Personal Wealth Management / Market Analysis

Italy and Spain Get New Governments—but Still Have Gridlock

The governments in Italy and Spain may be new, but the gridlock that likely results isn’t.

Citizens in both Spain and Italy are welcoming new governments today. Spanish (now former) Prime Minister Mariano Rajoy lost a confidence vote last night, ousting him and ushering in Socialist leader Pedro Sánchez as PM. And, in Italy, after their initial populist coalition attempt collapsed to start the week—seemingly ushering in a caretaker government and new elections—the Five Star Movement (M5S) and the League renewed coalition talks and formed a new government late Thursday. While these developments are no doubt newsy—and, accordingly, they are getting a ton of media attention today—for stocks, both extend the gridlock already in place. It is unlikely governments in either country are able to pass any significant legislation, a positive for stocks.

ITALY

Early this week, an attempted M5S/League coalition fell apart after President Sergio Mattarella rejected the populist coalition’s choice for finance minister—noted euroskeptic Paolo Savona. After this failure, M5S and League leadership took shots at one another in the press, seemingly showing little sign of renewing coalition talks. Mattarella tapped centrist Carlo Cottarelli as a potential caretaker PM, charged with passing a budget and keeping the government running ahead of new elections. The idea of a new vote stoked uncertainty and roiled markets, particularly since some feared an even more euroskeptic government than the shaky M5S/League coalition could result—and increase the chances of a much-feared Italian exit from the euro (a Quitaly). Thursday, though, Mattarella called the two parties back to Rome for one last chance at forming a coalition government. And it appears they had success.

Key to the deal were the ministerial posts. Savona is out as finance minister and is now tapped to be the (largely symbolic) Minister of EU Affairs. This should allow him to take shots at the EU from Brussels, which we are sure EU President Jean-Claude Juncker is thrilled about. But it gives Savona little actual policymaking power and was a trade-off Mattarella could accept, considering the coalition’s new choice—Giovanni Tria—is more friendly toward the euro. The coalition’s choice for Prime Minister is again Giuseppe Conte, the same former law professor[i] they tapped in their first attempt. League party head Matteo Salvini is to be Interior Minister while M5S head Luigi Di Maio would be Labor Minister. Both would serve as Deputy PM.

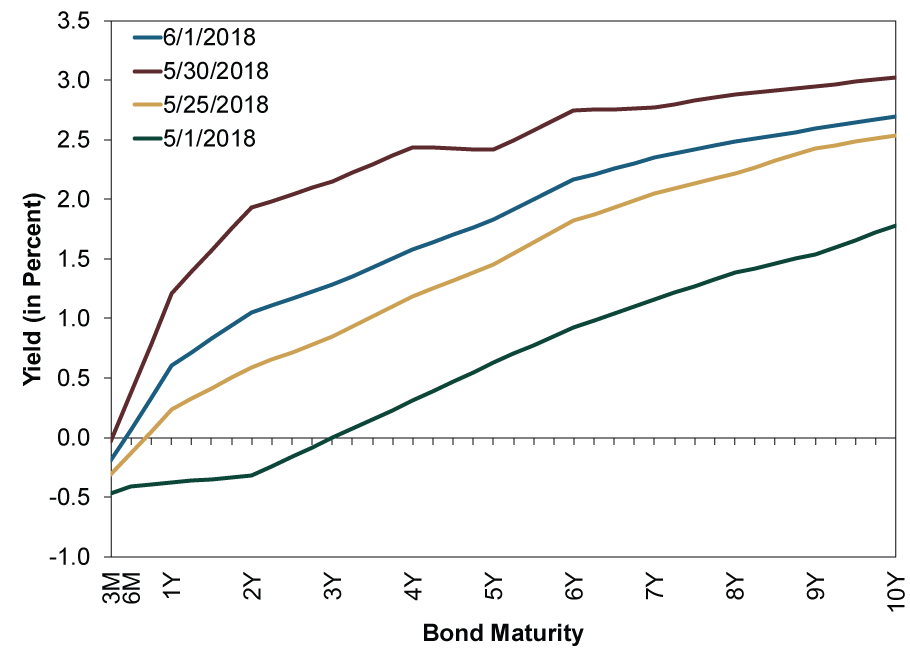

This move at least temporarily quells uncertainty over the Italian government’s composition. That said, we wouldn’t rule out this coalition faltering at some point, given the fact M5S and the League have little ideological overlap. For this same reason, we don’t anticipate major legislation passing that could roil markets. This includes the biggest fear, a Quitaly, as leaving the euro would require a constitutional amendment. It is highly unlikely this coalition could reach the required two-thirds vote in parliament to enact such a contentious law. Markets seem to see this as a relief, with Italian stocks jumping and sovereign bond yields—volatile all week—dropping from highs seen on May 30. (Exhibit 1)

Exhibit 1: Italy’s Bouncy Yield Curve

Source: FactSet, as of 6/1/2018 (at 8:56 AM).

SPAIN

The less-watched eurozone political drama was in Spain. While Italy stole the spotlight, Spanish Prime Minister Mariano Rajoy was attempting to manage a scandal after a judge found several of his Popular Party officials (not Rajoy himself) guilty of corruption and fraud. It seems he failed, as he lost a confidence vote Friday. In as PM is Socialist party head Pedro Sánchez, who got the support of far-left Podemos and Catalan and Basque separatist parties to form a government.

While the change is no doubt noteworthy, we believe this is a non-event for markets. Rajoy was heading an extremely weak minority government unable to accomplish virtually anything of significance. The incoming government will be similarly fragile and unlikely to achieve much of anything. Which is fine for Spain! The country already enacted many major reforms and economic growth has averaged 3.2% annualized GDP growth over the past three years.[ii] (In Q1 2018, it grew 2.8% annualized.) That is at the forefront of developed world growth. Gridlock prevents rolling back reforms Rajoy enacted and should assure the new government has little ability to upend growth through legislation.

All in all, these moves largely extend the gridlock dominating most of the western world recently. Politics that are more benign than many fear are one big positive we believe most investors fail to appreciate presently.

Hat Tip: Christo Barker.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History COVID-Panic’s Lockdown-Low Anniversary2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today