Personal Wealth Management / Market Analysis

Italian Debt Catches the ECB’s Eye

With or without the ECB’s help, Italy’s debt doesn’t look like a crisis-in-waiting.

When global stock and bond markets entered this year’s rough patch, it was probably only a matter of time before investors returned to a long-running source of worry: Italian debt. Any time eurozone bond yields rise, people worry Italy’s debt woes will return, with soaring borrowing costs rendering the country unable to finance its debt—and resurrecting the eurozone debt crisis. So it went this week as Italy’s 10-year yields jumped past 4.0%, leading to an emergency ECB meeting Wednesday to address the issue. In typical eurocrat fashion, the bank announced a plan to have a plan but offered scant detail, leaving observers guessing. Time will tell what exactly they roll out, but we don’t see much evidence Italy needs the help.

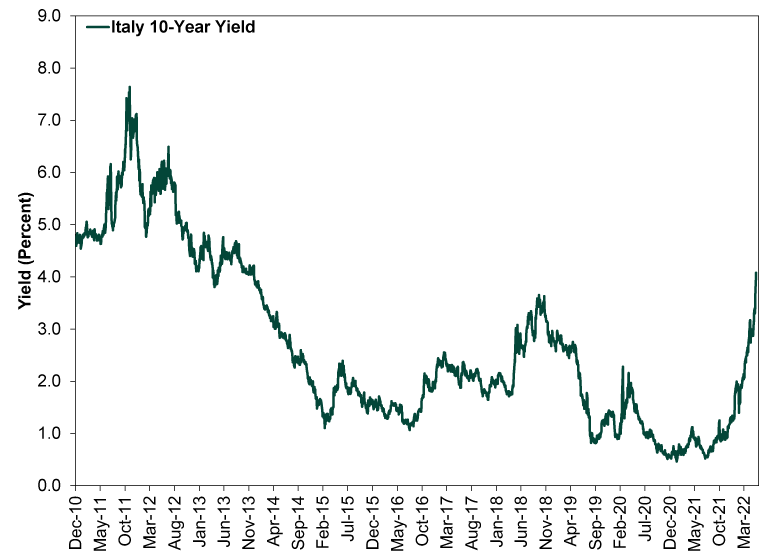

Pundits were a bit surprised last week when the ECB didn’t address Italian debt at its regularly scheduled meeting. Italian 10-year yields exceeded 3.0% at the time, and debt fears were already percolating. The bank’s silence, coupled with its jawboning about raising its policy rate later this summer, seemingly sent sentiment sharply lower, triggering that jump over 4.0% for the first time since 2013, as the eurozone crisis wound down. (Exhibit 1) Hence, today’s emergency meeting.

Exhibit 1: Italian Yields in Context

Source: FactSet, as of 6/15/2022. Italy 10-year benchmark government bond yield, 12/31/2010 – 6/14/2022.

In its post-meeting statement, the ECB said it would get cracking on an “anti-fragmentation instrument” to address divergence in eurozone member-states’ borrowing costs and “apply flexibility” when reinvesting the proceeds of maturing bonds in its portfolio. The first part is a mystery, but pundits are broadly guessing that it will be a new bond buying program similar to the Outright Monetary Transactions (OMT) program. Launched in late 2012 after then-ECB head Mario Draghi’s “whatever it takes” (to support the euro) speech during the heat of the eurozone crisis, OMT enabled the ECB to buy Italian and Spanish debt to reduce each country’s borrowing costs—a big fillip to sentiment at the time. The second part appears to be a pledge to alter the geographic breakdown of the ECB’s bond portfolio so that it can, say, invest the proceeds of maturing German and Dutch bonds into Italian Treasurys. That would enable it to proceed with its balance sheet runoff plans while simultaneously supporting Italy—a rather clever move.

Sentiment over the ECB’s plan seems mixed, if headlines are any indication. It didn’t cause the universal cheer “whatever it takes” did nearly a decade ago. Rather, pundits acknowledged the ECB’s apparent intent while bemoaning that the 150-word statement had no concrete, ready-to-go programs. But markets seemed to appreciate it, with Italian yields easing a bit and Italian stocks rising nicely on the day.

We read that move mostly as a relief rally rather than a sign that the ECB’s plans are a necessary change and fundamental good. As we have written before, rumors of Italy’s impending insolvency have long been greatly exaggerated. While its total debt load is up, servicing that debt pile remains very affordable. As of Q1’s end, total interest payments represented just 12.4% of tax revenues, which is down from nearly 20% during the debt crisis—and down from well over 40% in the mid-1990s.[i] Rising rates could make affordability harder, but it won’t happen overnight. By 2021’s end, the average maturity of Italian debt outstanding was up to 7.11 years.[ii] That suggests to us Italy has a lot of bandwidth to absorb higher rates, especially if it has managed to avoid default at times when debt service costs were far, far higher.

Some argue the pain will start arriving sooner if the ECB doesn’t act, citing the recent interest rate jump and the Italian Treasury’s seemingly big financing needs. This year, about €369.5 billion worth of Italian bonds are maturing, including about €227.8 billion in standard medium- and long-term bonds, known as BTPs.[iii] Based on the amount raised year to date, it does look like the Treasury is back-end loading its refinancing: Through today, the Treasury has met less than half its BTP financing needs for the full year, with only €92.3 billion sold.[iv] Things perhaps look especially bad on the 10-year front, with nearly €60 billion maturing this year and only €17.5 billion sold thus far.[v] But there is more than meets the eye here: Even at today’s higher rates, Italy is refinancing much of its maturing debt at a discount. Tongues wagged when the auction of 10-year bonds two weeks ago carried a 3.1% gross yield, but it replaced a bond with a 5.0% coupon.[vi] Even if the 10-year stayed above 4.0% for the rest of this year, Italy would still be replacing maturing 10-year BTPs at lower rates.[vii] Remember: 10 years ago was 2012, the very height of the eurozone sovereign debt crisis, with rates noticeably higher than today’s as a result. Some of the shorter-dated BTPs issued this year even fetched lower yields than the issues they replaced.

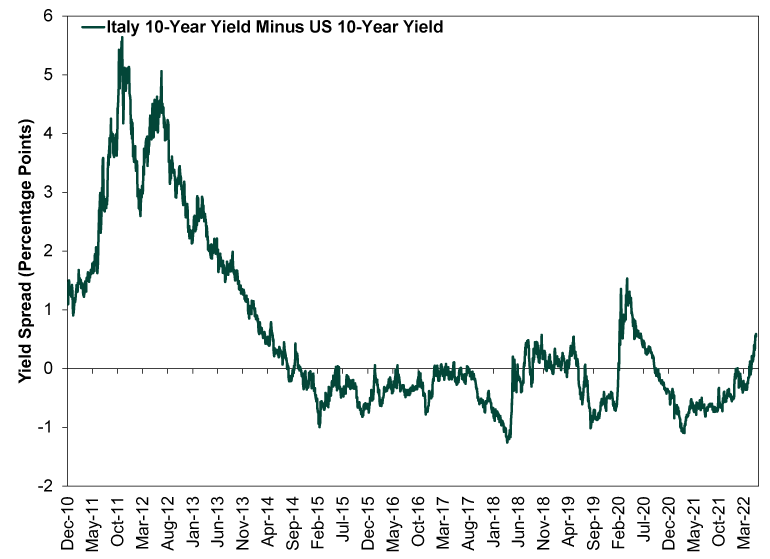

In short, even if the ECB did nothing, we don’t see much evidence Italy would be on the brink of a crisis. Rising yields thus far aren’t translating to skyrocketing debt service costs. Bond auctions are routinely oversubscribed. Then, too, Italy’s rising yields are part of a global trend, and for all the handwringing, they are only about 60 basis points above US yields—in our view, the true risk-free benchmark, given money would likely flow to the dollar in the event of a debt crisis repeat, not another euro country like Germany. If Italian debt were really so risky, it would likely fetch a much larger premium, as it did in 2011 and 2012. (Exhibit 2)

Exhibit 2: Rate Spreads Aren’t at Crisis Levels

Source: FactSet, as of 6/15/2022. Italy 10-year benchmark government bond yield minus US 10-year constant maturity Treasury yield, 12/31/2010 – 6/14/2022.

From our vantage point, Italy looks like a prime opportunity for uncertainty to fall, boosting sentiment higher. To the extent the ECB helps accelerate that process, we imagine markets will welcome it. But even if policymakers don’t go big, markets should gradually realize that Italy isn’t anywhere close to being unable to service its debt, bringing stocks globally some relief.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, US Q2 GDP, Eurozone Inflation

2026-07-27

2026-07-27 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 20 - July 242026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today