuation was extreme in 1929 and 1999, and stocks fell. But on many other occasions, stocks rose-sometimes by a lot-when valuations were above average. All three P/Es were above average for most of 2003 - 2005 and 1995 - 1999-stocks rose through both periods. The S&P 500's trailing P/E fell below its then-long-term average of 14.6 in May 1973-a mere four months after a bear market began-and kept plunging, along with stocks, through October 1974.[iii] In November 1980, the trailing P/E was a cheap 9.2-but a bear market began and ran until August 1982.[iv]

Those are extreme examples of P/Es' follies, but an all-inclusive look proves the point, too. Looking at the statistical correlation between stocks' trailing P/E ratios and forward looking one-year returns (between 1871 and 2014), we find valuations explain only 1% of forward stock returns. Now, take some of this with a grain of salt, because reporting in the 19th and early 20th centuries wasn't as rigorous as it is today. Nor are market returns pre-1926 the most reliable, as the fine folks at the Cowles Commission have thoroughly vetted data from 1926 onward only. But it illustrates the broader point all the same.

Exhibit 1: 1-Year Stock Return Versus P/E Ratio 1871-2014

Source: Global Financial Data as of 6/29/2015. Yearly Trailing 12-Month Price-to-Earnings Ratios as of 12/31 (as-reported earnings) and subsequent annual S&P 500 Total Returns, 1871-2014. R2 is the statistical measure of how much an outcome (in this case stock returns) is explained by a variable (in this case P/E ratios). A zero reading would indicate valuations explain none of forward market returns, while a reading of 1 would indicate valuations completely explain market returns. Standard error is the measure of the statistical accuracy of an estimate.

Our boss, Ken Fisher, described this scatter plot as a "shotgun blast" in his 2006 bestseller, The Only Three Questions That Count-there is no linear trend to note. Now, if you squint, it might look a little like a political map of former Soviet Republics, but that isn't useful for investing. If you're trying to figure out where stocks are headed at any given point in time, you may want to focus on the other 99% of what drives prices.

CAPE is no better. Actually, it's worse, because it is super backward-looking-the last 10 years of earnings don't predict the next 10. Also, in its effort to smooth away the extreme earnings declines during recessions and big rebounds in early recoveries, CAPE actually adds skew by keeping old recessions in the calculation years after the fact. Today's CAPE includes one of the worst profit declines in modern history (2008-2009), skewing average earnings lower and making CAPE look high for most of this bull market. It has exceeded its long-term average of 17.7 since August 2009 and topped 20 since December 2009, but the S&P 500 is up 127.4% and 103.8% over the same time frame.[v] CAPE didn't foretell that.[vi]

As for CAPE and its original purpose, forecasting 10-year returns, its creators purport to show a decent correlation, but even so, it is of little use to investors in the real world-any correlation is likely more coincidence than causal. Long-term returns are a function of long-term changes in stock supply and demand-not the last 10 years of earnings and recent price movement. But even if CAPE did work and nailed 10-year average annualized returns on the head, acting on it would add no value. Today, CAPE predicts below-average returns over the next decade-that doesn't mean every year will be bad or even below average. A flattish decade like the 2000s could have seven great years and three lousy ones. Most investors would probably want to participate in the great years. 10-years is simply an arbitrary timeframe-actual market cycles, which usually don't stack up with the Roman calendar, are far more meaningful.

CAPE, overall, is about as useful as a whale's hip bone. Traditional P/Es do have some use as an indicator of investor sentiment and where we are in a bull market's progression up the proverbial "wall of worry," but even here you can't simply look at the level. Valuations tend to be high early in bull markets, as stocks bounce before earnings recover. This clearly doesn't reflect euphoric sentiment. The path over an entire bull-once the early recovery works its way out of the calculation-is more telling. Trace it, and you can see confidence ascend as investors pay more for future earnings-and you can see this can actually run on for a long while before you arrive at that euphoric peak. In industry lingo, we call this multiple expansion.

So what of today's above-average P/Es? They've risen only modestly over the past couple years, which suggests investors are still just cautiously optimistic. We haven't yet seen the strong multiple expansion typical of late-stage bull markets like the late 1990s and mid-1980s. That is a good sign stocks have room to run, with P/Es likely rising alongside.

[i] Sorry.

[ii] Again, our apologies.

[iii] Source: Multpl, https://www.multpl.com/, as of 6/30/2015.

[iv] Source: Multpl, https://www.multpl.com/, as of 6/30/2015.

[v] Source: Factset, S&P 500 total returns, as of 6/30/2015. 7/31/2009-6/29/2015 and 11/30/2009-6/29/2015.

[vi] Even one of CAPE's creators (hahahahahaha-you probably thought we'd type "crusaders" here) recently said he's confused by this, "I've been very wary about advising people to pull out of the market even though my CAPE ratio is at one of the highest levels in history. Something funny is going on. History is always coming up with new puzzles."

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today