Personal Wealth Management / Market Analysis

Interest-ingly Rising Rates

Though interest rates have been rising lately, we don’t see this as cause for concern.

The 10-year US Treasury yield has risen from 1.67% to 2.18% in the past few weeks—the UK, France, Germany and Japan also saw their 10-year government bonds’ yields rise—which has sounded the alarm for some bond investors. Folks also fear rising rates signal higher borrowing costs to come and perhaps higher inflation on the not-too-distant horizon. However, in our view, rates remain low and rate movements seem like normal volatility.

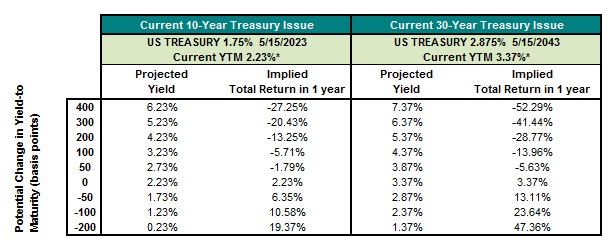

Now, for bond investors, concern is understandable, since rising interest rates mean existing bond prices fall (see Exhibit 1). With rates so low, even a modest upward rate move can have a big impact on bond prices. For example, if interest rates rise 100 basis points in a year (not an unreasonable move), holders of 10-year Treasurys will see their bond values fall by 5.69%. Holders of 30-year bonds will see bond values fall by 13.93%.

Exhibit 1: 10-Year and 30-Year US Treasury Yields

Source: Bloomberg Finance, L.P., as of 06/12/2013.

But even though rates have ticked up, they remain near generational lows, as shown in Exhibit 2. That rates are so low doesn’t mean they must rise fast or soon. They might very well bump along sideways for some time. But some volatility is expected and normal.

Exhibit 2: 10-Year US Treasury Yield

Global Financial Data, Inc., as of 6/13/2013.

As for borrowing costs, as interest rates rise, the cost to rent money does get more expensive—which could be a concern, particularly since lending growthhas been slow during much of the current economic expansion. But that’s not because rates have been too high. Lending growth has been slow, in large part, because banks have been disinterested in lending. The Fed’s endless rounds of QE have served to flatten the yield curve—which diminishes the profits banks can make on their next loans. With the low end of the yield curve pegged near zero, rates ticking up helps widen the yield curve, providing banks more incentive to lend. That’s a good thing, particularly since rates, though higher, are still quitelow by historical standards.

As for inflation, it’s true higher rates can reflect the market’s future expectation for inflation. But at this point, rates don’t seem to be signaling anything worrisome. Not too long ago, we were concerned about deflation—a much worse condition than some increasing inflation. And inflation has been incredibly tame for over a decade now. Even longer, perhaps. So inflation ticking up some (if it does) from very low levels doesn’t seem to be a material negative for the period ahead. Plus, with central banks globally still engaging in deflationary QE combined with still elevated levels of unemployment, there are multiple forces acting to keep prices in check.

For now, we’d expect to see continued volatility in interest rates. And rates moving up from generational lows wouldn’t surprise. But we don’t anticipate normal interest rate volatility derailing the expansion nor the equity bull market.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today