Personal Wealth Management / Politics

Inside George Osborne’s Red Briefcase

The red briefcase wasn't the only symbolism in Britain's budget.

UK Chancellor George Osborne and his Treasury cohorts practice moving in formation before delivering 2016's Budget. Photo by Stefan Rousseau - WPA Pool/Getty Images.

As always, our political commentary is non-partisan and non-ideological by design, and our analysis aims to assess policies' market impact only. We favor no political party or politician and believe partisan bias invites investment errors.

While pundits were busy dissecting the fallout from Super Tuesday 2.0[i], an altogether different political spectacle caught our eye: The UK's annual Budget, announced by Chancellor George Osborne Wednesday. Like all Budgets, it was crammed full of giveaways and pie-in-the-sky pledges to boost growth, with a few digs at the opposition. Economically it creates winners and losers, as all fiscal tweaks do, and there are political implications as well. Nothing here much changes our outlook for UK stocks, which remains quite bullish, but it's always good for investors to have the lay of the land.

Most of Osborne's speech was theater, starting with the 18 references to this being a Budget for "the next generation."[ii] Much was made of the Office for Budget Responsibility's GDP forecasts, which Osborne bragged projected growth through the end of this Parliamentary term-no shock, considering nonpartisan governmental agencies tend to extrapolate the recent past forward and have pretty much never penciled in a recession for a few years down the line just because. (And if they started now, we are quite sure it would be decried as partisan.) Osborne also included some obligatory swipes at the opposition Labour Party (over debt, deficits and former Prime Minister Gordon Brown's infamous gaffe about ending boom and bust) and the Scottish National Party (over their likely inability to support the North Sea oil industry if Scotland voted for independence)-as well as some shout-outs and giveaways to constituencies that flipped their allegiance to the Conservatives last May. This is all just political spin, which markets tune out. We suggest investors do the same.

Now, then, to the actual budgetary stuff-spending and deficits. Osborne stuck to his long-running pledge to run a surplus by 2020, promising (or warning of, depending on your viewpoint) another £3.4 billion in public spending cuts by then. Underpinning this were the Office for Budget Responsibility's (OBR) updated economic estimates, which revised the national debt and nominal GDP lower, resulting in a slightly higher debt-to-GDP ratio. We've long found the UK government's "austerity" push unnecessary and odd, as debt service costs were never problematic and, for all the talk, Osborne has never cut spending. Not once. He cut projected spending, but that is just fancy talk for making public spending rise more slowly. This newly promised "cut" is more of the same: Spending remains set to increase every year through fiscal 2020-2021. Cuts or no, though, the UK's fiscal footing remains firm: Debt service costs were just 7.2% of total tax revenues last year, even cheaper than America's.

As for the specific policies, here's the rundown:

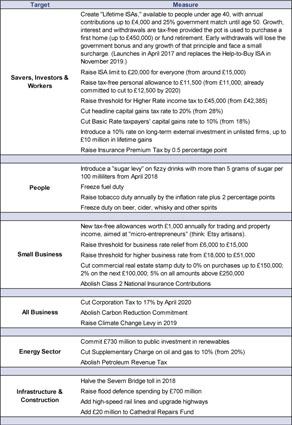

Exhibit 1: Major Provisions of the 2016-2017 Budget

Source: Her Majesty's Treasury, as of 3/16/2016.

There are winners and losers galore. Rumors of another round of wholesale pension reform proved false, and the tax-free lump sum distribution lived to see another year. Pension saving did get a shakeup, however, with the introduction of new Lifetime ISAs intended to encourage younger folks to save. Savers, investors and workers win, mostly. So do small businesses, kitchen-table entrepreneurs and the self-employed. Beer drinkers win, but soda drinkers and smokers lose. Corporation tax cuts should benefit firms across the board, though some of that will no doubt be eaten up by measures to clamp down on "tax avoidance," which is populist-speak for "closing loopholes companies used legally and legitimately to reduce their tax burden." We'd call the North Sea oil industry a winner, too, but the abolished tax has raised practically no revenue lately.

Overall and on average, these tax tweaks, however nice for the winners, are likely immaterial to stocks. Historically, stocks and taxes have no set relationship. Tax cuts aren't automatically positive or negative. Nor are tax hikes. Taxes are but one variable impacting growth in individual countries. For global markets, their relative importance is about a fraction of a peanut-and changes to that fraction of a peanut are unveiled under bright media spotlights, rendering them largely devoid of surprise power.

Devolution also got a push. Another chunk of local spending and investment was shifted from Westminster to cities and counties throughout England, and the much-ballyhooed "Northern Powerhouse"-a lofty attempt to boost heavy industry in North England-got some extra oomph. Wales got some budgetary love, too, with a £1.2 billion investment deal for Cardiff, negotiations for a similar "city deal" for Swansea, and £50 million for a "Compound Semiconductor Catapult" (jargon for an incubator/research cluster). The Severn Bridge toll reduction was even couched as Welsh economic stimulus, which is a bit like saying cutting the Bay Bridge toll would kickstart growth in Oakland, CA, but that's politics for you, we guess. These and the many other local investment provisions are no doubt nice for the recipients, but they're also just window dressing as far as the broader UK economy is concerned. "Let there be growth" as a development strategy in free-market economies has a success rate of about zero.

So why bother? Apologies for the cynicism, but the answer is likely politics. One, the Tories won a slim majority last May and are anxious to keep it. Doing so requires keeping constituents new and old happy-giveaways and platitudes can be successful in that department. Two, Prime Minister David Cameron plans to step down before 2020's election, and Osborne's ambitions to succeed him are well-known. His chief rival is London Mayor Boris Johnson, who happens to be on the opposite side in the EU referendum campaign. If "Leave" wins, Johnson's stock will likely soar and Osborne's will plunge. Why not take advantage of the last Budget before the referendum to grandstand a bit and curry some favor in advance?

Speaking of which, the "Brexit" debate was front and center in the Budget. Osborne used his speech to bolster the "Remain" case, stressing that all the forecasts are based on EU membership, and leaving will probably cause some painful downward revisions. As we've written before, that isn't necessarily true, but the real question is: How will all this land with voters? Some reports indicate "Project Fear," as some have colorfully dubbed the "Remain" campaign's economic arguments, isn't much swaying people. Polls have narrowed considerably in recent weeks. Whether Cameron, Osborne and the rest of the "Remain" crew stick with the dour, fear-based campaign-or instead highlight the many positive economic and sociological aspects of EU membership-might have a large influence on June 23's vote. For now, if the Budget is any indication, fear remains central to the campaign, but the world will have to wait and see.

For UK stocks, it doesn't much matter that the budget was heavy on symbolism and light on economically significant policies. The UK is already one of the world's freest, most competitive economies. Economic growth there is fine and likely continues, judging from the high and rising Leading Economic Index. A do-little government might frustrate some, but when markets like the status quo, they like governments that preserve it. UK stocks had plenty to like before Wednesday, and they still do.

[i] Codename "Super Twosday," trademark pending.

[ii] In the "our children" sense, not the Star Trek sense. We think.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

Politics France Falls Into Political Purgatory … Again2025-09-12

-

Expert Commentary Fisher Investments Reviews Fed Rate Cuts2025-09-12

-

Market Analysis Putting Stagflation Claims in Actual Context2025-09-11

-

Expert Commentary Should Investors Hold Cash on the Sidelines?2025-09-11

Learn More

Learn why 185,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 6/30/2025

New to Fisher? Call Us.

Contact Us Today