Personal Wealth Management / Economics

Italian Debt Perspective

Italy's bond yields moved sharply higher Wednesday, contributing to broad market volatility. But let's add some perspective to the central issue: Italy's debt and its costs.

Italian debt yields crossed 7% Wednesday—sending markets on their latest wild ride. The 7% level is viewed by many in the media as the level spelling automatic trouble. What’s more, the sovereign yield spread widened enough to trigger higher margin requirements on sovereign bonds used as collateral by banks.

We largely agree Italian yields at 7% are less than ideal, but the reality is, from a government finance perspective, it’s not nearly so catastrophic as many think. For one thing, the structure of outstanding Italian debt matters enormously in any discussion of interest rate impact. As it turns out, average Italian debt maturity is about 7 years at average rates closer to 4% or so. So that the secondary market shows rates breaching 7% doesn’t mean the Italian government necessarily pays that rate on its entire outstanding debt stock of around €1.8 trillion. This mostly impacts the rate and success of bond auctions in the near future—Italy has a few auctions left through January 2012 (roughly €50 billion worth), and their rates could be higher, which isn’t terrific. But to help illustrate: If rates remain at 7% through the heavier funding months of February through April 2012, the net effect would be an increase of approximately €5.9 billion in interest costs—not as much as folks may presume.

Much of the impact of 7+% rates depends on how long they stay there and the impact of potentially higher margin requirements. Certainly, if rates remain that high for a period of time, Italy’s situation could worsen—after all, roughly a fifth of Italy’s debt must be refinanced through the end of next year. Should Italy’s treasury not offer to compensate investors commensurate with rates available in the secondary market, auction demand could wane. But bear in mind, in the short term, rates can be quite volatile—meaning they could easily fall back to more benign levels sooner rather than later.

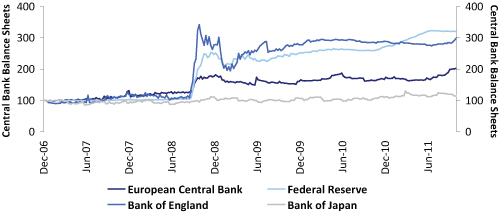

And lower rates aren’t an unreasonable expectation. The ECB has been doing some bond-buying in secondary markets to help keep sovereign rates low, but thus far, they haven’t done nearly as much as they could. From a balance sheet perspective, the ECB currently holds far less debt than either the Federal Reserve or the Bank of England—meaning they have quite a bit of firepower (should they decide to use it) potentially in the form of unsterilized bond purchases, which would effectively be quantitative easing.

Exhibit 1: Major Central Bank Balance Sheets

Sources: Federal Reserve, ECB, Bank of England, Bank of Japan.

That could help push sovereign rates down and lead to some devaluing of the euro. Which would in turn ease the situations in struggling peripheral countries, letting them inflate their way out of trouble.

That’s just one possible scenario of many, and the role of politics shouldn’t be underestimated in the continuing drama, either. The ECB has a new head—Italy’s Mario Draghi. It’s possible some of the ECB’s foot-dragging continues so as not to give the impression of being too easy on countries perceived (by Germany in particular) to have overspent their ways into their current troubles.

There’s also the fact the treaties governing the euro and ECB technically don’t allow for such bond purchases—but the likelihood that truly stops the ECB from acting in a meaningful way seems fairly small. After all, if the eurozone had strictly played by its own rules, Greece wouldn’t have been allowed into the eurozone in the first place. And no one would’ve had deficits as big as many are today.

At the end of the day, there’s little benefit to anyone in waiting so long Italy actually requires a significant bailout. So it could be the ECB may take action if—and when—push truly comes to shove. Italy (and the eurozone as a whole) no doubt continues to face significant challenges. But let’s remember, Italy is a far cry from Greece when it comes to its ability to ultimately return to growth. And it continues to be the case the sudden disintegration of the eurozone likely hurts even the stronger countries like Germany and France more than taking necessary steps to continue backstopping the periphery would.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today