Personal Wealth Management / Market Analysis

Infrastructure Isn’t Always Industrial Grade

Is President Trump's planned infrastructure spending an opportunity for investors?

In the wake of Donald Trump's election, many attributed Industrials stocks' rise to expectations for increased US infrastructure spending-one of Trump's big campaign promises. However, that doesn't make it wise to pile into infrastructure-related sectors solely based on Trump's pledges. It's still too soon to say exactly what the administration focuses on as the new president formally takes the reins, but expectations for an outsized infrastructure impact have likely outpaced reality.

Already moderating his promises a bit, Trump has lowered his infrastructure spending plan from the campaigned $1 trillion to $550 billion-roughly 3% of GDP. Now $550 billion worth of spending could be impactful if spent all at once (and presuming it didn't crowd out private investment in the process). However, it's likely spread out over many years-muting its stimulative power-and probably wouldn't start until 2018, just in time for midterms. It's also unrealistic to expect an infrastructure bill-or any bill- to pass through Congress undiluted or without bringing up other political landmines like raising taxes or deficit spending. In other words, there is a lot of potential for gridlock to get in the way.

Updating infrastructure has benefits, but the economy doesn't need a massive infrastructure bill to keep growing-the private sector has done fine driving most of the growth this expansion. Past infrastructure spending bills haven't moved the needle because they require years of planning, and spending typically gets bogged down across myriad national government agencies-not to mention conflicts with state and municipal needs. Consider the 2009 American Recovery and Reinvestment Act, which lacked readily available projects and drove little meaningful revenue for Industrials companies. And 2015's five-year, fully funded (by the Fed's dividends) $305 billion Highway Bill has thus far had a muted effect, going almost unnoticed.

Typically, big fiscal spending is most impactful during a recession, when businesses aren't spending and money isn't moving-this isn't the case today. While national infrastructure projects can drive material economic gains, it depends on the nature of the project. The Eisenhower Interstate Highway System, which comprised about 6% of 1956 GDP, had a big impact because it was relatively new and unique, and it massively improved the movement of goods. Today's upgrades aren't likely to cause anywhere near as big a jump. Not only that, undertaking such an endeavor requires politically viable funding; massive political capital; deep alliances across parties on national, state and local levels; as well as broad voter support. Mr. Trump meets few of these criteria currently.

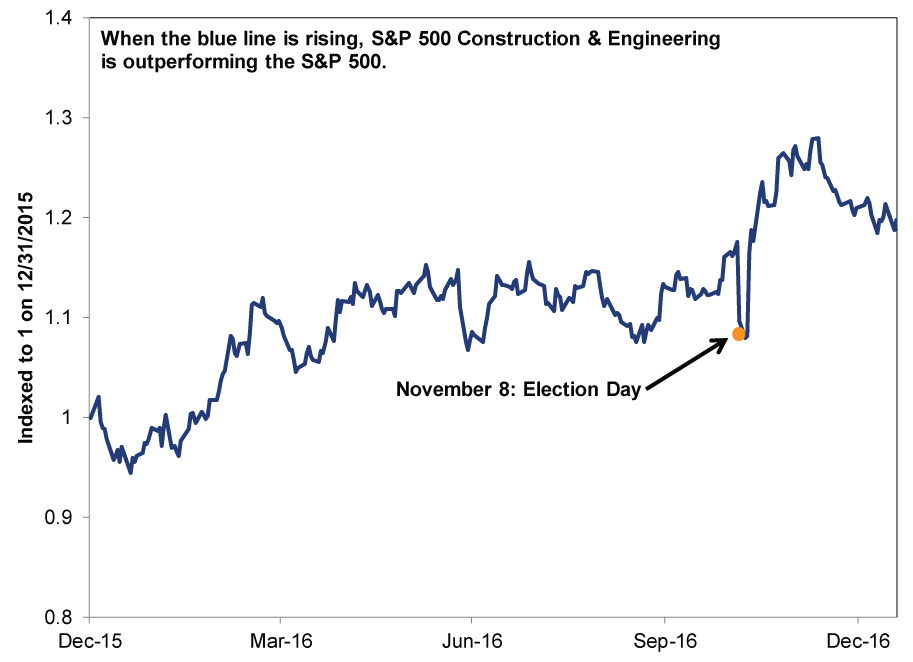

Conflating short-term market movement to a single factor-in this case, Trump and his potential spending plans-is an error. Like the broader equity market, infrastructure-related sectors have been rising since last year's correction, which bottomed in mid-February. They were also outperforming well before the election, a period when almost no one fathomed Trump winning. Post-vote gains are part of the broader bull market, not a Trump-inspired phenomenon, and the industry has already given back much of that initial relative pop. (Exhibit 1)

Exhibit 1: S&P 500 Construction & Engineering vs. S&P 500

Source: FactSet, as of 1/19/2017.

This early in the game, trying to pick industries that may or may not benefit from a Trump presidency amounts to investing on narratives, guesses and contradictory statements from the man himself. Investors are far better off looking more broadly. The bull market is likely to continue climbing because of underappreciated economic positives, gridlocked government and improving investor sentiment-not because of promised spending that may or may not happen.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today