Personal Wealth Management / Market Analysis

Inside the UK Downgrade

The UK’s downgrade isn’t great news, but it shouldn’t much impact one of the world’s healthiest debt markets.

The ratings agencies struck again Friday, when Moody’s downgraded the UK from AAA to Aa1—a one-notch drop. In the release, Moody’s cited the “challenges that subdued medium-term growth prospects pose to the government’s fiscal consolidation programme.”

So once again, it seems, a rater has made a rather arbitrary decision—much like the US was downgraded for the political brinksmanship surrounding the arbitrary debt ceiling—the UK’s been downgraded for not quite reaching its self-imposed, equally arbitrary deficit reduction targets. That says next to nothing about its overall fiscal health, which even Moody’s admitted is fine, saying “the UK’s debt-servicing capacity remains very strong and very capable of withstanding further adverse economic and financial shocks.”

Still, ever since downgrade rumors started circulating, many have feared its potential impact. US and French bond markets may have largely shrugged off their own recent downgrades, many fear the UK won’t be so resilient, suggesting rising gilt yields and the falling pound suggest heightened risk. In our view though, there are several reasons to believe a downgrade shouldn’t much impact the UK’s economic or fiscal health.

For one, rising gilt yields aren’t necessarily a sign of downgrade doom—it’s relatively normal for yields to rise in the run-up to the downgrade and then fall after. That’s what happened in the US, France and many other nations downgraded in recent years. This is basic investor psychology at work—rumors drive fear, and fear drives volatility. But after the downgrade, when the uncertainty is resolved, volatility tends to ease. Similar sentiment could very well be driving sterling volatility, and could now abate some since the downgrade has become reality.

Even without the threat of a downgrade looming in recent days and weeks, higher gilt yields wouldn’t surprise—not because risk is mounting, but because of market forces. As foreign investors regain confidence in Spanish and Italian debt, they’re moving from so-called “safe haven” assets like gilts to higher-yielding European sovereigns. Selling pressure typically means higher yields. Long-term gilt yields are also influenced by investors’ long-term inflation expectations. With inflation at 2.7% and not expected to fall any time soon, we’d rationally expect gilt yields to be somewhere north of the sub-1.5% witnessed last summer. But the BOE’s Asset Purchase Programme (quantitative easing) weighed on long rates, keeping them lower than they otherwise would have been. Now that the BOE’s sitting tight (the last round of purchases wrapped in November 2012), yields have somewhat more bandwidth.

Plus, despite the recent uptick, gilt yields remain near historic lows—not really what you’d expect of something “risky.” Fact is, UK debt markets are among the world’s deepest and most liquid, giving investors plenty of reasons to continue owning them.

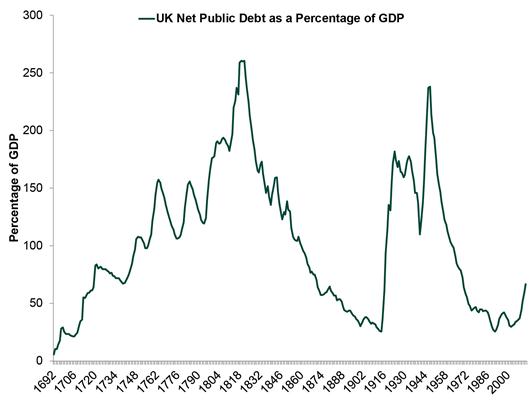

UK debt is also among the world’s most stable. Headlines may fret missed deficit targets, but deficit targets are political machinations. They don’t reflect the underlying health of Her Majesty’s Treasury. Here’s what does: Though net debt has risen in recent years, at 66.6% of GDP (2012 official estimate) it remains well below levels seen during much of the last three centuries. That’s below the US and well under EU maximum targets (80%—though the UK’s not subject to the Stability and Growth Pact’s limits). (Exhibit 1)

Exhibit 1: UK Net Public Debt as a Percentage of GDP, 1692 – 2012 (Estimated)

Source: HM Treasury, as of 02/21/2013. Includes official 2012 estimate. All others are actual outturn.

Debt is plenty affordable, too. Interest payments are about 8% of tax revenue—right in line with the US, which investors universally regard as among the world’s safest debt. According to Treasury forecasts, even if gilt yields were to rise to 5%, interest payments would only rise to about 10% of tax revenue in the next three years. Markets understand this—so while short-term volatility is possible (always is), it’s likely markets shrug off this downgrade once the immediacy is past.

The downgrade likely will have a political impact though. During the 2010 election campaign, Chancellor George Osborne said his party’s deficit reduction plans aimed to “safeguard Britain’s credit rating,” essentially staking his reputation on the AAA and setting off a national obsession with the rating. To many UK voters, the downgrade likely signals the failure of the government’s “austerity” program (a combination of tax hikes and cuts to projected spending increases) and likely dogs the coalition through the 2015 election. Many folks simply don’t realize keeping AAA was an arbitrary goal, politically convenient with the PIIGS floundering and downgrade rumors swirling on the Continent. Nor do they realize ratings agencies’ decisions are arbitrary, backward-looking and not indicators of economic health.

Not that the UK economy’s in stellar shape. As long as monetary policy remains contractionary and regulatory uncertainty reigns, many businesses—particularly small and medium firms—may struggle to grow. At the same time, ongoing efforts to free labor markets and cut red tape in the private sector should boost the UK’s huge service sector and—perhaps—motivate larger firms to start deploying the roughly £750 billion on corporate balance sheets in growth-oriented spending. And even with existing headwinds, there are bright spots throughout the economy—it may be struggling to find a stable growth trajectory, but it’s not uniformly weak.

And Friday’s downgrade simply doesn’t alter those fundamentals—backward-looking downgrades almost never do. Markets have long known the UK’s deficit reduction program would likely last longer than first planned—the government admitted as much in last December’s Autumn Statement. So take the downgrade for what it is—a rubber stamp on information folks already knew. Not a sign of things to come.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today