Personal Wealth Management / Market Analysis

Impact of Economic Growth Trends on Equity Returns over the Long Term

The relationship between economic growth rates and equity returns is not statistically significant in the long term.

Many believe US economic growth (as well as global) will inevitably be slower over the next 10 years than it has been historically. Suppose, for a moment, making such long-term forecasts consistently and accurately is possible (in our view, it isn’t). A logical next question in this hypothetical scenario is: How might slower long-term growth impact equities? It may sound counterintuitive, but our research shows the long-run rate of economic growth has virtually no impact on equity returns.

Empirical Evidence

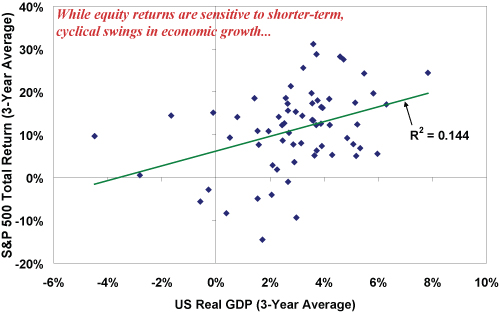

First, consider the evidence. Comparing post-WWII equity returns to GDP growth over rolling three-year periods suggests equity returns are sensitive to shorter-term, cyclical economic swings. The chart below illustrates this cyclical relationship by plotting GDP over three-year periods vs. equity returns over the same period. Our analysis gives us an R-squared of 0.14—meaning a mild positive relationship.

Exhibit 1: S&P 500 Return vs. US Real GDP—Cyclical: Rolling 3-Year Periods Since 1946

Source: Global Financial Data, Inc., as of 12/2/2011.

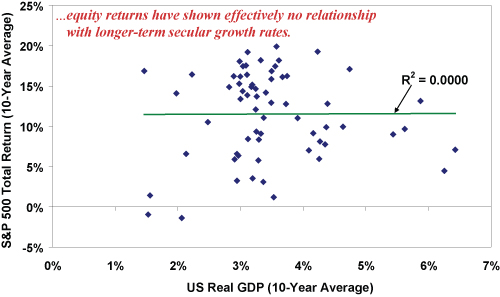

However, looking at longer 10- or 20-year periods shows essentially no relationship between equity returns and longer growth trends. The R-squared here is 0—meaning absolutely no relationship between the two factors exists.

Exhibit 2: S&P 500 Return vs. US Real GDP—Secular: Rolling 10-Year Periods Since 1946

Source: Global Financial Data, Inc., as of 12/2/2011.

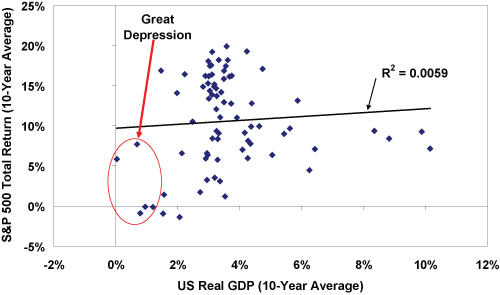

Even including the Great Depression, which had low growth and low equity returns, isn’t enough to create a meaningful statistical relationship between long-term growth rates and stock returns.

Exhibit 3: S&P 500 Return vs. US Real GDP—Secular: Rolling 10-Year PeriodsSince 1926

Source: Global Financial Data, Inc., as of 12/2/2011.

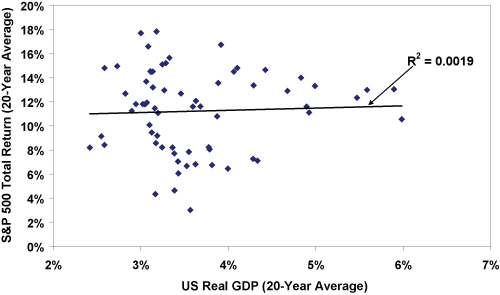

Exhibit 4: S&P 500 Return vs. US Real GDP—Rolling 20-Year Periods Since 1926

Source: Global Financial Data, Inc., as of 12/2/2011.

While it may seem counter-intuitive that long-term economic growth doesn’t drive equity returns, it’s important to remember equity markets are not a direct representation of the economy. Rather, capital markets simply allocate capital to the areas within an economy where investors believe a desirable risk-adjusted return can be achieved.

The allocation of capital is governed by supply and demand. For equity markets, while aggregate net demand may fluctuate rapidly, share supply is relatively fixed in the short term. Actions increasing supply of shares (IPOs, secondary offerings, stock-based mergers, employee stock grants, etc.) or decreasing supply (buybacks, cash-based mergers, companies going private, bankruptcies, etc.) are typically slow-moving. Thus, over shorter periods—like 12 to 24 months or so—the volatility of aggregate demand is the primary determinant of returns. However, over longer periods, share supply can expand or contract near-infinitely. Ultimately, changes in share supply over long periods divorce equity returns from broad underlying economic growth by reallocating capital.

While this applies to the broad market, it is easy to illustrate the impact of supply by looking at individual companies. Imagine Company A is a Tech firm that can grow its net income at a 15% average annual rate over the next 10 years, while Company B is a large Consumer Staples firm that will grow its net income at a 5% average rate over the same period. However, Company A issues employee stock incentives and options, regularly diluting earnings per share by about 5% per year, while Company B, facing low returns on newly invested capital, decides to buy back 5% of its shares each year. While net-income growth is vastly different for the two companies, earnings-per-share growth would be about 10% for each (roughly). Company B is essentially returning capital to shareholders to be reallocated. Assuming neither pays a dividend and P/E ratios remain stable, they likely have virtually identical stock returns despite the widely different underlying economic opportunities, all else being equal.

For Company B, the shrinking supply of shares offsets the lower growth opportunities—a natural response of share supply to price and valuation movement related to investors’ required return and a company’s cost of capital. From the company’s perspective, when stock valuations are high (commonly after a period of above-average returns), issuing stock is a cheaper way to raise capital than issuing debt. Conversely, when stock valuations are low (often after a period of below-average performance), it can make financial sense for a firm to use cash or borrow funds to buy back shares. If a company fails to do this, other players might step in, such as a private equity firm using leverage to take the company private, which also reduces the overall supply of public equity shares.

The net result? While short-term equity returns may be volatile as aggregate demand reacts to various influences (including economic conditions), over the long term, share supply can expand or contract massively—responding to wholly different pressures. This is one reason little relationship exists between longer-term economic growth trends and equity returns.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today